“Our economies are built on the back of women’s unpaid labour at home”

– Melinda Gates

Empowering women means, at its core, providing women with strength and confidence to control their lives, and knowledge of their own rights so that they can actively engage in their communities.

Increasing women’s access to financial services allows them to have better control over financial resources and improves independence and mobility. It also fosters greater investments in income-generating activities, and the ability to make decisions that serve the needs of women and their families. In short – financial inclusion empowers women.

But how do women, especially those living in rural areas, access financial services?

Savings groups (SGs) and access to finance

SGs are easily accessible groups of people who get together regularly to save money and borrow from the group savings, if needed, according to rules established by the group.

Programmes that promote SGs typically focus on women’s economic empowerment and measure change through quantitative indicators of economic well-being. This is mainly because SGs enable the accumulation of funds which can be used as capital for micro-enterprises and for such programmes, the quantification of results is easier. This approach, however, provides a limited understanding of the role of SGs in affecting various dimensions of women’s empowerment, such as social, political and reproductive empowerment.

The SEEP network, in partnership with FSD Africa and Nathan Associates, commissioned a savings group research across sub Saharan Africa. The aim of the research was to highlight good practices in the design and monitoring of Savings Group programmes for women’s empowerment outcomes. The research also led to the development of a monitoring tool for the measurement of the various dimensions of women’s empowerment within SGs.

Savings groups and women’s empowerment

The research built upon pre-existing frameworks and for the first time captured women’s empowerment in the specific context of SGs.

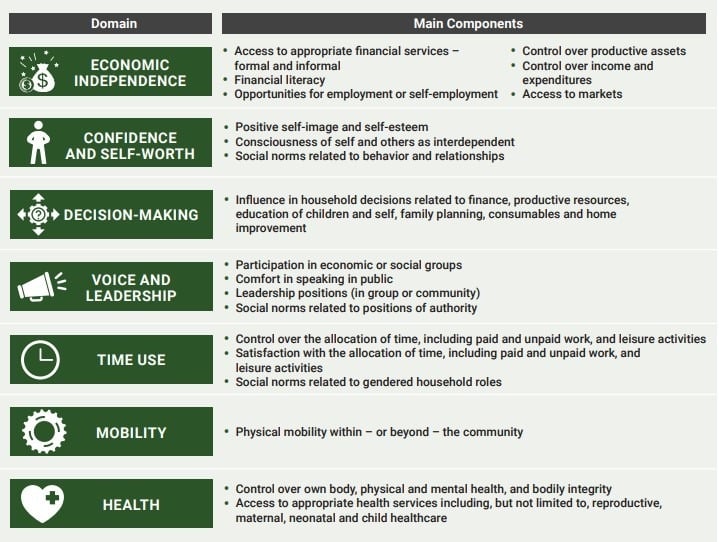

In particular, seven ‘domains’ or clusters of core areas within which empowerment can be measured have been identified. These are i) Economic independence; ii) Confidence and self-worth; iii) Decision-making; iv) Voice and leadership; v) Time use; vi) Mobility; vii) Health.

Through these domains, SGs market actors can design SGs interventions with sight of the empowerment impacts they aim to achieve. They can also observe the likelihood of empowerment outcomes and impacts across different SGs intervention types:

i) Savings Groups only interventions, for example, a development institution working on financial inclusion could adopt an SGs only approach to enable target groups to access appropriate financial services from formal financial institutions. For these kinds of interventions, empowerment impacts are strongly observed in 2 out of the 7 domains, economic independence and confidence and self-worth. Through this type of intervention, it was observed that participants gained access to appropriate financial services, enhanced financial management skills, expanded social and support networks. Fewer impacts on mobility, time-use and health were observed.

ii) Savings Groups in combination with other economic development activities, for example, a Savings Group initiative could be combined with financial education, technical or vocational training, or specific income generating activities. Strong empowerment impacts are observed for such interventions for 3 out of the 7 domains, that is, economic independence, confidence and self-worth and decision-making. Improved decision-making is observed through participants engaging in employment or self-employment and demonstrating abilities in influencing relevant decisions in their homes and communities.

iii) Savings Groups within other integrated programming i.e. programming that is aimed at weeding out harmful social norms & inequalities: for example, a Savings Group initiative could be integrated with gender programming that challenges harmful social norms such as domestic violence, female genital mutilation, negative attitudes to family planning/reproductive health, etc. The programming approach could combine SGs with education and capacity building for members accompanied by gender dialogue sessions, engaging members and their spouses, community and religious leaders.

For such interventions, impacts are strongly observed within 5 of the 7 domains: economic independence, confidence and self-worth, decision-making, voice and leadership and health. Empowerment demonstrated by leadership is observed through changes in gender norms, especially within women’s economic participation; empowerment in health through increased and improved investments in maternal, neonatal and child health or improved attitudes and norms with respect to reproductive and sexual rights. For empowerment demonstrated by time use, impacts are observed through more equitable allocation of unpaid household labour.

An example of an impactful SGs within an integrated programming intervention (i.e. intervention option iii), is the ‘Towards Economic and Sexual Reproductive Health Outcomes for Adolescent’ girls (TESFA) project under CARE International in Ethiopia. Girls within SGs provided with sexual and reproductive health (SRH) training demonstrated both economic and health related gains from programme participation. These were observed through, increased SRH knowledge, improved communication on SRH, decreased levels of gender-based violence, improved mental health, increased social support and gender attitudes.

