The Octavia Carbon Story

To keep global temperatures from rising more than 1.5°C as outlined in the Paris Agreement and prevent the worst impacts of climate change, the world will need to reach net-zero carbon emissions by around mid-century through removal and storage of as much carbon dioxide from the atmosphere as is put. While strategies to reduce emissions — such as increasing renewable energy, improving energy efficiency, and avoiding deforestation — are critically important, they will not be enough on their own. Reaching climate goals requires strategies that actively remove CO2 from the atmosphere.

Direct Air Carbon Capture is a promising carbon sequestration methodology but has yet to scale due to high costs. Kenya-based startup Octavia Carbon, which FSD Africa has invested in, though Cohort 11 of the Catalyst Fund is the only company utilizing DAC technology in the Global South and is uniquely positioned to disrupt the cost structure of current DAC projects.

The Octavia Carbon Innovation

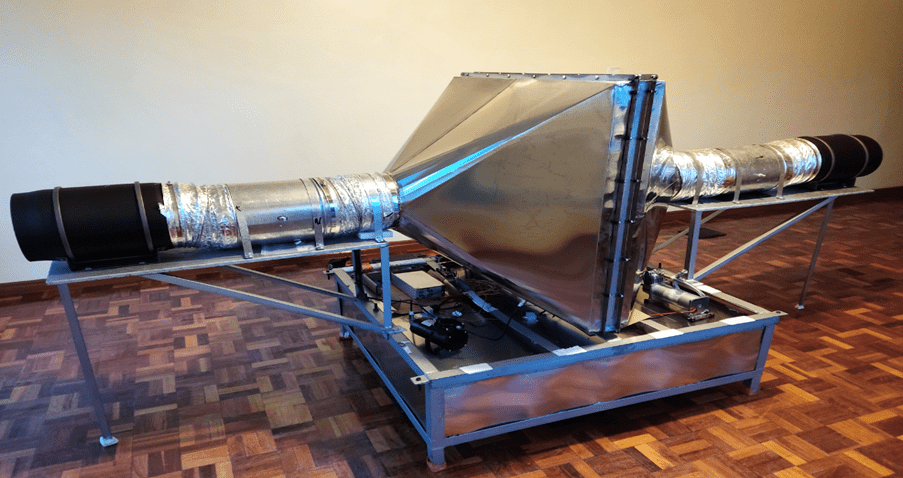

Octavia Carbon is one of about twenty companies around the globe that are building DAC technologies. The company has developed a prototype DACC machine and are currently working on a separate Minimum Viable Product (MVP) with a paying customer which will allow for iteration. The machine design will be replicated, with initial machines capturing 5-10 tonnes of CO2 per year and later machines capturing 100 tonnes of CO2 per year. By end of 2024, Octavia Carbon aims to produce at least one of these machines a day, adding some ~40,000 tonnes of CO2 per year in DACC capacity to the global market.

Project Location

Kenya, where Octavia Carbon is based, is uniquely well-suited for DACC thanks to natural endowments such as excellent geology for CO2 storage, geothermal activity, and unique renewables capacity and potential. The Kenyan Rift Valley is home to high-porosity basaltic rock that readily bonds with CO2-enriched water (carbonic acid – H2CO3), the fastest and safest form of permanent CO2 storage. Geothermal energy is also important for Octavia because ~80-90% of the energy required in DACC is low-grade (~80°C) heat energy. In Kenya, that kind of heat comes readily from the ground and is already a ‘waste’ product of geothermal power production.

For the electrical energy that DACC machines do require, it is ideal to have 24/7 green electricity, ideally coming right down the grid, and without too many competing uses for decarbonization (e.g., displacing fossil power plants). Kenya is uniquely well-suited for hydropower and geothermal energy, which today make up >90% of Kenya’s grid, and virtually 100% in Central Kenya. Few places in the world have any significant area covered by a 100% renewable grid. Kenya is also well endowed with solar (great irradiation and no seasonality), which could in the future complement the renewable energy mix even more.

Project Impact

Octavia Carbon will removes CO2 from the atmosphere and either stores it in rocks or makes it available to industries like floriculture which require carbon. This will catalyse the emergence of a new circular carbon economy that will use cheap air-captured CO2 to create further products like synthetic fuels/plastics. These direct activities will create innovative and sustainable economic growth, which will dramatically improve millions of livelihoods. Furthermore, there are additional applications for captured CO2, like enriching greenhouses with CO2, increasing plant photosynthesis and thereby leading to a higher yield, and making nutritious horticultural products more affordable and accessible to the populations that need them most. Indirectly, DACC can also eventually change the economics of geothermal energy by using abundant waste heat, co-utilizing injection wells, and providing a reliable offtake for excess energy.

