Pre-seed venture capital (VC) fund and accelerator Catalyst Fund has announced a $2 million investment in 10 startups developing solutions to improve the resilience of communities most vulnerable to climate change in Africa.

This is the first cohort of startups to receive funding from Catalyst Fund’s new $30M investment fund, backed by the financial sector development agency FSD Africa, aimed at helping early-stage founders develop technologies that will make Africa less susceptible to the impact of climate change.

These companies join Catalyst Fund’s existing portfolio in emerging markets which is made up of 61 startups. Catalyst Fund’s portfolio companies have so far raised more than US$640 million in follow-on financing and their solutions have already benefited more than 14 million people and small and medium-sized businesses worldwide.

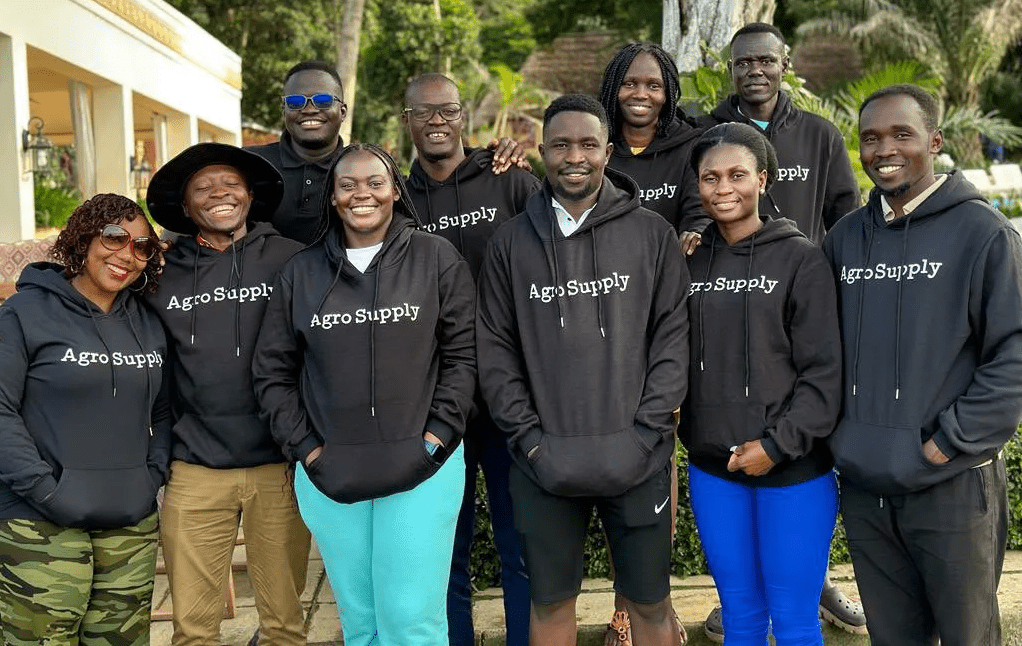

The startups include Eight Medical, Farmz2U, and PaddyCover from Nigeria, Farm to Feed and Octavia Carbon from Kenya, Bekia and VAIS from Egypt, Agro Supply from Uganda, Assuraf from Senega, and agroforestry startup Sand to Green from Morocco.

“We are delighted to have the opportunity to invest and support these ten African startups who are working through their innovative solutions to build a more resilient and sustainable future,” said Maelis Carraro, partner, and director of Catalyst Fund.

“Our goal is to support entrepreneurs who share our vision of a world in which everyone has the tools and opportunities they need to thrive. From AgTech and InsurTech, to waste management, natural disaster response, and carbon finance, these startups showcase technology and business model innovations that will help communities better adapt. to climate impacts and to increase their resilience,” Carraro explained further in a press statement.

Each of the 10 startups received $100,000 in capital investments as well as $100,000 in personalized support from Catalyst Fund experts aimed at accelerating their growth. In addition, each startup may be offered direct relationships with investors and talent networks that allow them to evolve.

Agro Supply Limited has developed a layaway system that makes use of a USSD code and scratch cards plus mobile money to enable farmers to save for agricultural inputs.

Catalyst Fund recently announced its first investments in ten African startups that are leading the way in areas like agtech, insurtech, waste management, disaster response, and carbon finance. The goal is to help communities adapt to the effects of climate change and build their resilience.

This is the first group of entrepreneurs to get help from its new $30 million pre-seed venture capital fund and accelerator. Its first partner, FSD Africa, is the fund’s leader, and the fund’s goal is to support high-impact entrepreneurs who are working to help underserved, climate-vulnerable communities in Africa become more resilient.

Catalyst Fund’s goal is to help entrepreneurs who use new ideas in technology, finance, and data to solve the biggest problems and take advantage of the biggest opportunities of our time. To do this, it has expanded its mission to include investing in businesses that tackle climate change, which is the biggest problem we all face.

Catalyst Fund already has 61 companies in emerging markets in its portfolio. These new startups will join them and get money, expert-led help building their businesses, and access to a network of investors, corporate innovators, and talented people who can help them grow.

Today pre-seed venture capital (VC) fund and accelerator Catalyst Fund announced a $2 million investment into 10 startups building solutions to improve the resilience of climate-vulnerable communities in Africa.

This is the first group of companies to get money from Catalyst Fund’s new $30 million venture capital fund, which is led by the financial sector development agency FSD Africa. The goal of the fund is to help early-stage founders create technology that will make Africa more resistant to the effects of climate change.

Each of the ten firms will receive $100,000 in equity investments as well as $100,000 in hands-on venture-building assistance.

These companies will join Catalyst Fund’s existing portfolio of 61 startups in emerging markets. They will get funding, specialized and expert-led help building their businesses, and direct connections to investors, corporate innovators, and talent networks that can help them grow.