A systematic approach to analyzing women’s empowerment

Saving Groups create economic independence for women but in order to analyze their contribution to other domains of empowerment, there is need for a systematic design of a monitoring and results measurement approach. Through this research, a toolkit that provides guidelines as to how to create an evidence-based theory of change was developed. Drawing from existing frameworks economic empowerment and existing data, the toolkit proposes a more holistic framework for SGs, based on the seven domains of empowerment discussed above. It also provides some standardized indicators to improve the comparability and aggregation of results across projects and organizations.

For more information and application of the WEE toolkit click here.

Category: Blog

Opinion article originally published on Business Day Nigeria.

Over the past decade, financial institutions have altered their view of unbanked rural populations from an impossible challenge to a fragment of society with real untapped potential.

But how do you deliver banking services to hard-to-reach communities? People who live where there is little infrastructure yet still need to buy goods, pay school fees and save for emergencies?

Recent technological developments have shown that banks can offer financial services without growing their branch network or installing more ATMs.

Financial institutions are now working with agents – local entrepreneurs who have established a business – for example a retail outlet, to provide basic banking services in the customer’s own neighbourhood.

This dynamic is known as agency banking. It enables banks to increase their reach with greater cost efficiency and it isn’t just the banks that benefit: jobs are created, local businesses grow and money flows through communities.

EquiCongo uses agency banking to reach customers in far-flung corners of the country who would otherwise be excluded from the banking ecosystem.

Reaching women

In Nigeria, Diamond Bank – recently acquired by Access Bank – developed an agent network with a focus on serving women. With 70% of women unable to access bank accounts or other basic financial services, Diamond Bank designed innovative savings schemes and rural credit that delivered financial services to women in their own communities.

The results have been impressive with 600,000 new accounts opened. This goes to show that women value the convenience and reassurance of agents who they trust, as they know them personally. This secret lies both in the power of personal relationships and word-of-mouth.

The power of digital

Digital technologies, such as the mobile phone, are central to successful agency banking models. According to the GSMA, a global organisation representing the interests of mobile operators, there has been an increase in both the number of active agents and the values they transact. In 2012, agents processed US$4.2bn in transactions. By 2017 this figure had jumped to US$17.2bn. Over the same period, the number of agents also increased significantly from 538,000 to nearly 2.9 million globally.

However, technology alone is not a quick fix. Across our work at FSD Africa – a UK-Aid funded organisation working to transform Africa’s financial markets – we see time and again that human relationships are key to unlocking financial services for unbanked populations. From a customer’s perspective, financial services become tangible and legitimate when delivered through trusted and well-known agents in their respective communities.

Roving agents

Recognising the importance of human relationships, banks are also turning to roving agents. These agents, with their door-to-door customer service, have reinforced the relationship between the bank and its customers, resul more customer-centric design and provision of financial services.

Nigeria’s Diamond Bank has roving agents dubbed ‘Beta Friends’, who directly market and sell savings and loan products to unbanked market traders, growing the bank’s customer base. Beta Friends visit market traders at their places of trade and help them open bank accounts and make transactions. They also assess loan applications, make recommendations to the bank’s credit officers and collect repayments.

Roving agents allow customers to save time and costs associated with having to visit a branch or an ATM. Women, caregivers and others unable to travel to bank branches also benefit from this model.

More than banking

FSD Africa has supported banks in Nigeria, Ghana and the Democratic Republic of Congo to establish successful agency banking models, bringing services to over two million unserved and underserved customers.

To scale up the model, international development organisations should pitch in to providand technical support. Equally, financial and insurance institutions should invest in agency research and training.

Over the coming years, agency banking will play an important role in financial inclusion, which is critical to the long-term reduction of poverty and economic growth in Africa. It’s now down to the commitment of all stakeholders to enable access to the financial products necessary to support and grow this band of game-changing innovators

Many claim that Central Bank Digital Currency (CBDC), formally known as Digital Fiat Currency, can have many benefits for financial inclusion and has the potential to impact mobile money. But can CBDC overcome the challenges that current mobile money providers and consumers face?

First things first; what is “Central Bank Digital Currency”. Simply put, CBDC is a digital representation of physical cash. As its digital alternative, CBDC is interchangeable with physical cash on a one-to-one basis as valid legal tender, and adopts all three of cash’s key features: a unit of account; a store of value; and a universally accepted means of exchange between transacting parties. The distinction between CBDC and private cryptocurrencies are summarised below.

Figure 1. Digital Fiat Currency compared to Private Cryptocurrencies

Source: Cenfri, 2018

So, what’s the relevance of CBDC to financial inclusion?

CBDC has the potential to digitise the entire payments value chain, from the first to the last mile in a more cost-effective and efficient way. Cenfri’s 2018 report “The benefits and potential risks of digital fiat currencies” finds that CBDC, unlike cryptocurrencies, can promote adoption through network effects because of the key features that is shares with cash. CBDC’s speed, efficiency and safety (being backed by the Central Bank) introduces much needed trust in digital payment mechanism, something that is lacking in private cryptocurrencies and mobile money. And trust is critical where money is involved. Trust means that CBDC could eventually be adopted along the entire value chain (like cash) and hence could promote financial inclusion at all levels of society.

