ImpactAlpha, February 15 – Community-powered mangrove restoration. Restocking local fish supplies. A marketplace for seaweed farmers.

Triggering Exponential Climate Action, or TECA, invested $27,500 each in seven oceans and seafood enterprises in Kenya, Egypt, South Africa, Uganda, Zimbabwe and Tanzania.

The partnership between BFA Global and FSD Africa also provides the companies with hands-on support.

“We look forward to seeing the impact of their financial and tech-enabled solutions on communities and ecosystems,” said BFA Global’s David del Ser.

Final beta version to follow on heels of agreement on Target 15 in new Global Biodiversity Framework.

Following the adoption of the Global Biodiversity Framework (GBF) at Montreal’s COP15, the Taskforce on Nature-related Financial Disclosures (TNFD) said the release of its V0.4 beta framework in March would further assist firms in assessing and reporting on biodiversity and nature-related risks.

Speaking at the TNFD’s ‘Moving to Action After Montreal’ webinar, David Craig, Co-chair of the TNFD, called the GBF an “ambitious framework” and highlighted its role in “halt[ing] the degradation of nature and biodiversity”. He also underlined the importance of the GBF in ensuring “harmony in nature” by addressing restoring natural ecosystems, which the TNFD’s disclosure framework aims to support.

The GBF featured 23 targets and four goals, but Target 15 is viewed as vital to private-sector management of biodiversity-related risks.

Also speaking on the webinar, Emily McKensie, Technical Director at the TNFD, said there were “key points of conceptual alignment” between the finalised GBF – including Target 15 – and the TNFD framework.

Harmony in nature

Target 15 requires governments to encourage companies and financial institutions disclose their risks, dependencies and impacts on biodiversity along their operations, supply and value chains, and portfolios.

“Target 15 means that disclosures on nature impacts, dependencies and risk are coming and we’re seeing more and more activity to support these,” said Craig. “The TNFD is a framework and a tool to support Target 15.”

McKensie underlined the momentum the TNFD could offer the GBF and Target 15, through its focus on helping firms and investors to disclose and risk manage nature-related impacts and dependencies.

She also highlighted the TNFD framework’s ability to help “operationalise” which organisations will regularly monitor, assess and disclose nature risks, dependencies and impacts, resulting in a “clear connection” to Target 15.

However, the GBF was accused of being “watered down” by a number of observers due the word ‘mandatory’ being excluded from the framework.

Maelle Pelisson, Advocacy Director at Business for Nature, who was privy to the behind-the-scenes negotiations at COP15, admitted that mandatory disclosures would have helped in “levelling the playing field” and demonstrating urgency.

Speaking on the webinar, Pelisson told onlookers the GBF would still help businesses to access data required to accelerate action on reducing negative impacts on nature. Pelisson also welcomed the engagement of businesses at COP15, as well as the rapid growth in momentum surrounding biodiversity and nature.

“We’ve seen this momentum growing so fast from March to December last year,” she said. “We can only expect that it will continue growing now that [the GBF] been adopted.”

September launch and beyond

According to Craig, disclosures are important because they “demonstrate accountability”, but he stressed that they are “meaningless” unless companies take action.

“What’s really important is that companies have invested the time the talent, the knowledge and the skills,” he said. “Don’t underestimate the urgency of the crisis, but also the urgency of the movement,” he added. “The GBF agreement is ambitious [but] it’s real targets will be set by governments and businesses who will see growing pressure and action to align on these targets.”

The TNFD framework builds on the four core pillars of the Taskforce on Climate-related Financial Disclosures (TCFD) for corporates and investors, and is expected to be incorporated into the disclosure standards of existing sustainability standards bodies and national laws.

Alexis Gazzo, Europe West Sustainability Co-leader at EY, told attendees on the webinar that implementation of TNFD guidance will be much faster than TCFD due to the framework “building on the foundations that have been set up for climate”.

The TNFD will run a formal consultation where market participants can submit responses to a full draft of the beta framework from March until 1 June. The pilot testing of the framework, which has been running since 1 July 2022, will also finish on the same day.

The final beta framework is expected to provide additional guidance on disclosure metrics, measurement of impacts, dependencies and risks across supply chains, and the sector-specific reporting requirements, including agriculture, aquaculture and mining.