Catalyst Fund’s Managing Partner, Maelis Carraro, said, “We are thrilled to be able to work with ten innovative African startups to build a more resilient and sustainable future.”

Our goal is to help mission-driven founders who share our vision of a world where everyone has the tools and opportunities they need to thrive. From agtech to insurtech, waste management to disaster response, and carbon finance to carbon finance, these startups show finance, tech, and business model innovations that will help communities better adapt to climate change and become more resilient.

Here are the top ten startups.

Agro Supply (Uganda)

A mobile layaway system that helps farmers save money slowly using their cell phones and cash out to buy farm inputs like hybrid (drought-resistant) seeds, from maize to sorghum, sunflower, and soybean, during planting season.

Assaraf (Senegal)

A digital insurtech platform that gives end users accesses to a variety of insurance products from more than 20 insurance companies, such as insurance for agriculture, cars, health, homes, and natural disasters. It also has a fully integrated claims management system.

Bekia (Egypt)

A technologically advanced waste management solution that enables businesses and households to trade in their waste (including plastic, paper, electronics, metals, and cooking oil) for cash rewards paid to a digital wallet.

Eight Medical (Nigeria)

A cloud-based platform for Emergency Medical Services (EMS) that lets people get urgent care when and where they need it.

This “911 for Africa” puts emergency medical workers on motorcycles in touch with people in trouble in 10 minutes or less, even if the problem is caused by the weather.

Farm to Feed (Kenya)

Afirm n the food supply chain that offers a digitally enabled solution to food loss/waste. Their environmentally friendly strategy focuses on giving farmers a market for their surplus and imperfect produce, improving food security, and lowering greenhouse gas emissions.

Farmz2U (Nigeria + Kenya)

An agtech company promoting sustainable agriculture. Farmers can obtain individualized farming guidance (particularly on regenerative farming practices), reasonable loans, quality and traceable inputs, and direct customers for their harvest through Farmz2U.

Octavia Carbon (Kenya)

Global South’s first Direct Air Capture (DAC) firm is constructing the world’s most affordable DAC hub.

Octavia is building DAC equipment to pull carbon out of the air and sell it to off-takers as either carbon dioxide or carbon credits.

Paddy Cover (Nigeria)

Works with established insurers and digital platforms to create and sell customized products through their platform. These products include health, life, and index-based crop insurance, which will be available in the future.

The services are built into the customer’s life in some way, either as a convenience or as a way to add value.

Sand to Green (Morocco)

Using agroforestry and a solar-powered desalination system, they turn deserts into land that can be used for farming. They also design climate-smart regenerative farms.

VAIS (Egypt)

A precision agtech startup dedicated to climate resilience and food security by giving farms data intelligence through their FarmGATE application, which is powered by proprietary artificial intelligence/machine learning (AI/ML)-based virtual field probing (VFP) technology. This helps farms make better use of water and other farm inputs to get better yields.

Catalyst Fund’s portfolio companies have raised more than US$640 million in follow-on funding so far, and they now serve more than 14 million individuals and MSMEs around the world.

Three Nigerian tech startups, PaddyCover, Farmz2U, and Eight Medical, have secured a total of $600,000 from pre-seed venture capital and accelerator Catalyst Fund.

This breaks down to $200,000 each for each of the three startups to scale their businesses.

The funding was part of a $2 million investment into 10 startups building solutions to improve the resilience of climate-vulnerable communities in Africa.

Each of the 10 startups is offered $100,000 of equity investments as well as $100,000 of hands-on venture-building support.

According to the VC, this is the inaugural cohort of the new $30 million VC fund of Catalyst Fund, anchored by financial sector development agency FSD Africa, aimed at supporting early-stage founders to develop technology that will make Africa more resilient to the impacts of climate change.

Who they are: The three Nigerian startups benefiting from the funding cover insurtech, agtech, and medtech.

PaddyCover works with established insurers and digital platforms to design and offer bespoke products via their platform that facilitates flexible insurance packages, including health, life, and, in the future, index-based crop insurance. The offerings are built into the lifestyle touchpoints of the customer, either as a convenience or as complementary value-adds.

Farmz2U is an agtech enterprise driving sustainable agriculture. Through Farmz2U, farmers can access personalized farming advice (especially on regenerative farming practices), affordable credit, quality and traceable inputs, and direct buyers for their harvest.

Eight Medical is a cloud-native Emergency Medical Services (EMS) platform that provides on-demand urgent care when and where it is needed. This “911 for Africa” connects emergency medical responders on motorcycles to users in distress in 10 minutes or less, including for climate-induced crises.

The goal of the Fund: While expressing the Fund’s excitement in partnering with groundbreaking African startups working to build a more resilient and sustainable future, the Managing Partner of Catalyst Fund, Maelis Carraro said:

“Our goal is to back mission-driven founders that share our vision of a world where every individual has the tools and opportunities they need to thrive. From agritech to insurtech, waste management, disaster response, and carbon finance, these startups display finance, tech, and business model innovations that will help communities better adapt to climate impacts and grow their resilience.”

Other African startups that received the investment include Agro Supply from Uganda, Assuraf from Senegal, Bekia from Egypt, Farm to Need from Kenya, Octavia Carbon, also from Kenya, Sand to Green from Morocco, and VAIS from Egypt. Only Nigeria has up to three startups in the cohort.

Financial Sector Deepening Africa (FSD Africa) will be quantifying changes in credit risk under different nature and climate scenarios for African central banks this year, the Kenya-based development agency’s director of risk, Kelvin Massingham, told Responsible Investor.