But what about mobile money specifically?

Mobile money may be a leader in “banking the unbanked” but the phenomenon still faces obstacles that undermine its uptake and use, as shown in the figure below.

Figure 2. Key supply and demand cost drivers of mobile money in SSA

Source: Cenfri 2019, based on data from various literature sources

The application of retail CBDC to mobile money can foster greaterinteroperability, improve payment efficiency, facilitate cost-saving gains and reduce key payment risks typically associated with mobile money. CBDC can also enable trust in mobile financial services due to its safety and the way in which its speed eases liquidity constraints of mobile-money agents. CBDC also eliminates the need for unnecessary third-party intermediaries and so streamlines payment clearance at the same time as enabling true interoperability.

How about the downsides of CBDC?

If CBDC is not implemented appropriately it could exacerbate contextual inequalities along the lines of digital, financial and economic disparities between population segments and also intensify the complexity of mobile money. For example, if not everyone has a mobile phone then only those that do can access CBDC; and if only certain areas have network coverage then only those in those areas can access CBDC; and so on. CBDC could threaten the intermediation role of traditional deposit-taking. CBDC could also exacerbate poor uptake of mobile money (e.g. due to illiteracy) simply because of CBDC’s (perceived) complexity. If everywhere you can only pay in CBDC then it may make the gap between illiterate and literate users even wider. The more vulnerable segments of the population, as primary unstructured supplementary service data (USSD) customers, could also be at greatest risk of identity fraud.

So what can be done to avoid these risks?

CBDC can bring maximum benefits to mobile money and financial inclusion if it meets certain pre-conditions. The basic principles to avoid these risks lie with governments and the enabling financial environment they create in their respective countries. Governments need to ensure appropriate and effective legislation and anti-money laundering and combatting the financing of terrorism regulation, as well as the implementation of robust consumer protection laws and national cyber-security defences. We know that that some developing economies lack these key laws – or lack the ability to uphold the legislation, even if it does exist. Through our Risk, Remittances and Integrity Programme, FSD Africa is partnering with Cenfri to combat these challenges by helping countries implement appropriate regulation that enables low-cost, efficient, domestic and cross-border payments to enable inclusive financial systems to operate at scale, and positively impact broader economic development.

It’s clear mobile money presents a significant use case for CBDC in the drive towards financial inclusion, but not without risks. If governments, supported by development partners, address these concerns, the impact of CBDC on mobile money could not only be positive, but could also contribute to significantly greater financial inclusion and better economic integration altogether.

You can delve deeper into the role of CBDC in delivering financial services to the unbanked and CBDC’s applicability to mobile money by downloading Cenfri’s latest report “Central Bank Digital Currency and its use cases for financial inclusion; a case for mobile money”.

Opinion article originally published on Devex.

One of climate change’s great injustices is that the worst affected countries are the ones that have contributed least to the problem.

In 2015, the world coalesced behind the Paris Agreement on climate change in an effort to transition to a low carbon future. And while much attention has been on the United States’ decision to withdraw from the agreement, many African governments have been stepping up.

Following the African Union’s lead, Ghana, Ethiopia, and Kenya, among others, have all factored climate change into their national development plans. And it is easy to see why these African nations are approaching climate change with earnest given the danger climate change presents to the continent. Cyclone Idai, for example, left incalculable destruction across three countries last month, an unfortunate reminder of the devastation climate change could have on the continent.

Trillions of dollars of investment are needed to combat climate change. And while the Paris Agreement does have funding mechanisms to support developing countries, these funds can only go so far.

Moreover, unlike the world’s primary greenhouse gas emitters, developing countries in sub-Saharan Africa need to encourage growth without fueling emissions.

Take electricity: Sustainable Development Goal 7 states that everyone should have access to affordable and reliable electricity by 2030. Yet, in a region where more than half the population still does not have access, governments need to improve access and reliability without turning to high-emitting power sources such as coal.

The role of green bonds

A solution to the crisis may lie in green bonds, which allow issuers to raise money specifically for environmentally friendly projects, such as renewable energy or clean transport.

This year, analysts predict the green bonds market will grow to $200 billion, a 20% increase from last year and a significant jump from 2016, which saw $87 billion raised. But while the global market continues to grow, there are fewer bonds available across Africa.

Most of Africa’s green bonds have been issued by the African Development Bank, which has raised over $1.5 billion since 2013. While Nigeria issued a $29.7 million bond to fund solar energy and forestry projects in December 2017, no other countries have followed suit.

African governments have historically relied on development finance institutions to fund green projects such as irrigation initiatives and solar energy. However, this is unsustainable and ignores potential capital that could be raised from pension funds, the diaspora, and the middle class. For example, Kenya’s pension sector is valued at about 1.2 trillion Kenyan shilling, or $11.9 billion.

If national governments want to unlock more capital, structures are needed to give investors the confidence to invest.

Kenya, Nigeria, and South Africa are leading the charge in sub-Saharan Africa. Since 2017, these countries have been working with a range of partners, including FSD Africa, to develop a robust framework for the issuance and listing of green bonds. Now, Nigeria and Kenya have joined India, China, and Indonesia in turning their frameworks into official guidelines — and the market is responding.