Growth potential

The business model involves extracting carbon from the air using DACC technology to either store carbon in deep rock formations or produce and then sell CO2 for industrial use. The growth trajectory depicted in the financial models is promising. By the end of 2024, wirh an annual CO2 production rate of 40,000 tonnes per annum, key customers will include industrial CO2 buyers and carbon credit off-takers. Based on Octavia Carbon’s calculations, the price per tonne of CO2 will range between $300 and $500 depending on customer profile and market fundamentals.

The range of prices for capturing a tonne of CO2 varies between $775 to 1200 today depending on the technology choice, low-carbon energy source, and the scale of their deployment. Hence, Octavia Carbon’s projected price for a tonne of CO2, which requires additional extraction from the sorbent, would make it a global cost leader by mid-decade.

It also has significant growth potential due to the market and natural conditions in Kenya. The cost of production in Kenya is much lower compared to the Global North where graduate engineers cost ten times more than in Kenya. Furthermore, the world’s largest DACC company has also located their largest installations in countries with high geothermal activity such as Iceland. In Kenya, it is estimated that there are about 7,000 to 10,000 megawatts (thermal) of untapped geothermal energy beneath the Rift Valley region. Both the supply of renewable energy and talented engineers at a fraction of the cost provides a significant competitive advantage in Octavia Carbon’s scaling plan.