Massingham was speaking to RI after FSD Africa was selected to deliver the UK government’s Nature Positive Economy programme, alongside the UNDP’s Biodiversity Finance Initiative (BioFin).

Established in 2012, FSD Africa is a non-profit company funded by the UK’s Department for International Development, which aims to promote financial sector development across sub-Saharan Africa.

The aim of the £7.2m Nature Positive Economy initiative, which was announced at COP15 in Montreal last year, is to support the transition of developing countries to nature-positive economies.

Massingham explained that FSD Africa will collaborate with six unnamed central banks in some of Africa’s largest economies and hopes to build upon work already done by the Dutch and French central banks.

Last year, the non-profit used publicly available central bank data to do nature stress tests for Zambia, Ghana, Kenya, South Africa, Egypt and Mauritius.

FSD Africa will also collaborate with the World Bank and BioFin to create a working group focused on central bank stress testing regarding nature, Massingham said.

In particular, it will centre on sharing learnings across geographies, creating knowledge briefs, and feeding into the work of global coalitions such as the Network for Greening the Financial System (NGFS).

As the group has not yet launched, no banks have formally joined.

FSD Africa also works with other players in the financial sector. It is currently conducting pilots of the Taskforce on Nature Related Disclosures (TNFD) with six entities in the banking and insurance sectors, and will look to increase that to 20 this year.

Massingham said: “During initial piloting of TNFD, when the financial institutions did their assessment, although they of course found nature to be a material risk for their portfolios, they all identified it as a major opportunity.”

Specifically, some banks are apparently looking at the potential for biodiversity bonds.

FSD Africa is also working with financial regulators in Kenya, Nigeria, Ghana and Egypt on how they can signal to their markets that nature-related financial disclosures are coming, in line with the commitment made by signatory countries in Target 15 of the Kunming-Montreal Global Biodiversity Framework.

Each of the 10 startups will be offered $100K of equity investments as well as $100K of hands-on venture-building support.

These ten companies will join Catalyst Fund’s portfolio of 61 startups across emerging markets and receive capital, bespoke and expert-led venture-building support.

The Catalyst Fund has announced a $2 million investment into 10 African startups building solutions to improve the resilience of climate-vulnerable communities in Africa.

The Catalyst Fund is a pre-seed venture capital (VC) fund and accelerator that backs high-impact startups that seek to improve the resilience of underserved, climate-vulnerable communities.

This is the inaugural cohort of the new $30 million VC fund of Catalyst Fund that is anchored by the financial sector development agency, FSD Africa.

It is aimed at supporting early-stage founders to develop technology that will make Africa more resilient to the impacts of climate change.

Catalyst Fund managing partner Maelis Carraro said that they are thrilled to have the opportunity to partner with ten African startups working to build a sustainable future.

“Our goal is to back mission-driven founders that share our vision of a world where every individual has the tools and opportunities they need to thrive,” Carraro said.

“From agritech to insurtech, waste management, disaster response, and carbon finance, these startups display finance, tech, and business model innovations that will help communities better adapt to climate impacts and grow their resilience.”

Each of the 10 startups will be offered $100K of equity investments as well as $100K of hands-on venture-building support.

These ten companies will join Catalyst Fund’s portfolio of 61 startups across emerging markets and receive capital, bespoke and expert-led venture-building support.

They will also receive direct connections with investors, corporate innovators, and talent networks that can help them scale.

The Fund’s portfolio companies have raised more than US$640 million in follow-on funding to date, and currently serve more than 14 million individuals and MSMEs globally.

The ten companies joining this next cohort of Catalyst Fund are Agro Supply (Uganda), Assuraf (Senegal), Bekia (Egypt), Eight Medical (Nigeria), Farm to Feed (Kenya), Farmz2U ( Nigeria, Kenya), Octavia Carbon (Kenya), PaddyCover (Nigeria), Sand to Green Morocco and VAIS (Egypt).

FSD Africa Digital Economy director Juliet Munro said that these companies are strong examples of the innovation needed to enhance the resilience of vulnerable communities across the continent.

“At FSD Africa, we believe that by harnessing the power of tech, and specifically fintech innovation, we can help to spur the development of climate resilience solutions for Africa, thereby helping deliver on COP27’s core themes of adaptation and implementation,” Juliet said.

Catalyst Fund Partner Aaron Fu said that COP27 in Egypt called for more private sector financing to fill the $330B funding gap for adaptation and resilience by 2030.

Aaron also said that it called for more local innovations to support communities in building resilience to climate impacts.

“The Catalyst Fund’s new cohort exemplifies what these innovative climate solutions for the most vulnerable could look like,” he added.

He also said that they are also thrilled to be backing companies in Francophone Africa and Northern Africa for the first time.

Catalyst Fund intends to back many more startups like them across the African continent in the years to come.

NAIROBI, Kenya, 10 January 2023 -/African Media Agency(AMA)/- Today pre-seed venture capital (VC) fund and accelerator Catalyst Fund announced a $2 million investment into 10 startups building solutions to improve the resilience of climate-vulnerable communities in Africa. This is the inaugural cohort of the new $30M VC fund of Catalyst Fund, anchored by financial sector development agency FSD Africa, aimed at supporting early-stage founders to develop technology that will make Africa more resilient to the impacts of climate change.

Each of the 10 startups will be offered $100K of equity investments as well as $100K of hands-on venture-building support.

These companies will join Catalyst Fund’s existing portfolio of 61 startups across emerging markets and receive capital, bespoke and expert-led venture-building support, and direct connections with investors, corporate innovators and talent networks that can help them scale. Catalyst Fund’s portfolio companies have raised over US$640 million in follow-on funding to date, and currently serve more than 14 million individuals and MSMEs globally.