Last month, the Nigerian-based Access Bank issued Africa’s first certified corporate green bond, unlocking $41 million to protect Eko Atlantic City, near Lagos, from rising sea levels. This bond will also support a solar energy project. Notably, the bond was fully subscribed, highlighting the fact that if the frameworks are built, investors will come.

While development finance will always play a critical role in supporting development on the continent, countries are recognizing they need to unlock funding from other areas. Kenya and Nigeria have heard this call and global markets have responded. This should give other countries confidence to follow suit.

Given the nascent nature of capital markets in Africa, we have the unique opportunity to build them from the ground up and respond to pressing priorities including climate finance. This is particularly critical as governments start to pursue infrastructure development at a larger scale.

Green bonds may still be a small piece of the global bond market, but they are showing real potential for helping developing countries move to greener, more equal economies.

Like most bankers, Patrick Kiiru did not imagine Congolese refugees as his ideal clients, seen by most as simply hungry, homeless, and transient. But after three days with FSD Africa in Gihembe Refugee Settlement—a bumpy one-hour journey north of Rwanda’s capital Kigali—the head of diaspora banking at Kenya’s Equity Bank Group began to change his mind.

After having experienced the refugee-finance business case firsthand, Kiiru describes reaching an “aha” moment: “I can solve this problem. It is possible to serve… refugees profitably.” Refugees need more than food and shelter; they, too, can benefit from financial services.

With targeted financial and technical support from two United Kingdom aid-supported agencies—FSD Africa and Access to Finance Rwanda—Kiiru’s bank is preparing to offer its Eazzy Banking mobile money product to Rwanda’s adult refugee population of more than 89,000, with plans to expand in other countries. With a footprint in Kenya, Uganda, Rwanda, and the DemocratDRC), this may be the early days of a region-wide approach by Kiiru and his team.

This risk perception versus reality gap is not distinct to banking refugees. The theme persists across all 26 fragile and conflict-affected states in sub-Saharan Africa, as defined by U.K. aid. There are two big picture consequences.

First, development agencies and their partners with a focus on private sector development can neglect to deliver services where they are needed most. According to a 2016 CGAP survey of 19 financial inclusion donors in sub-Saharan Africa, the highly fragile states of Chad, Central African Republic, and Somalia had only one active donor each. This means some countries, regions, and communities remain trapped within a humanitarian crisis paradigm.

As the world grows more prosperous, international development practices will only increase in concentration in the left-behind nations, regions, and communities.

Second, development financiers, commercial investors, and business leaders can misprice risk—adding a premium based on perception rather than the reality. This means capital is not being efficiently allocated. According to World Bank figures in 2017, excluding Ethiopia, Kenya, and Nigeria, just 3.23 percent of all foreign direct investment in sub-Saharan Africa reached fragile states.

This mean that, in fragile states, many investment-ready firms are left without the long-term finance they need to survive and grow. This is not to say fragile states are not difficult places to invest and do business. Since 2016, FSD Africa’s own increasing fragile states footprint in the DRC, Sierra Leone, Zimbabwe, and for forcibly displaced people has had to weather a cycle of instability: political (e.g., military coups, new central bank governors), environmental (e.g., Ebola outbreaks, mudslides), and economic (e.g., currency depreciation, inflation).

But the people, entrepreneurs, and investors in Africa’s fragile states are resilient and resourceful. The FSD Africa team has witnessed numerous examples of smart practices which help to mitigate risk.

On the investor side, locally born nationals, who are better able to price risk accurately, are particularly active; many accept that there will be arid periods when deployapital is too risky, and so switch to running their own enterprises; and many deals rely on financial innovation to hedge against risks.

On the donor side, some build a presence—people and platforms—which lays dormant when things are difficult, but which springs into action when pockets of opportunity present themselves. Others complement their fly-in, fly-out model with a permanent local lead, who provides a depth of relationships and market intelligence to build and maintain momentum in good times and b

Nearly one in four households in Africa are headed by women, reaching 41% in Zimbabwe, 36% in Kenya and 35% in Liberia according to the World Bank. Female-headed households have been increasing across all countries, globally. So, as well as considering the broader challenges and opportunities affordable housing creates for everyone, we should also ask: what’s the significance of housing specifically for women?

The consequences of good housing are far-reaching: the quality of housing impacts on its residents’ health and safety, their ability to function as productive members of society, and their sense of well-being in their community. Good housing contributes to good health outcomes, provides protection from the elements and supports a family’s needs throughout its life cycle. These factors have a particular impact on women. In many low-income households across Africa, whether in rural areas or in the cities, the home is still the woman’s domain. The quality of the living environment impacts partn her day-to-day experiences and capacities to meet the needs of all who depend upon her. It is for this reason that we know that women are especially keen on home improvements and often the drivers of such initiatives within their households.

Increasingly, and especially in high-unemployment contexts, the income-earning potential of housing is also being recognised. Many women identify entrepreneurial opportunities through their housing, using their homes as their business premises, running a shop on site, or working remotely. Some are renting out one or two rooms, or a structure in the backyard (see our video interviews with two female clients of Sofala’s i-build home loans project) contributing to household income. Recent research finds that poverty falls faster, and living standards rise faster, in female-headed households.