TNFD’s framework will then be finalised in September 2023.

The next UN Biodiversity Conference (COP16) is scheduled to take place in Turkey in 2024. It will likely see countries providing updates and reviews of their national biodiversity plans targets. Countries will also be expected to develop their national financial plans as a part of their resource mobilisation for implementation.

Today, climate resilience venture launcher Triggering Exponential Climate Action (TECA) has announced the selection of seven startups to each receive $55,000 in funding to advance their solutions for the blue economy in Africa.

The startup founders were selected following their participation in TECA’s fellowship program, where they were supported to create ideas for companies in the blue economy, build teams, and form companies.

vulnerable communities. Each startup will receive $27,500 in seed capital and $27,500 in hands-on venture building support to progress financial and tech-enabled solutions that bolster the climate resilience of communities and ecosystems in and around the oceans, lakes, and rivers across the Eastern region of Africa.

“Through the TECA program, we are proud to support and accelerate the development of innovative solutions that will protect and sustain the environment and vulnerable communities in the Eastern coast of Africa. These seven startups represent the forefront of the blue economy in Africa, and we look forward to seeing the impact of their financial and tech-enabled solutions on communities and ecosystems,” said David del Ser, Chairman and Chief Innovation Officer at BFA Global.

“The ventures that have been formed through the TECA program are an inspiration. They represent young Africans – including women – coming forward with great ideas and solutions to climate-related challenges, in this case, in the blue economy. I’m proud that FSD Africa is supporting this initiative, which leverages finance and technology to help build resilience and create opportunity in the context of climate adversity. Through our partnership with BFA Global, we plan to roll out TECA beyond the blue economy to also solve for other challenges and geographies across Africa.” said Juliet Munro,

Digital Economy Director at FSD Africa.

Founders of the seven startups selected in the current cohort originate from six countries in Africa—Kenya, Egypt, South Africa, Uganda, Zimbabwe and Tanzania—with ideas focusing on bridging existing gaps in: aquaculture; ecotourism; measurement, reporting, and verification (MRV) in conservation; seaweed value chain; mangrove restoration and protection; and financial services for fisher folk. The startup companies and their solutions are:

AquaTrack: a data-driven solution for sustainable aquaculture production. They aim to provide a water quality monitoring device for fish farmers seeking to increase production and efficiency in their farms.

Carboni Bank: a community-centred platform for tourists to offset their carbon emissions and support local climate initiatives.

ConserVate: utilizing innovative digital technology to build local capacity for monitoring reporting and credible verification (MRV) of conservation impact for both funders and implementers to reverse the effects of climate change.

Mwani Blu: building a seaweed marketplace with high-level traceability, providing women smallholder farmers with dignified and stable incomes.

RegisTree: empowering coastal communities to be agents of climate change mitigation by facilitating their role in mangrove restoration and protection.

Vua Solutions: a fintech company seeking to provide affordable and responsible financial services to people working in the blue economy.

Wezesha Aqua Farms: seeking to address the dwindling wild capture fisheries stocks that negatively impact the livelihoods and socioeconomic status of local fishing communities around the great lakes region in Eastern Africa.

To further invest in the success of these startups, TECA will provide comprehensive venture building support that includes mentorship, capacity building, business model refinement, and support launching their products and services in the market.

Startups working on climate resilience solutions are encouraged to apply for the next TECA cohort.

Renewable energy projects attracted investments worth $382 billion globally in 2021, according to the International Energy Agency, but only $13 billion, or three percent of that, funded projects in Africa, highlighting a major funding gap foiling green transition and energy access on the continent.

With only 48 percent of African population having access to electricity, experts say investment in the continent’s renewable energy sector could both leapfrog the green transition efforts and connect more people to the grid.

Despite this, it has been established that investors with the capacity to invest in this sector shy away from the African market, a problem which brought together several stakeholders in the energy sector in Nairobi this week, attempting to change the narrative.

At a forum convened by the World Resources Institute (WRI) and the Children’s Investment Fund Foundation, participants drawn from the private sector, government, civil society organisations from Kenya and beyond deliberated on how investors can be mobilised to support Africa’s green transition through investments.

Reluctant to invest

Rebekah Shirley, WRI’s deputy regional director told the forum that private sector players are reluctant to invest in this sector, creating a funding gap of billions of dollars every year, despite the wide access gap.