“We are thrilled to have the opportunity to partner with ten groundbreaking African startups working to build a more resilient and sustainable future,” said Maelis Carraro, Managing Partner of Catalyst Fund. “Our goal is to back mission-driven founders that share our vision of a world where every individual has the tools and opportunities they need to thrive. From agtech to insurtech, waste management, disaster response, and carbon finance, these startups display finance, tech, and business model innovations that will help communities better adapt to climate impacts and grow their resilience.”

The ten companies joining this next cohort of Catalyst Fund are:

Agro Supply [Uganda]: a mobile layaway system that helps farmers save money gradually using their mobile phones and to cash out in order to purchase farm inputs such as hybrid (drought-resistant) seeds, from maize to sorghum, sunflower and soybean during the planting season.

Assuraf [Senegal]: a digital insurtech platform offering end-users access to a range of insurance products (e.g. agriculture, automotive, health, housing, natural disasters) from over 20+ insurance companies with a fully integrated claims management system.

Bekia[Egypt]: a tech-enabled waste collection solution enabling companies and households to exchange their waste (plastic, paper, electronics, metals, cooking oil) against a financial incentive paid on a digital wallet.

Eight Medical [Nigeria]: a cloud-native Emergency Medical Services (EMS) platform that provides on-demand urgent care when and where it is needed. This “911 for Africa” connects emergency medical responders on motorcycles to users in distress in 10 minutes or less, including for climate-induced crises.

Farm to Feed [Kenya]: a food supply chain company that is providing a digitally-enabled solution to food loss/waste. Their climate-smart solution focuses on providing a market for imperfect and surplus produce from farmers, contributing to food security and greenhouse gas emissions reduction.

Farmz2U [Nigeria, Kenya]: an agtech enterprise driving sustainable agriculture. Through Farmz2U, farmers can access personalized farming advice (especially on regenerative farming practices), affordable credit, quality and traceable inputs, and direct buyers for their harvest.

Octavia Carbon [Kenya]: the Global South’s first Direct Air Capture (DAC) company that is building the world’s lowest-cost DAC hub. Octavia is currently building DAC machinery to capture carbon from the air for resale as either carbon dioxide or carbon credits to off-takers.

PaddyCover [Nigeria]: works with established insurers and digital platforms to design and offer bespoke products via their platform that facilitates flexible insurance packages, including health, life and, in the future, index-based crop insurance. The offerings are built into the lifestyle touchpoints of the customer, either as a convenience or as complementary value-adds.

Sand to Green [Morocco]: transforms deserts into cultivable land using agroforestry methodology and a solar-powered desalination system to design climate-smart regenerative farms.

VAIS [Egypt]: a precision agtech startup committed to climate resilience and food security by providing data intelligence to farms via their FarmGATE application, which is powered by proprietary artificial intelligence/machine learning (AI/ML)-based virtual field probing (VFP) technology, to enable better use of water and other farm inputs to produce better yields.

“At FSD Africa, we believe that by harnessing the power of tech, and specifically fintech innovation, we can help to spur the development of climate resilience solutions for Africa, thereby helping deliver on COP27’s core themes of adaptation and implementation,” said Juliet Munro, Director of Digital Economy at FSD Africa. “These companies are strong examples of the innovation we need to enhance the resilience of vulnerable communities in across the continent.”

“COP27 in Egypt this year called for more private sector financing to fill the >$330B funding gap for adaptation and resilience by 2030. It also called for more local innovations to support communities in building resilience to climate impacts. The Catalyst Fund’s new cohort exemplifies what these innovative climate solutions for the most vulnerable could look like. We are also thrilled to be backing companies in Francophone Africa and Northern Africa for the first time. We intend to back many more startups like them across the African continent in the years to come,” said Aaron Fu, Partner at Catalyst Fund.

The Catalyst Fund is a pre-seed VC fund and accelerator backing high-impact tech startups that seek to improve the resilience of underserved, climate-vulnerable communities. We partner with mission-driven founders that share our vision of a world where every individual has the tools and opportunities they need to thrive.

NAIROBI, Kenya, 10 January 2023 -/African Media Agency(AMA)/- Today pre-seed venture capital (VC) fund and accelerator Catalyst Fund announced a $2 million investment into 10 startups building solutions to improve the resilience of climate-vulnerable communities in Africa. This is the inaugural cohort of the new $30M VC fund of Catalyst Fund, anchored by financial sector development agency FSD Africa, aimed at supporting early-stage founders to develop technology that will make Africa more resilient to the impacts of climate change.

Each of the 10 startups will be offered $100K of equity investments as well as $100K of hands-on venture-building support.

These companies will join Catalyst Fund’s existing portfolio of 61 startups across emerging markets and receive capital, bespoke and expert-led venture-building support, and direct connections with investors, corporate innovators and talent networks that can help them scale. Catalyst Fund’s portfolio companies have raised over US$640 million in follow-on funding to date, and currently serve more than 14 million individuals and MSMEs globally.

“We are thrilled to have the opportunity to partner with ten groundbreaking African startups working to build a more resilient and sustainable future,” said Maelis Carraro, Managing Partner of Catalyst Fund. “Our goal is to back mission-driven founders that share our vision of a world where every individual has the tools and opportunities they need to thrive. From agtech to insurtech, waste management, disaster response, and carbon finance, these startups display finance, tech, and business model innovations that will help communities better adapt to climate impacts and grow their resilience.”

The ten companies joining this next cohort of Catalyst Fund are:

Agro Supply [Uganda]: a mobile layaway system that helps farmers save money gradually using their mobile phones and to cash out in order to purchase farm inputs such as hybrid (drought-resistant) seeds, from maize to sorghum, sunflower and soybean during the planting season.

