“Africa is the world’s largest untapped growth market for ‘Islamic’ commerce”

The Economist Intelligence Unit, ‘Mapping Africa’s Islamic Economy’, 2015.

The global Islamic financial services industry reached an overall total value of USD 2.4 trillion at the end of 2017, and the market is expected to grow to USD 3.2 trillion by 2020. However, the Islamic finance industry in Kenya remains largely untapped, despite the desire to turn Kenya into an Islamic finance hub for the East African region. In 2016, the International Monetary Fund found that African countries accounted for only 1% of global Islamic finance assets. And according to The Economist’s Intelligence Unit report, Islamic banking represented only 2% of Kenya’s total banking assets.

In Kenya, we are witnessing a silent evolution as the country works towards developing a sustainable real economy. Ambitious changes affecting all Kenyans are being rolled out, the benefits of which will be felt for generations to come. This is the long-term development blueprint that aims to create “a globally competitive and prosperous country with a high quality of life by 2030.”

As part of the vision, the Kenyan regulators are working towards developing financial markets that offer Islamic products and services aimed at providing an inclusive financial sector focus

What is Islamic Finance?

Under Sharia law, it is not permitted to charge interest as money isn’t allowed to generate more money by being put into a bank account or lent to someone else. Instead, banks make their money by sharing the risk of their investments with investors, operating on a profit-loss basis. Importantly, Islamic finance is not just for Muslims as perceived – on the contrary, Islamic financial products have also proliferated in non-Muslim communities.

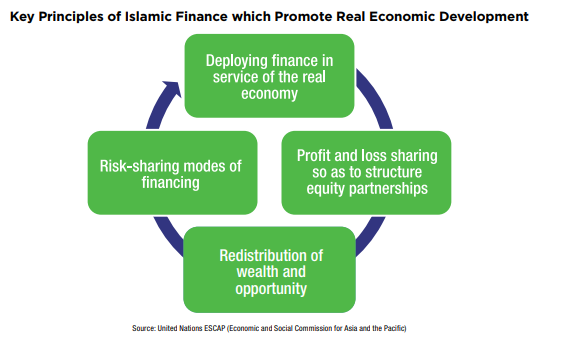

The principles of Islamic Finance support development

Islamic finance not only offers an alternative source of long-term financing for developmental projects but also has inherent characteristics and principles that catalyze real economic development. Through its inherent ethical, sustainable, environmentally and socially-responsible approach that further promotes risk sharing, Islamic Finance connects the financial sector with the real economy. It emphasizes on inclusivity and social welfare in the economy by investing in long-term tangible assets like roads, water systems, electrification in rural areas, provision of sanitation facilities and much more. Such development fosters improvement in standards of living for the poor and takes care of their welfare.

How Islamic Finance can promote Kenya’s real economic development?

Whilst Islamic finance has been part of Kenya’s financial services system for some years, its full potential has not yet been realised, including its role in helping Kenya to achieve its Vision 2030 objectives. Here, we briefly examine how Islamic finance can help Kenya to address some of its development challenges as it progresses towards advancing its real economy:

- Fostering inclusive capital markets – Islamic finance promotes the use of additional financial products amongst consumers who are already accessing conventional interest-based financial services. This accelerates the mobilization of domestic savings, which can be used for investments in infrastructure like roads, water systems and electrification to poor households. Furthermore, it also promotes an entrepreneurial culture among the young and dynamic Kenyan population. The availability of regulated Islamic financial products also enhances inclusive capital markets for the Kenyan communities. Businesses and SMEs benefit from access to an alternative range of financial products thus providing opportunities for access to capital and business growth. Savers keen to earn a Sharia-compliant or ethical return on their savings also take an interest in the range of offerings that Islamic finance has.

- Encouraging alternative sources of long-term finance – Islamic finance offers a wealth of opportunity for a country like Kenya that is undertaking huge strides to develop its national infrastructure. However, raising long-term finance is often a key challenge to the success of these projects. Islamic financial instruments, such as Sukuk (Islamic bonds), offer an attractive solution: they provide a source of long-term funds for projects that are tied to tangible assets (like roads) hence promoting the growth of ‘real economy’.

- Attracting investment flows through foreign direct investment and developing overseas partnerships – A regulated Islamic financial framework not only supports investment flows to Kenya from overseas through Foreign Direct Investments but also bolsters investor protection and confidence. It further strengthens the on-going partnerships with foreign governments and allows for more, similar, partnerships to be developed.

Ready for take-off

Part of FSD Africa’s work on Islamic finance is policy and regulatory reform. FSD Africa’s support to the Kenyan financial sector regulators has resulted in several legal amendments and the development of new regulatory frameworks, which create greater access to these financial products and thus extending their market reach, including:

- The amendment of relevant acts to provide for the issuance of sovereign Sukuks, Shariah-compliant finance products and taxation exemptions.

- Developing regulatory frameworks to facilitate development of Takaful Retirement Benefits Schemes in Kenya.

The benefits of this work are already being felt. The domestic market has also been stimulated with market stakeholders, alike, eager for the expansion of Islamic finance products into mainstream retail, commercial and corporate segments.

Importantly, the competitive advantage that Kenya has achieved is being eyed with keen interest from the region, as is how the country takes the developments forward to enhance the future of its people through promoting sustainable real economic development.