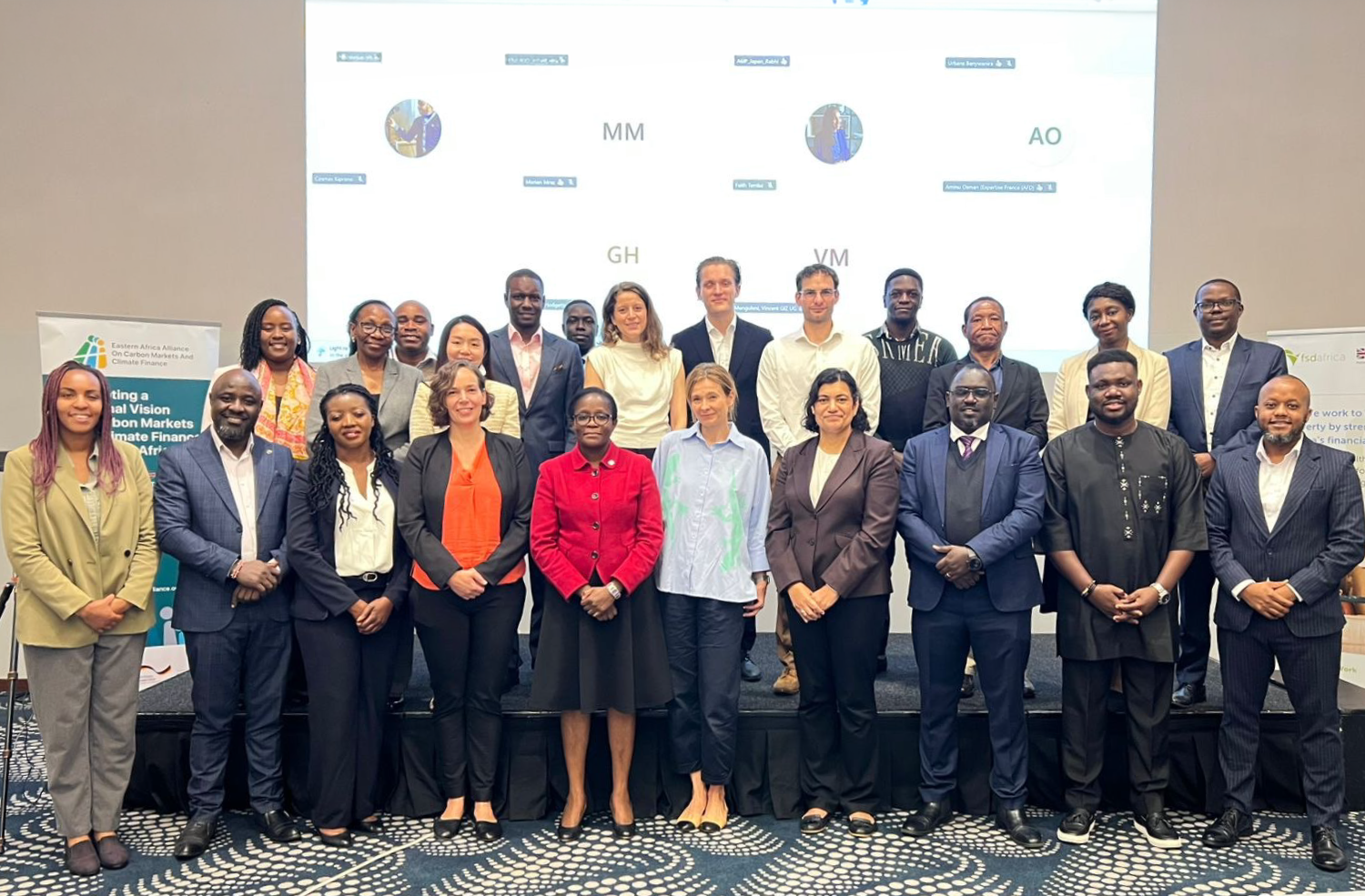

Representatives from donor agencies, development finance institutions, climate finance organisations, technical partners, and regional market initiatives during the Regional Donor Roundtable on Financing Readiness in Carbon Markets held in Nairobi on 7 May 2026. Photo FSD Africa.

Nairobi, Kenya – FSD Africa co-hosted a regional donor roundtable on financing readiness in African carbon markets in Nairobi on 7 May 2026, bringing together development partners, policymakers, technical organisations, and market actors to examine how stronger policy and regulatory environments can help unlock financing into African carbon markets.

Co-hosted with the Eastern Africa Carbon Alliance, the meeting brought together more than 30 senior representatives from donor agencies, climate finance organisations, and market ecosystem partners to discuss how the region can build more credible, coordinated, and investable carbon market ecosystems.

The discussions took place against a backdrop of shrinking development budgets and growing demand for support around carbon market regulation, institutional readiness, and implementation capacity. Participants agreed that stronger coordination across institutions will be essential if the region is to build functioning carbon markets capable of attracting long-term private investment.

The workshop included representatives from the World Bank, African Development Bank, United Nations Environment Programme, United Nations Development Programme, GIZ, European Union, JICA, and FCDO, alongside conservation organisations, technical assistance providers, and regional market initiatives.

Building more coordinated and investable carbon markets

Discussions focused on where financing and implementation gaps remain across the region, where support efforts overlap, and how institutions can work together more strategically to reduce duplication and strengthen regional impact. Participants also explored how support in one country or initiative could potentially be leveraged into others through stronger partnerships and coordinated approaches.

A strong theme throughout the discussions was the need for deeper collaboration across the ecosystem to improve efficiency, reduce duplication, and strengthen the overall impact of support being provided across the region.

Stakeholders also expressed strong interest in exploring a more structured platform that could improve visibility across country readiness efforts, ongoing interventions, partnership opportunities, and outstanding financing gaps. Participants noted that clearer coordination and transparency could help strengthen investor confidence while improving how support is deployed across the market ecosystem.

Reshma Shah said the discussions reinforced growing recognition that policy and regulatory stability are no longer secondary considerations in carbon markets, but central determinants of whether markets succeed in attracting investment.

Across our engagements with financial institutions, there is clear interest from banks, insurers, pension funds, and investors…But carbon markets continue to be perceived as high risk, with policy and regulatory uncertainty remaining one of the main drivers of that risk perception

She added that carbon markets represent a potentially important mechanism for mobilising climate finance across the region, but that stronger institutional coordination and clearer market signals will be needed if countries are to move from fragmented pilot activity toward functioning and investable markets.

A changing funding landscape

Reflecting on the discussions, Mark Napier noted that tightening aid budgets are forcing organisations to think more carefully about where catalytic support can have the greatest impact.

This is a good illustration of how shrinking aid budgets are forcing everyone to focus on the most salient issues

he said following the roundtable discussions.

Napier also reflected on the importance of understanding where meaningful capital and ecosystem support is emerging across the sector, particularly as countries seek to build enough scale and coordination to make carbon markets viable over the long term. He pointed to the potential for countries such as Ethiopia to emerge as important testing grounds for carbon market development where sustained commitments, ecosystem coordination, and market activity begin to reach critical mass.

Strengthening the enabling environment for investment

For FSD Africa, the convening reinforced the role the organisation can play in helping connect policy readiness and market infrastructure directly to capital mobilisation outcomes. Rather than focusing on detailed policy implementation work, the organisation’s role is to help build the enabling conditions that improve investor confidence and connect policy, projects, and financial markets into clearer investment pathways.

The group agreed to reconvene virtually in the coming weeks to review consolidated workshop outputs and identify priority areas for collaboration going forward.