Assuraf [Senegal]: a digital insurtech platform offering end-users access to a range of insurance products (e.g. agriculture, automotive, health, housing, natural disasters) from over 20+ insurance companies with a fully integrated claims management system.

Bekia[Egypt]: a tech-enabled waste collection solution enabling companies and households to exchange their waste (plastic, paper, electronics, metals, cooking oil) against a financial incentive paid on a digital wallet.

Eight Medical [Nigeria]: a cloud-native Emergency Medical Services (EMS) platform that provides on-demand urgent care when and where it is needed. This “911 for Africa” connects emergency medical responders on motorcycles to users in distress in 10 minutes or less, including for climate-induced crises.

Farm to Feed [Kenya]: a food supply chain company that is providing a digitally-enabled solution to food loss/waste. Their climate-smart solution focuses on providing a market for imperfect and surplus produce from farmers, contributing to food security and greenhouse gas emissions reduction.

Farmz2U [Nigeria, Kenya]: an agtech enterprise driving sustainable agriculture. Through Farmz2U, farmers can access personalized farming advice (especially on regenerative farming practices), affordable credit, quality and traceable inputs, and direct buyers for their harvest.

Octavia Carbon [Kenya]: the Global South’s first Direct Air Capture (DAC) company that is building the world’s lowest-cost DAC hub. Octavia is currently building DAC machinery to capture carbon from the air for resale as either carbon dioxide or carbon credits to off-takers.

PaddyCover [Nigeria]: works with established insurers and digital platforms to design and offer bespoke products via their platform that facilitates flexible insurance packages, including health, life and, in the future, index-based crop insurance. The offerings are built into the lifestyle touchpoints of the customer, either as a convenience or as complementary value-adds.

Sand to Green [Morocco]: transforms deserts into cultivable land using agroforestry methodology and a solar-powered desalination system to design climate-smart regenerative farms.

VAIS [Egypt]: a precision agtech startup committed to climate resilience and food security by providing data intelligence to farms via their FarmGATE application, which is powered by proprietary artificial intelligence/machine learning (AI/ML)-based virtual field probing (VFP) technology, to enable better use of water and other farm inputs to produce better yields.

“At FSD Africa, we believe that by harnessing the power of tech, and specifically fintech innovation, we can help to spur the development of climate resilience solutions for Africa, thereby helping deliver on COP27’s core themes of adaptation and implementation,” said Juliet Munro, Director of Digital Economy at FSD Africa. “These companies are strong examples of the innovation we need to enhance the resilience of vulnerable communities in across the continent.”

“COP27 in Egypt this year called for more private sector financing to fill the >$330B funding gap for adaptation and resilience by 2030. It also called for more local innovations to support communities in building resilience to climate impacts. The Catalyst Fund’s new cohort exemplifies what these innovative climate solutions for the most vulnerable could look like. We are also thrilled to be backing companies in Francophone Africa and Northern Africa for the first time. We intend to back many more startups like them across the African continent in the years to come,” said Aaron Fu, Partner at Catalyst Fund.

The Catalyst Fund is a pre-seed VC fund and accelerator backing high-impact tech startups that seek to improve the resilience of underserved, climate-vulnerable communities. We partner with mission-driven founders that share our vision of a world where every individual has the tools and opportunities they need to thrive.

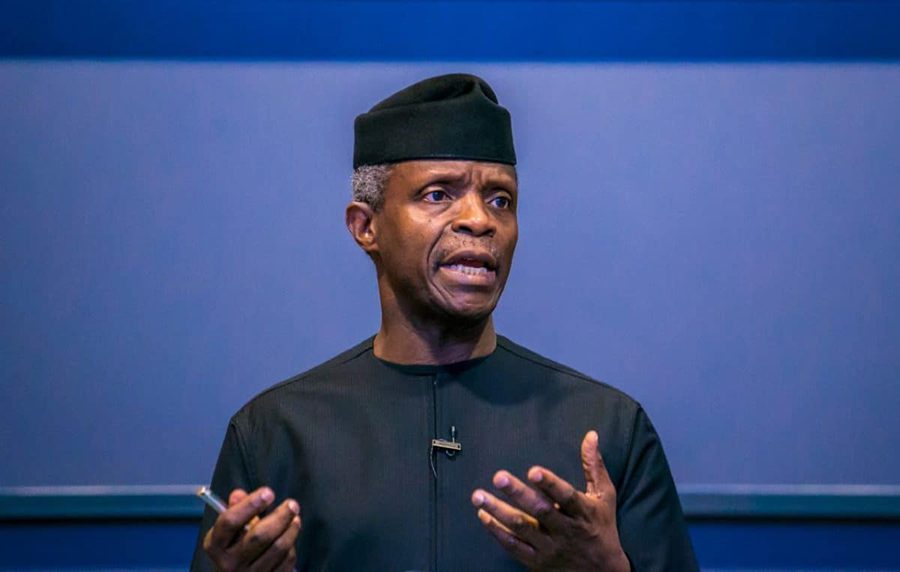

Nigeria’s Vice President, Prof. Yemi Osinbajo, said Africa’s share of the global carbon market can be scaled up massively to reach foreign direct investment (FDI) of between $120 to $200 billion annually.

The Vice President stated this during his keynote speech at the Rockefeller Foundation meeting in New York.

He identified a combination of capital flows, job creation, and the avoidance of long-term climate destruction as critical drivers of African leaders’ interest in supporting this effort.

According to him, Africa currently has only a small share of the carbon market. He explained the importance of this projected carbon finance stream, saying:

“For a continent that needs $240 billion annually in mitigation investment alone, this carbon finance stream could be the difference between transitioning and not (transitioning). As all of us in this room understand well, the priorities of the African continent are not just to act decisively on the climate crisis, but to also create significant growth opportunities for our young and growing population.”