A home and its surroundings also affect a woman’s identity and self-respect. This social dimension, while less tangible, is nevertheless hugely significant. A home offers long- and short-term security for women as household members, especially those that are unmarried. Secure housing provides safe shelter and protection from homelessness after divorce, widowhood, job loss or other challenging circumstances. A key development worth noting has been that all government subsidised homes in South Africa are now registered in the names of both spouses. In short, a secure home enables more choices and more individual freedom. Having “a place to call my own” makes it possible for a woman to run her own household, that is, to become the head of the household, providing a degree of security to ride out and rebound from life’s uncertainties, such as temporary unemployment or illness.

Another impspect of home ownership is access to collateral, which enables women to access financial services and accelerate their earning potential. A savings account in a woman’s name offers a form of security and independence: a safe place to store and protect earnings. Women make better borrowers because they know that their ability to improve the home in the future depends on the reputation they develop in managing a particular loan. Women are therefore a very important part of the housing solution, and should be understood as such, by policy makers, project implementers, and service providers. In cases where women do not have title deeds for their home, banks are revolutionising the way they lend for home construction. For example, in Kenya – a country with a population of 50 million, but less than 30,000 mortgages – the Kenya Women Microfinance Bank (KWFT) has created a new loan product called “Nyumba Smart” (“smart home”). Using flexible collateral, the loans provide female customers with up to $10,000, repayable over three years, for the construction of all or part of a house.

Despite this progress, over 300 million women live in African countries where cultural norms prevent equal property rights, even when there are formal, equitable property laws ouragingly, innovative technology-based tools are helping to overcome this barrier. For example, the social enterprise, Map Kibera is working on an open-source mapping platform for Nairobi’s largest slum. The objective is to give inhabitants an informal claim to their land, to lobby for services and to act as “evidence” in negotiations with municipal governments, which may otherwise bulldoze settlements with no legal title without warning.

At FSD Africa, we believe housing plays a crucial role in economic development and poverty reduction, not least for women. That is why we have partnered with the “http://housingfinanceafrica.org/”>Centre for Affordable Housing Finance in Africa (CAHF) to promote investment in affordable housing and housing finance across Africa; we have also invested in Sofala Capital, which includes Zambian Home Loans Limited and iBuild Home Loans Pty Limited as part of its group of companies. By strengthening Sofala’s balance sheet, we are enabling these companies to achieve scale with their innovative housing finance product offerin

The Green Bonds Listing Rules and Guidelines for Kenya were issued last week. These make it clear to issuers of Green Bonds in Kenya what the regulators expect of them by way of disclosure. Regulatory certainty is the bedrock of well-functioning financial markets and so the launch is an important milestone in the development of this fast-growing market.

The Kenya Green Bond Programme, co-funded by FSD Africa, has already identified KSh90bn of investment opportunity in Green Bonds in the manufacturing, transport and agriculture sectors in Kenya, a small but significant contribution to a global market that is already worth almost $400bn. The Kenyan government itself is planning to issue its first Green Sovereign Bond, perhaps in the next six months.

The Patron of the Kenya Green Bond Programme, Central Bank Governor Patrick Njoroge, a passionate environmentalist, spoke eloquently at the launch about the societal value of investing through Green Bonds.

The elephant in the room was the interest rate cap in nya. While caps remain in place, the pricing for Green Bonds, as for other non-sovereign bonds, will almost certainly be prohibitively expensive compared to long-term bank finance. We run the risk that the momentum that now exists in Kenya for Green Bonds will stall because of this almost existential problem. The Governor urged us to take a long view – implying the caps will one day be lifted. We live in hope but it is a pity that priority sectors for Kenya’s economic development, such as affordable housing and manufacturing, cannot at the moment easily benefit from investor interest in this asset class.

Already Nigeria, which issued a Green Sovereign in December 2017, is pulling ahead of Kenya and the Nigerian corporate sector seems to be gripping the Green Bond opportunity more vigorously than Kenya with several issues at an advanced stage, including in the commercial banking sector. FSD Africa has an active Green Bond programme in Nigeria too.

Another problem is easy access to competitively-t from Development Finance Institutions. On the one hand, DFIs push environmental priorities through ESG frameworks. On the other, they offer credit lines to potential issuers on significantly more attractive terms than bond pricing. Does that matter – if green projects get funded anyway? Well, yes it does, if it means we keep not seeing demonstration transactions for Green Bonds. The potential supply of finance for Green Bonds from local pension funds and other institutions is so much greater than what DFIs will ever be able to make available – we should take what opportunities there are to get local institutional capital into this market and DFIs should step back.

A big part of the attraction with Green Bonds is the extra corporate disclosure that is required. Companies are required to lay out their environmental strategy for the Green Bond they want to issue and what systems they will put in place to make sure the bonds proceeds are allocated for the stated environmental purpose. This createunity for a different kind of conversation between investors and issuers, forging a connection that is values-based as well as purely economic.

In the same way, according to Suzanne Buchta of Bank of America, a big issuer of Green Bonds, Green Bonds create opportunities for new kinds of “corporate conversation” within companies – how green is this initiative, how green are we as a company? Buchta suggests that the ESG disclosures from Green Bonds lead to such positive outcomes that they could become the norm for all bonds.