“Even in other regions of the world where energy access is still a challenge like the Southeast Asia, we don’t see funding gaps of this magnitude, why Africa?” she posed.

Alex Wachira, principal secretary for the state department of energy, said that there is a list of challenges contributing to the energy gap, even in Kenya, which slow down economic growth in the country.

“We (the Ministry of Energy) are aware of the many challenges attributed to this, including limited incentives to attract private sector investors,” he said in a speech read by a representative.

Lack of political will

Another challenge identified is the lack of political will for appropriate legislation and implementation of policies to incentivise private sector investment in renewable energy projects, especially in rural areas.

For instance, only two of Kenya’s 47 counties have drafted energy plans that would give way to appropriate energy policies, deprioritising renewable energy projects at the local governments.

This, according to Eva Sawe – a senior programmes officer at the Council of Governors, is because lawmakers have not been sensitised on why renewable energy projects should be a priority.

But even with the right policies and incentives to support private sector investment in renewable energy on the continent, investors said there is a still a shortage of talent in Africa limiting the production capacity of companies investing in the sector.

“If an investor is coming into the country to do any renewable energy project, the first hurdle they will face is the lack of skilled people,” said Andrew Amadi, the chief executive of Kenya Renewable Energy Association.

The African continent faces a unique path forward when it comes to industrialization and economic growth as calls for reaching climate goals worldwide continue to grow

Africa needs about $300 billion in climate financing annually

Private funding for green projects in Africa is very low

FSD Africa is in talks with potential green-bond issuers across the continent to raise at least $400 million for climate-linked projects this year.

The agency backed by the UK’s Foreign, Commonwealth & Development Office will be a transaction adviser on the deals it expects to come from countries, including Tanzania, Zambia, Nigeria and Morocco. The amount to be raised will be about 70% higher than what FSD Africa said it helped to mobilize in climate- and gender-related financing in 2022.

Climate resilience venture launcher Triggering Exponential Climate Action (TECA) has announced the selection of seven startups to each receive $55 000 in funding to advance their solutions for the blue economy in Africa.

The startup founders were selected following their participation in TECA’s fellowship programme where they were supported to create ideas for companies in the blue economy, build teams, and form companies.

The TECA programme, managed by BFA Global and supported by FSD Africa, was created to accelerate the development of climate-resilient solutions to protect and sustain the environment and vulnerable communities.

Each startup will receive $27 500 in seed capital and $27 500 in hands-on venture building support to progress financial and tech-enabled solutions that bolster the climate resilience of communities and ecosystems in and around the oceans, lakes, and rivers across the Eastern region of Africa.

“Through the TECA programme, we are proud to support and accelerate the development of innovative solutions that will protect and sustain the environment and vulnerable communities in the Eastern coast of Africa. These seven startups represent the forefront of the blue economy in Africa, and we look forward to seeing the impact of their financial and tech-enabled solutions on communities and ecosystems,” said David del Ser, chairperson and chief innovation officer at BFA Global.

“The ventures that have been formed through the TECA program are an inspiration. They represent young Africans – including women – coming forward with great ideas and solutions to climate-related challenges, in this case, in the blue economy,” added Juliet Munro, digital economy director at FSD Africa.

“I’m proud that FSD Africa is supporting this initiative, which leverages finance and technology to help build resilience and create opportunity in the context of climate adversity. Through our partnership with BFA Global, we plan to roll out TECA beyond the blue economy to also solve for other challenges and geographies across Africa.”

Founders of the seven startups selected in the current cohort originate from six countries in Africa—Kenya, Egypt, South Africa, Uganda, Zimbabwe, and Tanzania—with ideas focusing on bridging existing gaps in: aquaculture; ecotourism; measurement, reporting, and verification (MRV) in conservation; seaweed value chain; mangrove restoration and protection; and financial services for fisher folk. The startup companies and their solutions are:

AquaTrack: a data-driven solution for sustainable aquaculture production. They aim to provide a water quality monitoring device for fish farmers seeking to increase production and efficiency in their farms.

Carboni Bank: a community-centered platform for tourists to offset their carbon emissions and support local climate initiatives.