“The investment required to advance the energy transition in Africa is huge. World Bank estimates suggest that Africa needs $6.5 trillion US dollars between now and 2050 for mitigation action alone to keep temperatures below 2 degrees of warming.”

VP Osinbajo also highlighted that the carbon market pipeline could create 30 million jobs in the next decade, with the potential to create more than 100 million jobs through climate-aligned projects by 2050.

Africa’s carbon markets: During his speech, VP Osinbajo noted that the rapid progress recorded in Africa benefitted from the support of a very engaged Steering Committee with the United Nations, Global Energy Alliance for People and Planet (GEAPP), USAID, and a range of other public and private actors, which resulted in the successful launch of the African Carbon Markets initiative (ACMI) in Sharm-el-Sheikh, Egypt during the COP-27 event.

“The strong commitment and presence from fellow African leaders demonstrate the willingness and leadership of Africa. We already have 7 African countries (Burundi, Gabon, Kenya, Malawi, Mozambique, Nigeria, and Togo) signed up to develop country carbon activation plans and over $200 million in advanced market commitments, which we must continue to further advance as this is going to be the critical driver of action on the continent.”

“I think it’s an auspicious moment for Africa to be participating more fully in the global carbon market conversation, especially in the light of the slowing pace of green investment flows into the continent. The work several of us have done together in the past few months makes it clear that while other sources of flows are slowing down globally, carbon markets are growing rapidly,” Osinbajo said.

Advancing carbon markets: VP Osinbajo also spoke about the essence of collaborations in developing carbon markets on the continent. He said collaboration is a key to unlocking opportunities in Africa’s carbon markets. He said:

“One of the strong points of ACMI and the way we must structure it going forward, in terms of governance, is the flexibility to smoothly work with other initiatives, and there will be many others. Two days before the opening of Cop 27, Senator John Kerry and I had a conversation about the proposed Energy Transition Accelerator and we both agreed that once the details were worked out, we would work out a collaborative framework with ACMI.

“Carbon markets will play a critical role in the implementation of this (Energy Transition) Plan – in mobilizing the capital required to move to our net-zero economy-wide trajectory. I want Nigeria to have the first Carbon Markets Activation Plan.”

In his contribution, the US Presidential Envoy on Climate Change, Senator John Kerry, commended VP Osinbajo for his leadership on the issue of energy transition. Kerry said:

“We are grateful for the leadership of the VP, grateful for the reception you gave me on my visit to Nigeria. I am honoured to share the platform with you on how to move the African Carbon Market Initiative (ACMI) forward.

“It is possible to create a high-integrity carbon market in a way to address Climate Change and African Development aspirations. We are all joined together looking forward to developing the financing.”

In case you missed it: The ACMI is a new initiative that was launched during the conference of parties (COP 27) event held in Egypt. The ACMI will be led by a fourteen-member steering committee of African leaders, CEOs, and carbon credit experts. The ACMI aims to dramatically expand Africa’s participation in voluntary carbon markets.

COP27 may be over but its impact will be felt for many decades to come.

Discussions highlighted nature’s pivotal role in tackling the climate crisis.

Here we reflect on 10 areas where progress is being made on climate action.

The implications of COP27 will likely be felt for decades to come, for better or worse. While a broad range of analysis has already been published on the ultimate outcomes of COP27, this summary includes reflections on how nature was the stand out topic at COP27 – here are the top ten takeaways.

1. Calls for structural reform of finance for nature and climate

It was impossible to pass a day at COP27 without having a conversation about finance – but finance means different things to different people. The breakthrough on loss and damage funding made the headlines, but this year there was much attention on structural reform of the financial system as well as the need to create innovative mechanisms that support nature and climate outcomes at national and ecosystem levels.

The Bridgetown agenda remained a central theme within these discussions. Before COP27, there was much focus on the need for financing adaptation measures – although in fact, very little progressed on this agenda from Glasgow. The multilateral development banks are also under scrutiny – sovereign bonds and sustainability-linked loans and bonds have been high on the agenda. Leading financial institutions from Japan to Norway to Brazil, all signatories to the Financial Sector Commitment on Eliminating Commodity-driven Deforestation have been moving forward with implementation through the Finance Sector Deforestation Action (FSDA) initiative.

FSDA members have published shared investor expectations for companies, and they are stepping up engagement activity and are working with policymakers and data providers. More broadly, the 10 point plan for financing biodiversity moved ahead at COP27 with a ministerial meeting between 16 countries representing five continents to set a pathway for bridging the global biodiversity finance gap – and looking ahead to the biodiversity COP15 in December 2020.

2. Biodiversity COP15 looms large

The biodiversity COP is usually a distant cousin to the climate COP, but in Egypt there was a considerable amount of attention on the need to create a “sister agreement” – a Paris moment for nature. The messaging that the climate and nature crises are deeply linked was made loud and clear at COP27.

On Biodiversity Day, the Paris climate champions urged leaders to step up action to address the accelerating loss of nature by delivering an ambitious biodiversity agreement at COP15 in Montreal. On the same day, more than 340 civil society leaders called on governments to prioritise the biodiversity COP, and a new survey from more than 400 experts from 90 countries revealed that a shocking 88% believe that the state of the world’s nature is “alarming” or “catastrophic and potentially irreversible”.

However, even though many countries were pushing for COP15 to be included in the COP27 text, the attempt failed – a disappointing outcome as net-zero emissions will not be enough to limit rapidly rising temperatures. Governments also need to halt and reverse biodiversity loss by 2030.