Interestingly, the Economist this week is also calling for companies to be obliged to assess and disclose their climate vulnerabilities by making mandatory the https://www.fsb.org/2017/06/recommendations-of-the-task-force-on-climate-related-financial-disclosures-2/ voluntary guidelines issued in 2017 by the private sector Task Force on Climate-related Financial Disclosures set up by the Financial Stability Board.

This trend towards transparency is good for market-building. It’s good for investors, companies and for employees of those companies. And Green Bonds are playing an important catalytic role in this.

Remittances are a pivotal, though often unseen, driver of economic growth across Africa, in particular having a positive pro-poor effect on health, education and human capital development. The continent’s remittance economy has grown quietly and organically, taking up an essential role not just as a safety net, but also as a catalyst for entrepreneurship. Why is this so important? Because it changes how we should think about remittances: these flows are international development finance by another name, with the potential to be highly targeted, efficient and effective.

Remittances are an efficient, impactful and resilient form of development capital. FSD Africa has supported research by Cenfri which shows that the value of remittances in sub-Saharan Africa (SSA) is almost equal to that of “traditional” foreign capital flows such as overseas development assistance (ODA) and foreign direct investment (FDI). And their impact is potentially greater – especially in areas like health and education. In 2015, the region received USD39 billion in FDI and USD37.1 billion in ODA, compared to USD34.6 billion in remittances. However, between 2012 and 2015, formal flows of remittances grew at a higher growth rate than both FDI and ODA. If we isolate the UK as a source of capital, between 2015 and 2016 remittance flows actually overtook the value of ODA and FDI combined. Cenfri’s most recent case study, Remittances in Uganda, tells us that remittances from the UK to Uganda amounted to USD275 million annually – more than double the amount of foreign aid from the UK.

Yet the cost to send money home remains high. The average cost of remittances to SSA is over 9% of the value of the transaction, compared to a global average of 7% (we dig deeper into this in our infographic on the cost of remitting money from the UK). We want to bring these costs down. Signatories to the UN’s Sustainable Development Goals have pledged to reduce the average transaction costs of remittances to less than 3% of the amount transferred by 2030, with no remittance corridor costing more than 5%.

Our new research, Moving Money and Mindsets, shows an exciting new trend towards transferring money online. In 2016, 90% of remittances from the UK were being paid in cash at an agent. Fast forward two years, and we found that roughly half of focus group members now use online services – a significant and rapid switch in behaviour. Online remittances providers – like WorldRemit, Wave and TransferWise – not only provide transparency, security and convenience but are also significantly cheaper. It costs almost £16 to send £120 from the UK to Ethiopia in cash using an agent. The same amount costs only £6 to send online. Switching online clearly makes economic sense, so why stick to cash?

Some remittance markets are simply “stickier” than others. In countries with underdeveloped payment systems – like Zimbabwe, Sierra Leone and the DRC – cash is still king. For example, in the DRC, less than 10% of people have a bank account, and mobile money is virtually non-existent. Other barriers to switching to online services include the registration process, perceived security issues and technological barriers for older people. The solutions range from relatively easy quick fixes like simplifying the registration process and marketing online services to customers to longer-term interventions designed to develop digital payment infrastructures in Africa. Our Risk, Remittances and Integrity (RRI) Programme is working at the individual, regional and global levels to remove these barriers to switching to online, and to bring the transfer costs down. Cash may still be king in some countries in Africa, but cash is costly and with digital alternatives on the rise, its reign may be nearing its end.

Read FSD Africa’s new research, “Moving Money and Mindsets” here.

If you open the World Bank’s Global Financial Development Database and compare the data on private credit against total population, it is instructive to note the markedly different growth rates. In the developing economies of sub-Saharan Africa, credit extension has grown fairly impressively in the last 10 years albeit off a low base—from 10 percent to 18 percent. However, the total population of the region has grown by nearly a third, and now stands at 1 billion people. These disparate numbers suggest that credit is not growing fast enough to build the infrastructure and create the jobs needed to support this rapidly growing, young population.

THE IMPORTANCE OF CREDIT

For the majority who live on the continent, especially those living in cities contending with rising food and fuel prices, their ability to build or acquire assets is extremely constrained. For most people, access to credit is not about investing in buildings or businesses. It’s about managing daily challenges. In shor is a necessity, the means by which people can “stay in the game.”

For sure, easier access to credit—through, for example, credit and store cards as well as mobile-based loan product innovations like M-Shwari, Branch, and Tala—helps with consumption smoothing. But in Africa today there is not much that credit markets can offer the economically active “near poor” to help them build capital in a meaningful sense.

In developed economies, housing finance has allowed countless millions over the decades to build household wealth. Yet in Africa, mortgage markets are extremely thin. In Uganda, there are an estimated 5,000 mortgages for a population of 41 million while in Tanzania, there are only 3,500 mortgages in a country with a population of 55 million. Market dysfunction like this means that people without land or buildings do not benefit from the asset-price inflation that creates unearned wealth for those who already have capital, and so we see societies becoming dangerously divided and unequal.

Credit extension in Africa lags behind other regions of tha dramatic extent. While the ratio of credit to GDP is only 18 percent in sub-Saharan Africa, comparable figures in South Asia and Latin America are 37 percent and 47 percent, respectively. Across sub-Saharan Africa, central bankers and policymakers now realise that much bigger and better-functioning credit markets should be a priority outcome for their financial market reform strategies.