ConserVate: utilizing innovative digital technology to build local capacity for monitoring reporting and credible verification (MRV) of conservation impact for both funders and implementers to reverse the effects of climate change.

Mwani Blu: building a seaweed marketplace with high-level traceability, providing women smallholder farmers with dignified and stable incomes.

RegisTree: empowering coastal communities to be agents of climate change mitigation by facilitating their role in mangrove restoration and protection.

Vua Solutions: a fintech company seeking to provide affordable and responsible financial services to people working in the blue economy.

Wezesha Aqua Farms: seeking to address the dwindling wild capture fisheries stocks that negatively impact the livelihoods and socioeconomic status of local fishing communities around the Great Lake region in Eastern Africa.

To further invest in the success of these startups, TECA will provide comprehensive venture building support that includes mentorship, capacity building, business model refinement, and support launching their products and services in the market.

Startups working on climate resilience solutions are encouraged to apply for the next TECA cohort. For more information, visit the TECA website.

From sunshine to rare minerals to a youthful population, Africa has the raw ingredients to make the green transition. Now it needs the finance.

Take power. Exceptionally strong sun and vast swathes of desert mean Africa is the region with the highest solar generation potential over the long term, according to calculations by the World Bank. It’s now cheaper to build and operate new large-scale wind and solar farms in many parts of the world than to keep running coal or gas-fired power plants. With more than half of people in Sub-Saharan Africa living without electricity, expanding solar should be a no-brainer.

Yet investment in renewable energy in Africa fell to an 11-year low in 2021, comprising just 0.6% of the global total, according to a report by BloombergNEF. Financing options are insufficient and expensive because lenders worry about the risks of taking on new projects in often politically or economically unstable countries with broken supply chains — though the opportunities can be unrivaled.

“African cities and economies are growing faster than anywhere in the world, so it’s ripe for transformation. The question is why we are not seeing the uptick in investment we should expect,” said Wanjira Mathai, regional director for Africa at the World Resources Institute. “The biggest challenge right now is the cost of capital. To unlock that would be absolutely catalytic.”

Renewable Investment in Africa

Source: BloombergNEF

Note: Global renewable energy asset investment by region

The world’s least developed continent, Africa produces just 4% of global greenhouse gas emissions but is already suffering some of the worst consequences of a changing climate. Rich nations have never met a 2009 pledge to funnel $100 billion a year to help developing countries shift toward cleaner energy sources and bolster their infrastructure against extreme weather.

At the UN-sponsored COP27 climate talks in Egypt last year, delegates agreed to create a new fund for countries battered by climate disasters, though the details have yet to be hammered out. And private sector lenders are calling for multilateral development banks to play a bigger role in financing clean energy projects in poorer nations.

It’s an issue that looms large over this year’s climate conference, which is taking place in Dubai.

Africa needs investments worth $2.3 trillion to meet the needs of its population, plus an additional $1 trillion to bolster its infrastructure against climate disasters, according to estimates from the Africa Finance Corp.

Financing for climate-related projects around the world reached an estimated $632 billion in 2019 and 2020, according to the Global Climate Initiative. Only $19 billion of that came to Africa, including just $2 billion from the private sector.

Even the continent’s buzzing startup scene lags behind the rest of the world. Africa was on the receiving end of just over 1% of the $415 billion in venture capital that went into the startup sector globally in 2022, according to research firm Briter Bridges. Of that, 15%, or around $800 million went into “clean tech” or “climate tech.”

A worker fills a truck that delivers water to remote communities from a pump in Garissa, Kenya, on Friday, May 20, 2022.

Photographer: Simon Marks/Bloomberg

Faced with limited resources and immediate challenges, governments are making stark — and divergent — choices.

“Two days ago, we went to distribute food relief to 4.3 million affected Kenyans in an emergency program that has forced us to re-allocate funds budgeted for education and health,” Kenya’s newly-elected president, William Ruto, told COP27 leaders in November. “The tradeoffs we are forced to make between indispensable public goods is evidence that climate change is directly threatening our people’s life, health and future.”

Ruto called for Africa to leapfrog fossil fuels and embrace clean power as the foundation of its future development. Lacking the oil, gas and coal deposits abundant in some parts of the continent, Kenya has embraced renewables instead. Over 90% of its power comes from sources including solar, wind and geothermal. It also beat the European Union by four years in banning single-use plastic bags and is now considering forcing drivers to pay a congestion charge to curb pollution, a measure that only London has enacted and that New York is debating.