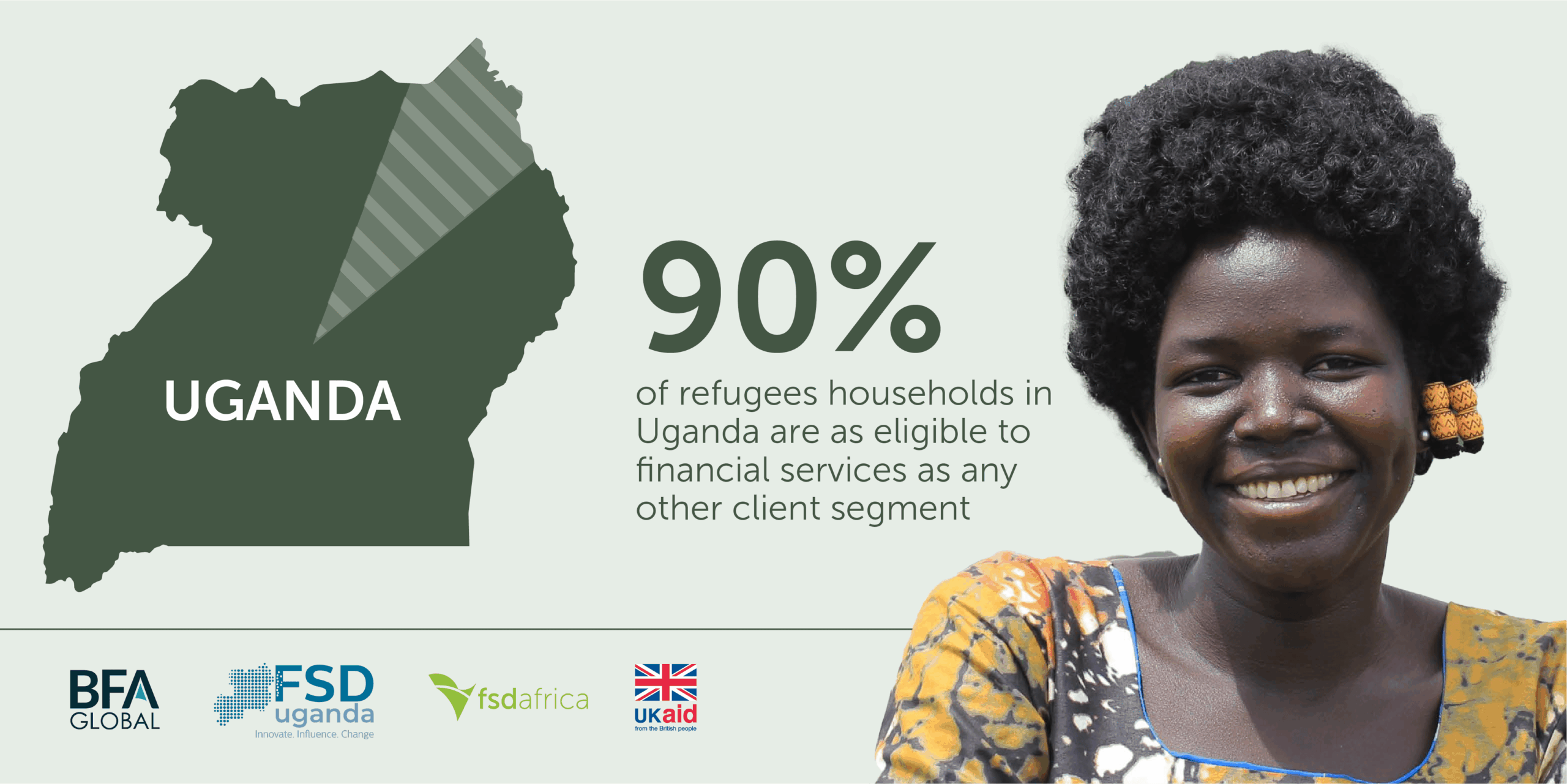

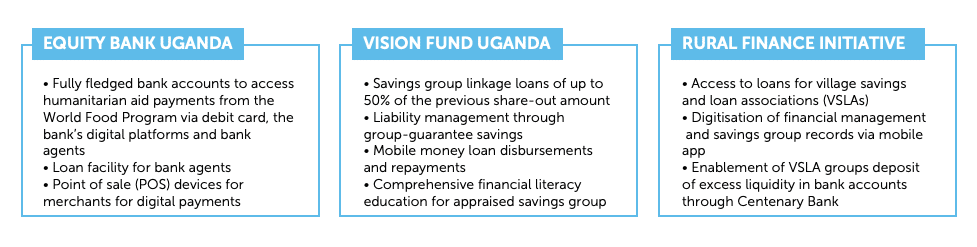

Amani fled conflict and persecution in his home country in South Sudan, and found solace in Uganda’s Bidi Bidi refugee settlement. Amani’s life took a transformative turn courtesy of the

Amani fled conflict and persecution in his home country in South Sudan, and found solace in Uganda’s Bidi Bidi refugee settlement. Amani’s life took a transformative turn courtesy of the  Amani opened a savings account with Equity Bank, which enabled him to save money and start planning for a better future securely. With access to credit and affordable loans, Amani seized the opportunity to start a small business, selling handmade crafts within the settlement.

Amani opened a savings account with Equity Bank, which enabled him to save money and start planning for a better future securely. With access to credit and affordable loans, Amani seized the opportunity to start a small business, selling handmade crafts within the settlement. Through Amani’s dedication and hard work, his business flourished. Amani not only improved his own living conditions but also extended support to other refugees in the settlement with the income generated. Amani became an inspiration, encouraging fellow refugees to explore entrepreneurship as a means to financial independence.

Through Amani’s dedication and hard work, his business flourished. Amani not only improved his own living conditions but also extended support to other refugees in the settlement with the income generated. Amani became an inspiration, encouraging fellow refugees to explore entrepreneurship as a means to financial independence. Recognising the importance of financial literacy, Amani actively participated in financial education programs organised by project partners. Amani learned valuable skills such as budgeting, saving, and managing cash flow. Motivated by his own success, Amani began mentoring other refugees, sharing knowledge and empowering them to take control of their financial lives.

Recognising the importance of financial literacy, Amani actively participated in financial education programs organised by project partners. Amani learned valuable skills such as budgeting, saving, and managing cash flow. Motivated by his own success, Amani began mentoring other refugees, sharing knowledge and empowering them to take control of their financial lives. Amani’s journey was not without obstacles. Like many other refugees, he faced uncertainties, limited resources, and occasional setbacks especially during the COVID-19 pandemic. However, through perseverance and the support of the refugee community, Amani remained steadfast in his pursuit of a better future. Amani’s resilience and determination served as a beacon of hope for others facing similar challenges.