3. Strong signs of political will for forests

The creation of the Forest and Climate Leaders’ Partnership (FCLP), announced at the World Leaders’ Summit, is being driven by the reality that there is no time to lose when it comes to halt and reverse forest loss by 2030, with the intent to demonstrate success by COP28. The leaders of the 28 – and counting – FCLP member countries serve as key actors in the partnership, and its ultimate priority setters.

The FCLP will hold regular meetings, including leader-level moments at the beginning of climate COPs to encourage accountability. Starting in 2023, the FCLP will also publish an annual Global Progress Report that includes independent assessments of global progress toward the 2030 goal, as well as summarising progress made by the FCLP itself, including in its action areas and initiatives.

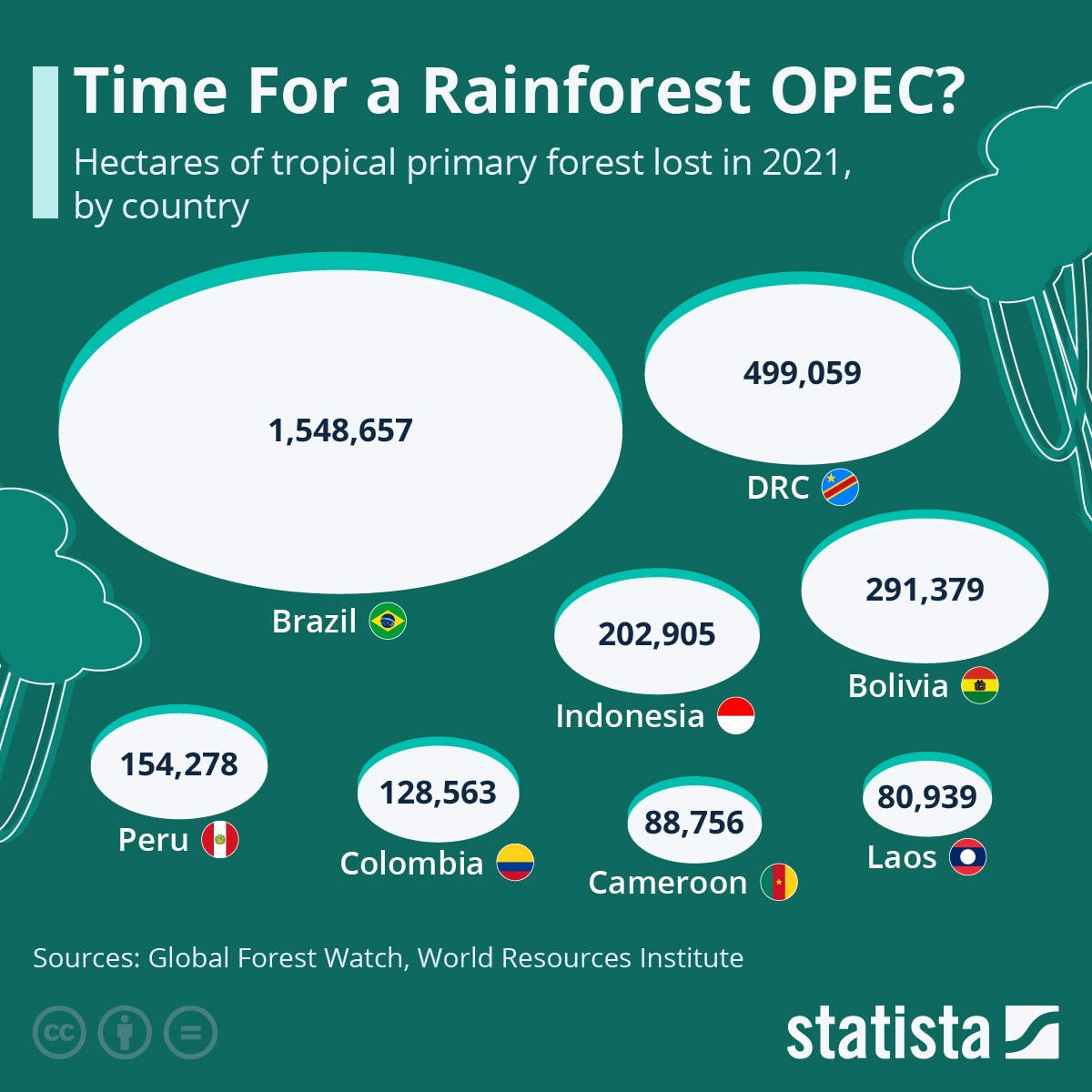

The presence of Brazil’s president elect, Luiz Inacio Lula da Silva, put a spotlight on the Amazon at COP27 – with Brazil promising to prioritise stopping deforestation and offering to host COP30 in three years’ time. Also, an announcement by Brazil, Indonesia and the Democratic Republic of Congo – made in Indonesia ahead of the G20 – signalled their intentions to work together to protect their vast swathes of tropical forests, earning the nickname “the OPEC of rainforests”.

This chart shows the total hectares of forest that have been destroyed in different countries. Source: Statista.

4. Implementation of forest pledges

Coming into COP27, there were clear signs that the global community is not yet on track to halt and reverse forest loss and degradation by 2030. Another UN-led report found that for 2030 goals to remain within reach, a one gigaton milestone of emissions reductions from forests must be achieved not later than 2025, and yearly after that, but that current public and private commitments to pay for emissions reductions are only at 24% of the gigaton milestone goal.

However, it wasn’t all bad news on the implementation front. Nature4Climate’s new joint commitment tracker found that 55% of the commitments tracked are demonstrating substantial signs of progress. There are also some bright spots to celebrate. For example, tropical Asia is on the path toward reversing forest loss by 2030: Indonesia’s deforestation rate dropped by 25% last year, and Malaysia also reported a fall of 24% in the pace of forest loss last year.