What on Earth?What on Earth?What on Earth?The Bloomberg Green newsletter is your guide to the latest in climate news, zero-emission tech and green finance.The Bloomberg Green newsletter is your guide to the latest in climate news, zero-emission tech and green finance.The Bloomberg Green newsletter is your guide to the latest in climate news, zero-emission tech and green finance.

“They ban coal, and we follow, they say firewood is not for fetching, they say we need to plant more trees,” Bola Tinubu, a leading candidate in this month’s Nigerian presidential elections, said in October. “If you don’t guarantee our finances and work with us to stop this, we are not going to comply with your climate change.”

The Just Energy Transition Partnerships are an effort to respond. The first was signed in 2021 between South Africa and the US, the UK, the European Union, Germany and France. The $8.5 billion financing package was designed to help South Africa transition away from coal and provide a blueprint for new agreements between developed countries and middle-income nations that depend on dirtier fossil fuels.

The details of the deal weren’t agreed until a few months ago though, with South Africa and its partners disagreeing about how the money should be spent. In the meantime, South Africans have faced daily power rationing as the loss-making state utility Eskom struggles to manage its ageing coal-fired plants.

The African Hydrogen Partnership, a grouping of private sector organizations, is pushing to develop green hydrogen as an alternative fro everything from public transport to clean cooking fuel.

“Our focus is on the domestic market,” said its co-founder and vice-chairman Siegfried Huegemann. “It’s where we see great potential, fantastic potential for developing new industries.”

When pipelines and harbors are built, however, Africa could become a major source of green hydrogen for markets elsewhere. The continent has the potential to produce €1 trillion ($1.1 trillion) worth of green hydrogen annually by 2035, according to a study by the European Investment Bank. As with electricity generation, however, transformational changes of that magnitude need money.

“We know that the climate challenge will be significantly difficult to manage and to adapt to — and in Africa the opportunity is dependent upon building resilience and economic resilience above all,” Mathai said. “You can see what a vicious circle this is.”

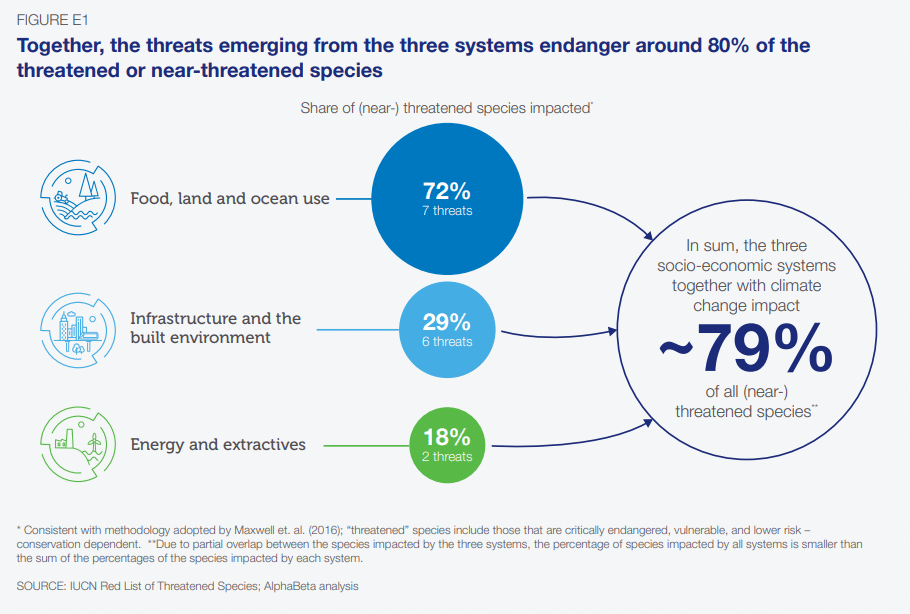

Human activity is destroying biodiversity faster than ever before.

Almost 80% of threatened species are impacted by economic activity.

The COP15 summit has started work towards a new global pact on nature protection.

5 key transformations can save the natural world and boost GDP by trillions of dollars.

