The development of digital finance tools and systems is a key pillar of inclusive finance. One of the key challenges facing the penetration of digital finance in Africa is digital finance capacity and knowledge gaps among professionals and policymakers in financial institutions and governments across the continent.

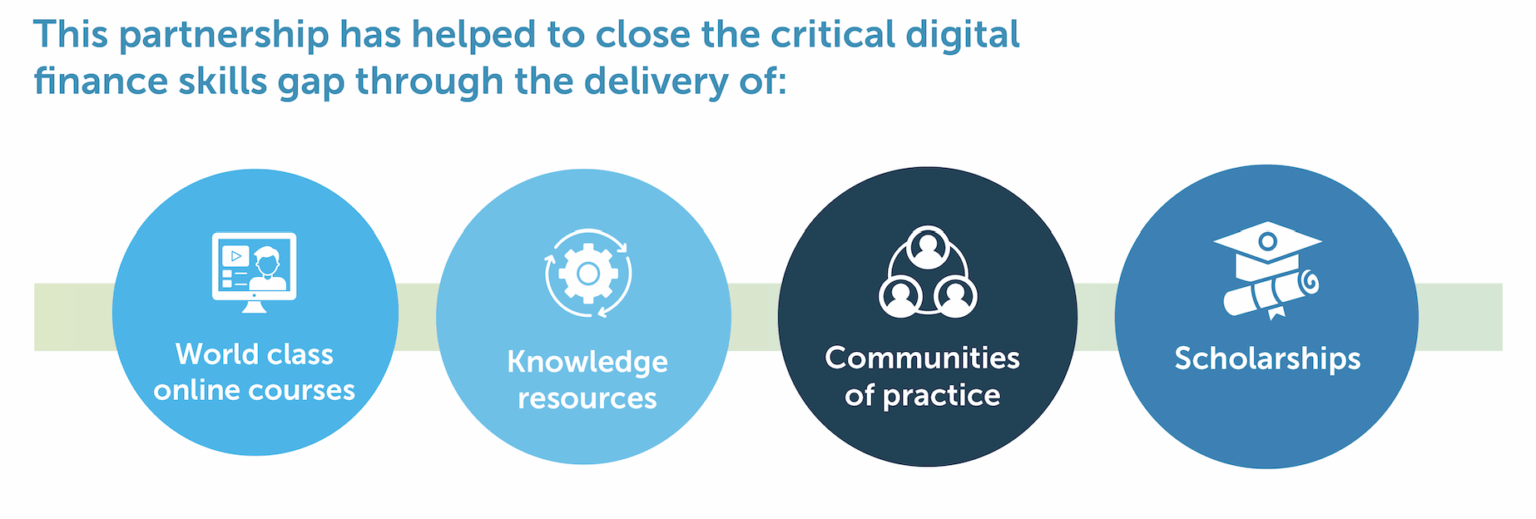

In 2016, FSD Africa partnered with the Digital Finance Institute (DFI) to address this challenge. Through this five-year partnership, we supported the pilot and scale of the institution’s flagship professional program – Certified Digital Finance Professional (CDFP).