In the financial inclusion world, credit raises concerns because of the risks of over-indebtedness. Indeed, this is a worry in contexts such as in Kenya, where there has been a proliferation of different apps for online credit, and evidence is emerging that online credit is being used for unproductive activities, like online gambling. But we should not let this get in the way of the reality that Africa needs a lot more credit if economic development is keep pace with population growth.

Despite the importance of credit markets, we have not yet, collectively, made them a serious enough object of inquiry—and the consequs of not doing so are profound.

CREDIT MARKET REFORM

Credit market reform poses a challenge because credit straddles the entire financial market—from microcredit at the one end, through to capital markets, including project and bond finance, at the other. Credit also involves banks as well as non-bank financial institutions, including now fintechs and even telcos—so whose job is it to regulate credit markets? Central banks only? Or market conduct authorities with mandates that go beyond consumer credit into areas such as investor protection? Or dedicated credit regulators, such as South Africa’s National Credit Regulator? It is not always clear who should be responsible and so reform processes often lack leadership.

We also see credit market reform being promulgated in a fragmentary way. For example, strengthening credit market infrastructure tends to be the preserve of those interested in the development of small and medium enterprise finance, while consumer protection tend looked at through a responsible finance lens—when in fact the different elements interrelate. Credit market reform strategies should be much more joined up than they are.

There is currently no single African “observatory” monitoring the evolution of credit markets in Africa and no single Africa-based resource dedicated to combating credit market dysfunction. The past decade has seen numerous policy mis-steps in relation to credit markets, well-intended initiatives that have not been grounded in good evidence. Better information exchange might have prevented these mistakes. In Africa we lack effective mechanisms for knowledge sharing and peer learning around credit, a marked contrast to the plentiful knowledge sharing around related areas such as bank supervision and digital financial services.

There is also a vital need for African credit markets to take advantage of the increasing availability of concessional capital as donor organisations shift their funding towards returnable capital and awaant finance. Blended finance capital structures, with their ability to de-risk and pump prime lending, should encourage banks and other lenders to explore new markets in a sustainable way, in which risks are appropriately shared.

In addition, there is a fundamental need for much better data on credit markets. Without much more granular data by sector or by gender, it is going to be difficult for policymakers to implement effective strategies aimed at driving investment into essential industry sectors such as agriculture, housing, and infrastructure.

The Bank of Zambia, with support from FSD Africa, has been piloting an innovative scheme to improve data on credit markets. Under the scheme, all regulated financial institutions submit supplemental quarterly returns on their loan books to the central bank in return for which they get to see, in aggregate and by sector, trend data on the evolution of credit markets in Zambia. In this way, they can benchmark their own performance against the performance of tentire industry. We think this will spur competition and innovation by private credit providers. The Zambian authorities, meanwhile, now have the information with which they can make informed choices about where to take credit markets in Zambia, and how to manage risks but also, crucially, how to foster innovation and where to target support.

Note: The Africa Growth Initiative at The Brookings Institute first posted this blog on 1 August 2018. This is a reproduction from the original with AGI’s permission.

Note: This blog reflects the views of the author only and does not reflect the views of the Africa Growth Initiative.<

Setting the scene…

Blink and you might have missed it. But as dusk gave way to darkness on a sunny afternoon in Kigali, UNHCR Livelihoods, Access to Finance Rwanda (AFR) and FSD Africa received a brief but deeply significant email from Equity Bank Rwanda…

“This is to confirm that Equity Bank Rwanda will honor either proof of registration or refugee IDs as valid identification documents [to open a bank account]. We will issue a memo to all our branches to this effect before the end of the week”

18:18, Thursday 22 February, 2018

Kigali, Rwanda

Equity Bank Rwanda

This email marked another milestone for FSD Africa (UK aid’s Nairobi-based platform for inclusive financial sector work in sub-Saharan Africa) almost exactly 12 months of work in a new and important area: the financial inclusion of refugees and other forcibly displaced populations (FDPs).

The recent, rapid growth of FDPs in sub-Saharan Africa has created an urgent need to respond quickly to a complex and dynamic challenge. Through this blog, we wanted to capture what we’ve learned so far so…

Demand-signals: a new way to deliver humanitarian assistance…

Perhaps our most important realisation/conclusion is that refugee settlements are not only hubs for humanitarian assistance. They’re markets, too…

There are buyers and sellers supported by rules and institutions (both formal and informal), especially in larger, older refugee settlements such as Gihembe in Rwanda. And like most markets – these places have failures and pinch-points which inhibit the ability of FDPs to access and use, for example, financial services to help manage their lives.

And while the need for food, shelter and other safety net-type activities will remain, there is now good evidence (from our work and beyond e.g. this study by the IFC, which was featured in The Financial Times) that market-shaping and building has the potential to crowd-in the private sector to profitably deliver some of the goods and services that refugees need and can pay for themselves.

As a quick data point or two from Rwanda, primary FSD Africa and BFA research showed that 90% of refugee households earn $29+/month (the same as the median value of Rwandan bank account holders), while 43% have a secondary school education or more. Globally, 42% of all FDPs have been displaced for 5 years or more.