Forest pledges made in Glasgow at COP26 were also in the spotlight. In 2021, $2.67 billion was put towards forest-related programmes in developing countries – 22% of the $12 billion pledged at COP26, meaning that donors are on track to deliver by 2025. Private sector funds are also moving: for example, one year after launch, the IFACC initiative is scaling innovative financial mechanisms to help farmers without further conversion of the Amazon, Cerrado and Chaco ecosystems.

So far, commitments have risen from $3 billion to $4.2 billion and disbursements are expected to exceed $100 million this year. Similarly, the public-private LEAF Coalition has mobilised an additional $500 million in private finance, bringing a total of $1.5 billion in support of tropical forest protection. This is part of $3.6 billion of new private finance announced at the climate summit.

And exciting private sector initiatives worth noting include the launch of a new company Biomas (by Suzano, Santander, Itau, Marfrig, Rabobank and Vale) to restore 4 million hectares in the Amazon, the Mata Atlantica rainforest and the Cerrado. Also, 1t.org announced pledges from its first four Indian companies (Vedanta, ReNew Power, CSC Group and Mahindra) to join 75 other companies worldwide committed to planting and growing 7 billion trees in more than 60 countries.

5. Nature of negotiations

In the negotiations, nature-based solutions were included in the COP27 text for the first time, with forests, oceans and agriculture each having their own section. The Koronivia Dialogue – the track where food and agriculture is discussed at the UNFCCC – has finally been included in the text, but all eyes turn to COP28 for the focus required to truly transform food systems.

In the wonderful world of Article 6, things remain complex. Last year, at COP26 in Glasgow, countries decided on the basic framework of Article 6. Throughout 2022, countries have been focused on how to operationalise the Article 6 mechanism that allows countries to actually begin trading. In Egypt, the discussions were very technical – such as how registries are going to work, how countries will report on the trading, and what information should be submitted –with the aim of making things easy to track.

For nature, it was decided at COP26 that land use emissions were part of Article 6 – as it includes all sources and sinks. The focus in Egypt has been on article 6.4 – the mechanism for developing guidance on activities involving removals which includes reforestation, restoration, afforestation etc.

6. Technology meets nature

In a similar way to finance, “tech” gets everywhere at climate COPs, although historically that is not really the case when it comes to nature – not this year however. In Egypt, the need for high-tech solutions for nature and climate challenges was a constant refrain. The role of tech in improving transparency and accountability in monitoring supply chains (and tackling deforestation) and also in enhancing the integrity of carbon markets was evident everywhere.

Notable developments include Verra’s partnership with Pachama to pilot a digital measuring, reporting and verification platform for forest carbon. A new Forest Data Partnership was announced by WRI, FAO, USAID, Google, NASA, Unilever and the US State Department. WRI’s Land and Carbon Lab was on show demonstrating the new frontier of measuring carbon stocks and flows associated with land use.

Nature4Climate demonstrated a beta version of its new online platform (naturebase) to help decision makers implement natural climate solutions. And the new Global Renewable Energy Watch – a partnership between The Nature Conservancy, Microsoft and Planet – was also demonstrated. Capturing this emerging trend, Nature4Climate and Capital for Climate launched a report on the size and potential of the whole “nature tech” market that was discussed at an event in the Nature Zone.

7. Food finally arrives on the scene

Food was on everyone’s mind at COP27 in Egypt – but for the first time, it also made it onto the main agenda – being recognised in the final text and also with at least five event spaces solely dedicated to food and agriculture.

Important developments included the Food and Agriculture for Sustainable Transformation Initiative (FAST) launched by the Egyptian COP presidency – a multi stakeholder partnership to accelerate access to finance, build capacity and encourage policy development to ensure food security in countries most vulnerable to climate change.

Also related to food, 14 of the world’s largest agricultural trading and processing companies shared their roadmap to 1.5℃ – to mixed reactions – with detailed plans on outlining how they will remove deforestation from their agricultural commodity supply chains by 2025.

8. An increasingly blue COP

Observers have expressed encouragement at this being “an increasingly blue COP”, with the ocean called out in the final declaration and the first ever ocean pavilion in the blue zone. Several declarations reinforced the recognition of the fundamental role of the ocean in the climate system.

The critical role that Indigenous peoples and local communities (IPLCs) play as guardians of the forest is now firmly established and beyond question. At COP27, there was a polite but palpable frustration from IPLCs that climate funds are not reaching them. This massive deficit is increasingly being acknowledged by both by Indigenous and non-Indigenous actors, with a wide range of events dedicated to this topic.

While COP27 was a good space for Indigenous and non-Indigenous actors to share knowledge, to listen deeply to one another, to build relationships, it clearly can’t be the only space. While there are a number of encouraging signs of progress, including linking IPLCs with high-integrity markets, it’s clear the clock is ticking and IPLCs are getting impatient.

Clearly we must act with urgency, but it’s critical to take the time to build trust and mutual understanding, including absolute adherence to free, prior and informed consent protocols. This is necessary so that IPLCs can decide (or not) to participate in carbon markets with transparency, full understanding, and free consent. This takes time.

10. African-led initiatives take centre stage

While this was not the “African COP” that many hoped it might be, there were still a range of significant announcements coming out of Egypt that highlighted the continent’s potential as a natural capital powerhouse. These included the launch of the Africa Carbon Markets initiative, the Declaration for the Africa Sustainable Commodities Initiative, the launch of a $2 billion African restoration fund, a funding boost for Africa’s visionary Great Green Wall initiatives, and the announcement by the Global EverGreening Alliance and Climate Impact Partners of a new partnership to up to $330 million in community-led removal programs across Africa and Asia.