Whether you live in a city, a rural area or by the ocean, it’s likely you have noticed a decline in biodiversity. Maybe fewer birds visit your urban feeders, larger mammals are less common in the fields and forests around you, or your catches on those fishing trips are getting smaller.

What we’re all witnessing is a potentially catastrophic loss of biodiversity on which entire ecosystems depend.

Global efforts to protect nature

In an ongoing effort to slow the destruction of nature, delegates at the 2022 United Nations Biodiversity Conference in Montreal, Canada, focused on reversing the rapid decline of animals, plants and insects. The conference, also known as COP15, worked towards a new global agreement to protect biodiversity.

In a strongly worded opening address, UN Secretary-General António Guterres told delegates that “humanity has become a weapon of mass extinction”. Guterres piled further pressure on attendees by describing the conference as “our chance to stop this orgy of destruction”.

The destruction to which Gueterres refers spans the globe and is happening on a massive scale. According to a UN Global Land Outlook assessment, more than 1 million species are now threatened with extinction, vanishing at a rate not seen in 10 million years. As much as 40% of Earth’s land surfaces are considered degraded.

Research by the International Union for the Conservation of Nature found that human activity for food production, infrastructure, energy and mining accounts for 79% of the impact on threatened species.

Human systems for food, infrastructure and energy are destroying biodiversity. Image: WEF/IUCN

Creating a nature-positive economy

Only by fundamentally transforming these systems can we shift from destructive human activity to a nature-positive economy. The World Economic Forum’s New Nature Economy Report II sets out a range of transitions that will reverse nature loss and pull us back from the brink. Without these changes, the world will suffer irreversible destruction of biodiversity that will have far-reaching impacts on the economy and all life on Earth.

The report delivers a stark warning about the risks we are creating by destroying nature, stating that “$44 trillion of economic value generation – over half the world’s total GDP – is potentially at risk as a result of the dependence of business on nature and its services”.

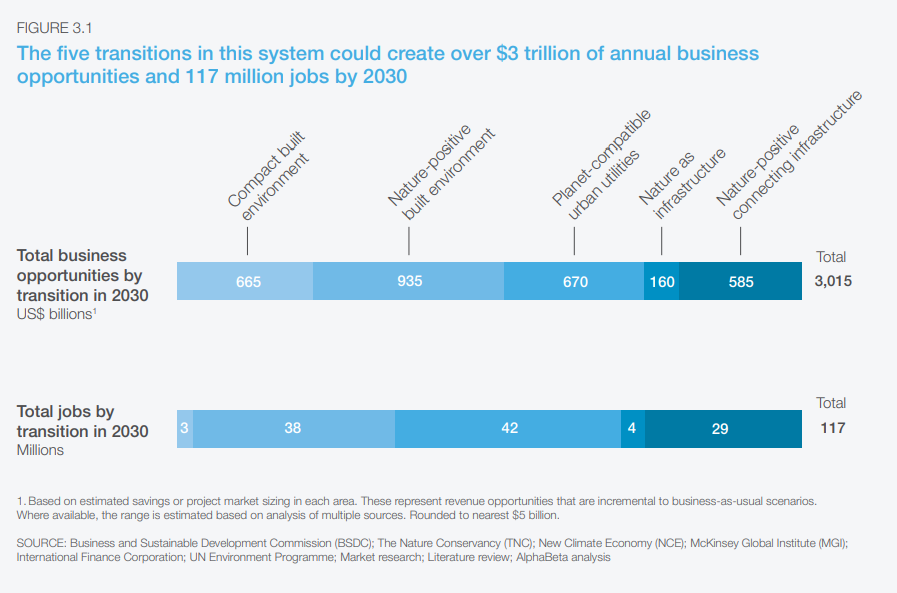

Five key transitions in the global economy could have a dramatic impact in slowing the loss of biodiversity, while bringing trillions of dollars of new economic opportunities and creating more than 100 million jobs.

Five key transitions in the global economy could have a dramatic impact in slowing the loss of biodiversity. Image: WEF New Nature Economy Report II

These transitions are:

1. Compact built environment

Higher-density urban development will free up land for agriculture and nature. It can also reduce urban sprawl, which destroys wildlife habitats and flora and fauna. Existing cities and settlements should be considered for strategic densification. Conservation-management projects should be established to protect biodiversity in areas that have been spared from development. This transition creates a $665 billion opportunity, with 3 million jobs created by 2030.