Amani’s journey was not without obstacles. Like many other refugees, he faced uncertainties, limited resources, and occasional setbacks especially during the COVID-19 pandemic. However, through perseverance and the support of the refugee community, Amani remained steadfast in his pursuit of a better future. Amani’s resilience and determination served as a beacon of hope for others facing similar challenges. Amani dreams of expanding his business beyond the settlement’s boundaries, creating opportunities for fellow refugees and contributing to the local economy. Amani’s journey exemplifies the transformative power of financial inclusion and the impact it can have on the lives of refugees.

Amani dreams of expanding his business beyond the settlement’s boundaries, creating opportunities for fellow refugees and contributing to the local economy. Amani’s journey exemplifies the transformative power of financial inclusion and the impact it can have on the lives of refugees. Through access to financial services, coupled with resilience and community support, Amani has not only thrived but has become a source of inspiration for others. Amani’s story highlights the importance of creating an inclusive world where refugees are given a chance to rebuild their lives, contribute to their communities, and dreams of a brighter future.

Through access to financial services, coupled with resilience and community support, Amani has not only thrived but has become a source of inspiration for others. Amani’s story highlights the importance of creating an inclusive world where refugees are given a chance to rebuild their lives, contribute to their communities, and dreams of a brighter future. Amani fled conflict and persecution in his home country in South Sudan, and found solace in Uganda’s Bidi Bidi refugee settlement. Amani’s life took a transformative turn courtesy of the

Amani fled conflict and persecution in his home country in South Sudan, and found solace in Uganda’s Bidi Bidi refugee settlement. Amani’s life took a transformative turn courtesy of the  Amani opened a savings account with Equity Bank, which enabled him to save money and start planning for a better future securely. With access to credit and affordable loans, Amani seized the opportunity to start a small business, selling handmade crafts within the settlement.

Amani opened a savings account with Equity Bank, which enabled him to save money and start planning for a better future securely. With access to credit and affordable loans, Amani seized the opportunity to start a small business, selling handmade crafts within the settlement. Through Amani’s dedication and hard work, his business flourished. Amani not only improved his own living conditions but also extended support to other refugees in the settlement with the income generated. Amani became an inspiration, encouraging fellow refugees to explore entrepreneurship as a means to financial independence.

Through Amani’s dedication and hard work, his business flourished. Amani not only improved his own living conditions but also extended support to other refugees in the settlement with the income generated. Amani became an inspiration, encouraging fellow refugees to explore entrepreneurship as a means to financial independence. Recognising the importance of financial literacy, Amani actively participated in financial education programs organised by project partners. Amani learned valuable skills such as budgeting, saving, and managing cash flow. Motivated by his own success, Amani began mentoring other refugees, sharing knowledge and empowering them to take control of their financial lives.

Recognising the importance of financial literacy, Amani actively participated in financial education programs organised by project partners. Amani learned valuable skills such as budgeting, saving, and managing cash flow. Motivated by his own success, Amani began mentoring other refugees, sharing knowledge and empowering them to take control of their financial lives. Amani’s journey was not without obstacles. Like many other refugees, he faced uncertainties, limited resources, and occasional setbacks especially during the COVID-19 pandemic. However, through perseverance and the support of the refugee community, Amani remained steadfast in his pursuit of a better future. Amani’s resilience and determination served as a beacon of hope for others facing similar challenges.

Amani’s journey was not without obstacles. Like many other refugees, he faced uncertainties, limited resources, and occasional setbacks especially during the COVID-19 pandemic. However, through perseverance and the support of the refugee community, Amani remained steadfast in his pursuit of a better future. Amani’s resilience and determination served as a beacon of hope for others facing similar challenges. Amani dreams of expanding his business beyond the settlement’s boundaries, creating opportunities for fellow refugees and contributing to the local economy. Amani’s journey exemplifies the transformative power of financial inclusion and the impact it can have on the lives of refugees.

Amani dreams of expanding his business beyond the settlement’s boundaries, creating opportunities for fellow refugees and contributing to the local economy. Amani’s journey exemplifies the transformative power of financial inclusion and the impact it can have on the lives of refugees. Through access to financial services, coupled with resilience and community support, Amani has not only thrived but has become a source of inspiration for others. Amani’s story highlights the importance of creating an inclusive world where refugees are given a chance to rebuild their lives, contribute to their communities, and dreams of a brighter future.

Through access to financial services, coupled with resilience and community support, Amani has not only thrived but has become a source of inspiration for others. Amani’s story highlights the importance of creating an inclusive world where refugees are given a chance to rebuild their lives, contribute to their communities, and dreams of a brighter future.