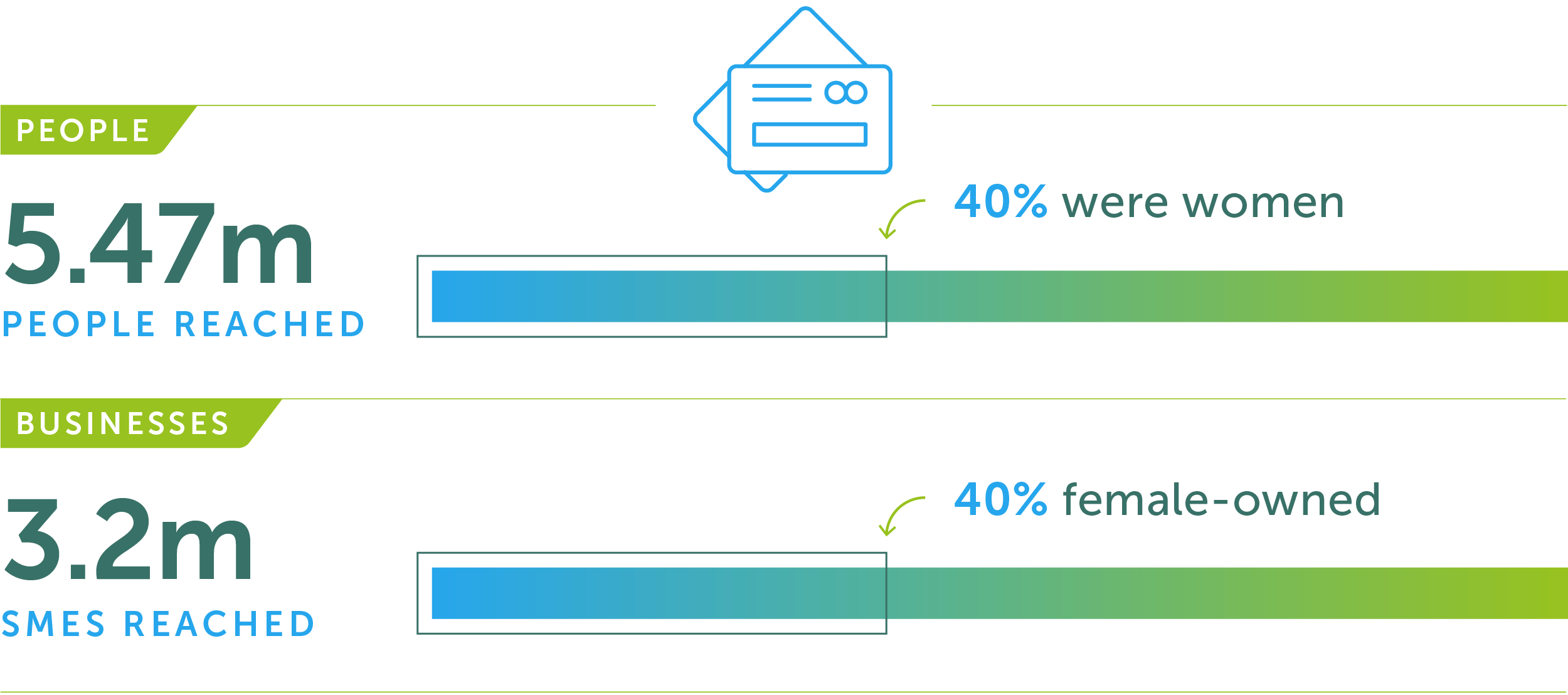

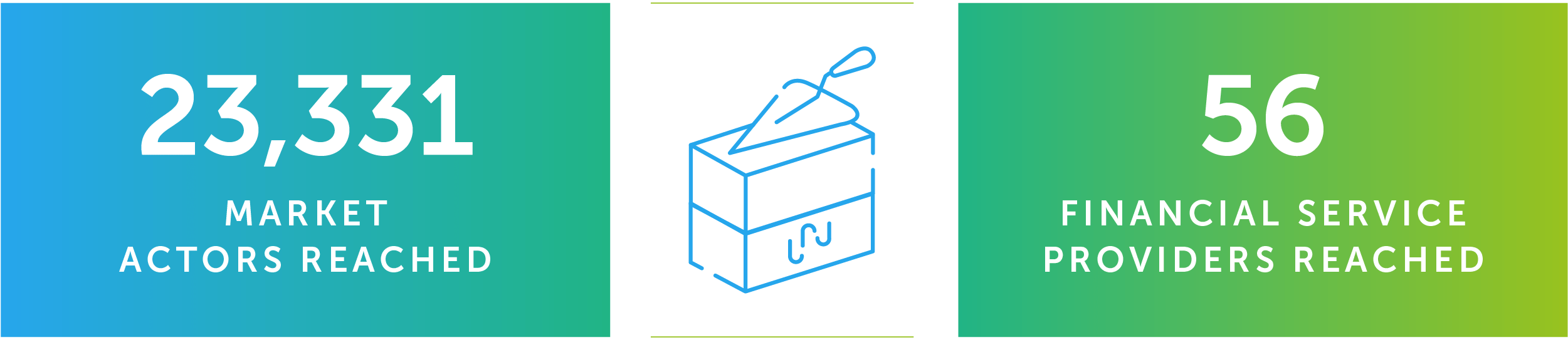

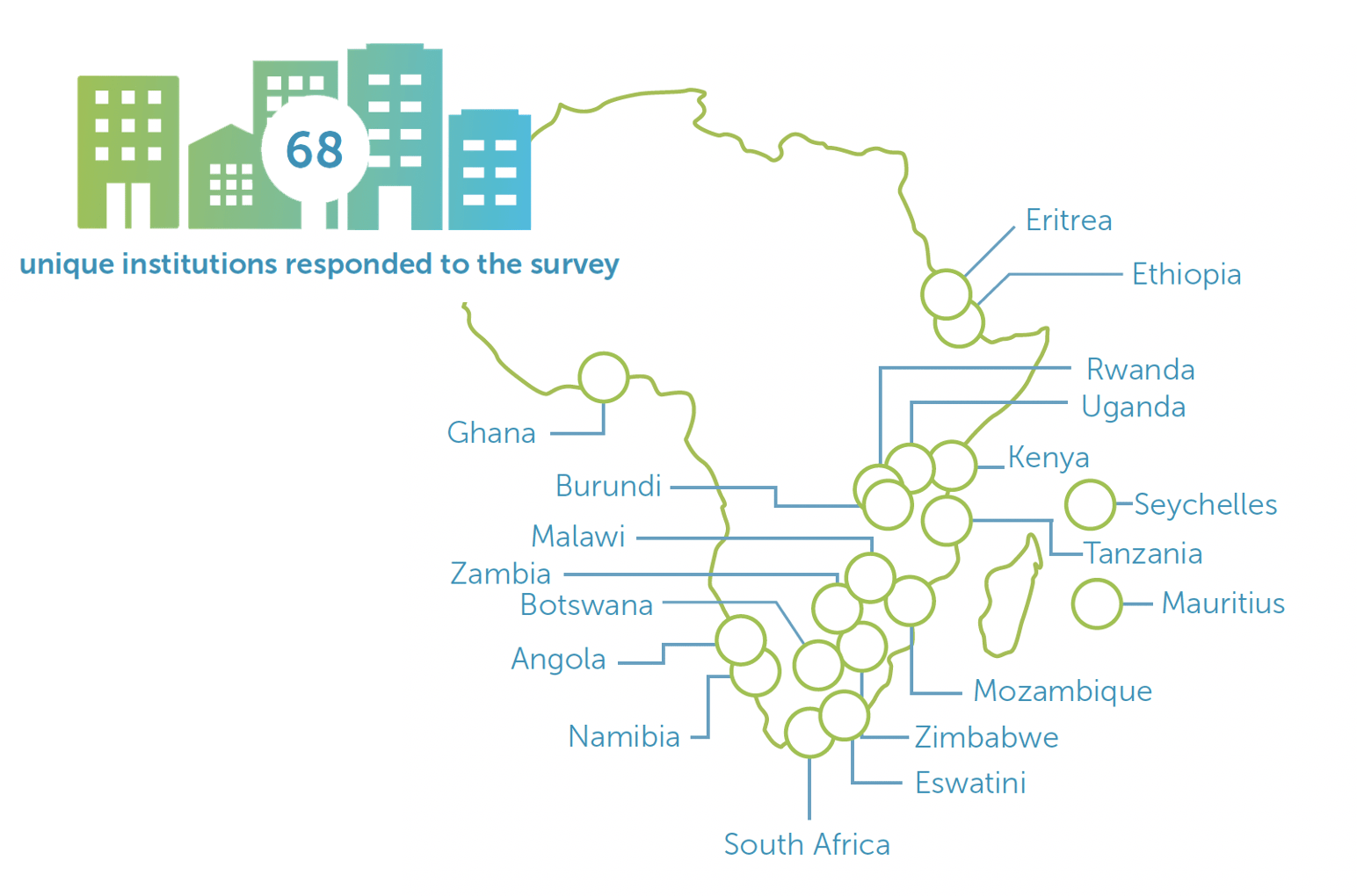

Since then, we have been able to achieve some of the below milestones:

As a result of this work:

- Capacity in digital finance professionals and services providers has increased.

- Institutional capacity for digital finance regulation has increased in both regulators and digital finance providers.

- Digital finance policies, regulations and directives have been developed or adapted by DFI alumni.

- Cross-Sector collaboration has increased resulting in new country-based initiatives on policy, product, customer needs and inclusion.

This partnership leaves the sector with a specialised capacity building utility company (Digital Frontiers), an e-learning school focused on building capabilities and skills aligned to the SDGs (Digital Frontiers Institute), a services business (Gateway), and the formation of a new global Alliance that represents the Inclusive Digital Finance Profession.