Identify and experience the market opportunity…

We’ve found that a lack of information is a major challenge. First, refugees are typically viewed by financial service providers as high risk (and low return) clients. Second, they are too often treated as a homogeneous, unsegmented group, dependent on humanitarian hand-outs.

This stereotyping is a tough nut to crack. It involves bridging knowledge gaps, but also long-held attitudes and behaviors. We quickly realised that market intelligence alone – on the financial lives of FDPs and business case for providing FDPs with financial access – just wasn’t enough. Financial services providers needed to see and feel the refugee market for themselves.

In November 2017, FSD Africa, AFR and UNHCR took bank decision-makers out of their offices in Kigali and into a refugee settlement for two nights to develop and test new/existing products, an approach which was replicated by colleagues at FSD Uganda in June 2018.

The transformation was remarkable, and something we started to document, in order to share with other banking decision makers in Kigali, East Africa and beyond.

“It is possible to serve the base of the pyramid, especially refugees, profitably; …I think I may have not necessarily seen the opportunity before I got here”

Patrice Kiiru, Equity Bank Kenya

The power of partnerships…

FSD Africa knew little about this space when we started out. We had theories to test, but little practical experience of accessing camps, refugee politics nor humanitarian assistance more broadly.

The only way we have been able to learn quickly is through the quality of our partners. For UNHCR Rwanda to speak with authority about the power of markets to deliver welfare enhancing outcomes to FDPs was refreshing and impressive in a space historically dominated by charitable giving and direct delivery.

“The way I see it, financial inclusion is really the key to unlocking the economic inclusion”

Jakob Oster, Livelihoods Officer, UNHCR Rwanda

We have built useful partnerships with a wide range of institutions, from commercial banks to charities, and from UN agencies to fintechs. Amongst them, UNHCR is our key humanitarian partner and, through our Innovation Competition FSD Africa and AFR are providing x5 £10,000 accelerator grants to CARE Rwanda, Equity Bank Rwanda, Tigo/Airtel Rwanda, Umutanguha and MFS Africa to develop new solutions to particular challenges faced by refugees. This commitment may be followed to larger investments (up to £150,000) to allow ideas to reach real scale. Beyond this competition, we’re continually looking for opportunities to engage interested, impactful private sector partners.

We have also built partnerships to maximise our local understanding and influence. AFR – a UK Aid, US Aid, Swedish Sida and MasterCard Foundation-funded ‘FSD’ programme for Rwanda – has been an invaluable support. Located in Kigali, with deep connections to the local banking system and regulators, the whole process has been made more effective. Within three months of beginning our work, AFR had successfully lobbied the Central Bank and MIDIMAR to add refugees to the Rwandan Financial Inclusion Strategy.

FSD Africa and AFR have also worked closely with DFID Rwanda.

“Market participation triggers wins for refugees, host communities and hosting governments. This new initiative has been a great demonstration of how to incentivise a market-driven response to a humanitarian challenge.”

Viola Dub, Private Sector Development Advisor, DFID Rwanda

This work falls within the context of a broader Government of Rwanda and DFID Rwanda approach to FDPs. In 2016, Rwanda – as an FDP host nation – signed up to the UN’s Comprehensive Refugee Response Framework, and with DFID Rwanda support is designing a plan for refugee integration.

The host community challenge/opportunity…

A crucial issue that we have struggled to grip is how to integrate host communities – ‘native’ settlements, often poor, rural and located nearby/adjacent to refugee settlements – into our programming. There are a number of stories about host community residents feeling that refugees benefit disproportionately from international aid and government agency support.

This is a difficult balance to strike. It is encouraging to see evidence that local communities benefit from hosting refugee communities, due to higher agricultural opportunities and incomes, but trickle down forces alone seem inadequate. Ensuring we work for host communities as well as FDPs means investing as much in understanding and responding to their specific needs as we do to the FDP. After all, their inclusion in our approach can only bolster the business case adding hundreds of thousands of potential clients.

“I was very surprised, because before arriving in the camps I was not expecting to find some real businesses in the camps; I was surprised to see someone with a business like other Rwandese outside of the camps.”

Theophile Nsabimana, Vision Fund Rwanda

Twelve month conclusions…

One year on, our successes (and failures) may lack the ‘flash-bang’ of a large DFI investment or a VIP launch, but we really can see the emergence of new markets.

FSD Africa and AFR are now seeding product/solution prototypes by more than five financial service providers in Rwanda. Refugees – young and old, male and female, short-term and long-term displaced – have expressed their demand for financial services to help manage their lives. The National Bank of Rwanda has incorporated refugee finance into its financial inclusion strategy, and banks now better understand that refugee IDs are eligible banking IDs (as per the introduction to this blog).

More broadly, we believe that we’re at the tipping point of genuine behaviour change within the private sector towards this group. FSD Africa and AFR received 23 applications to our refugee finance competition in December 2017, while only last week FSD Uganda and FSD Africa received more than 20 applications by MFIs, banks and fintechs just to visit camps to see the opportunity for themselves. FSD Africa is also about to start work replicating this approach in DRC, through our sister organisation ELAN RDC.

The proof is in the pudding. And we’ll be watching carefully to see: whether refugees can become long-term, profitable clients for the financial sector, but also whether finance can be genuinely useful to forcibly displaced people. But, for now at least, the market is on the move…