2. Nature-positive built environment

These built environments share space with nature. They are less human-centric, instead placing biodiversity at the core of project design. Infrastructure is located to avoid or minimize the destruction of nature, and all buildings are energy and resource efficient. Developments must include nature-friendly spaces and eco-bridges to connect habitats for urban wildlife. There’s a $935 billion opportunity in these built environments, and the possibility to create 38 million jobs by 2030.

3. Planet-compatible urban utilities

To stall biodiversity loss, we need utilities that effectively manage air, water and solid waste pollution in urban environments. In addition to benefiting nature, this will provide universal human access to clean air and water. Smart sensors and other Fourth Industrial Revolution technologies can transform urban utilities and make them planet-compatible. Creating them could deliver a $670 billion business opportunity and create 42 million jobs by 2030.

4. Nature as infrastructure

This transformation involves incorporating natural ecosystems into built-up areas. Instead of developments destroying floodplains, wetlands and forests, they would form an essential part of new built environments. This approach to development can also help deliver clean air, natural water purification and reduce the risk from extreme climate events. The business opportunity by using nature as infrastructure could hit $160 billion and create 4 million jobs by 2030.

5. Nature-positive connecting infrastructure

“Connecting infrastructure” includes roads, railways, pipelines and ports. Transitions in this area mean a change in the approach to planning to reduce biodiversity impacts, with a willingness to accept compromises when it comes to travel time and distance between departure point and destination. Building in wildlife corridors and switching to renewable energy in transport are key elements of nature-positive connecting infrastructure. The business opportunity here could peak at $585 billion, with the opportunity to create 29 million new jobs by 2030.

Time to make peace with nature

The outcomes of the COP15 biodiversity summit will shape the direction of humankind’s relationship with the natural world.

Costa Rica, once home to rampant logging, has now almost doubled the size of its rainforest. They turned it all around within a generation. It can be done.

António Guterres urged delegates to overcome their differences and reach agreement on protecting nature, telling the conference: “it’s time for the world to adopt a far-reaching biodiversity framework – a true peace pact with nature – and deliver a green, healthy future for all.”

Morocco has once again emerged as a leader in the Maghreb in matters of climate finance systems and regulation to support climate action, according to the “Climate Finance Readiness Index” report

The report, published recently by the Toronto and Casablanca-based consulting firm Green For South, highlighted that Morocco is, in its sub-region which also includes Algeria and Tunisia, the first to have adopted “appropriate regulations and guidelines (mostly voluntary at this stage), an interesting volume of climate finance activity (dealing with international funds and issuing green bonds) and effective awareness raising schemes.”

The report also highlighted Morocco’s efforts to improve its climate resilience, particularly in terms of mitigation, which requires significant investment, recalling in this regard the total cost of climate mitigation and adaptation actions included in the NDC (Nationally Determined Contribution) as published in June 2022. The amount is estimated at $78 billion, divided between mitigation measures ($38) and warning measures ($40 billion).

Tunisia also has appropriate regulation (on a voluntary basis), an interesting volume of climate finance activity, the report said, noting, however, that there has been no issuance of green bonds or “Sukuk” and awareness provisions are still limited.

As for Algeria, the report noted that the country “has no regulation in the financial sector to support climate action and that climate finance activity is still limited,” estimating that overall, the North African region is at an early stage of implementation of these actions.

For this firm specializing in sustainable finance, green and climate, Morocco and Tunisia are called to further strengthen their regulations and make them mandatory, and encourage green emissions and launch more awareness initiatives and training.

In the Middle East, Egypt is leading the way in making all ESG and climate risk regulations mandatory in the different financial sectors, namely banking, insurance, and capital markets, unlike countries like Jordan, Morocco, Tunisia, and Turkey that generally have voluntary reporting requirements.

The consulting Green for South firm, specializing in sustainable, green and climate finance, has evaluated in its Climate Finance Readiness Index report the regulations and measures taken by 14 countries in terms of climate finance. The assessment, covering 4 regions – North Africa, Middle East, Gulf and Turkey – takes into account the specificities of each territory and sets up appropriate criteria. With a score of 31.33%, the North African region shows promising results, with Morocco representing the most successful model.