FSD Africa and the SEEP Network convened a stakeholder meeting in Benin in February 2017 to explore the role of savings groups in contributing to broader development goals and activities in the country.

Country: Ethiopia

Skills shortages among financial institutions (FIs) in Africa have long been recognized as an important- and perhaps the most important- constraint to their growth. In late 2012, the Consultative Group to Assist the Poor (CGAP) conducted a global on-line survey which aimed to better understand the dynamics within the market for skills development and other services; and to develop guidance for funders to support market development.

Subsequently, FSD Africa and CGAP sought to better understand the demand for and supply of capacity building services for financial inclusion in Sub Saharan Africa (SSA) by digging deeper into available data from the 2012 CGAP global research. The aim was to explore differences in responses by service provider type and clusters of countries/sub-regions.

The key highlights from the SSA analysis include: FIs acknowledge that the most significant short-term challenge they face is the lack of capacity to run their institutions professionally and regard risk management, strategic plnning and mid-level and people management skills as most needed; although FIS are aware of the availability of the services they need in the marketplace, they do not always regard these to be of high quality. Lastly, capacity building providers face the challenge of finding, training and maintaining qualified staff for the provision of high-quality services

Remittances are a pivotal, though often unseen, driver of economic growth across Africa, in particular having a positive pro-poor effect on health, education and human capital development. The continent’s remittance economy has grown quietly and organically, taking up an essential role not just as a safety net, but also as a catalyst for entrepreneurship. Why is this so important? Because it changes how we should think about remittances: these flows are international development finance by another name, with the potential to be highly targeted, efficient and effective.

Remittances are an efficient, impactful and resilient form of development capital. FSD Africa has supported research by Cenfri which shows that the value of remittances in sub-Saharan Africa (SSA) is almost equal to that of “traditional” foreign capital flows such as overseas development assistance (ODA) and foreign direct investment (FDI). And their impact is potentially greater – especially in areas like health and education. In 2015, the region received USD39 billion in FDI and USD37.1 billion in ODA, compared to USD34.6 billion in remittances. However, between 2012 and 2015, formal flows of remittances grew at a higher growth rate than both FDI and ODA. If we isolate the UK as a source of capital, between 2015 and 2016 remittance flows actually overtook the value of ODA and FDI combined. Cenfri’s most recent case study, Remittances in Uganda, tells us that remittances from the UK to Uganda amounted to USD275 million annually – more than double the amount of foreign aid from the UK.

Yet the cost to send money home remains high. The average cost of remittances to SSA is over 9% of the value of the transaction, compared to a global average of 7% (we dig deeper into this in our infographic on the cost of remitting money from the UK). We want to bring these costs down. Signatories to the UN’s Sustainable Development Goals have pledged to reduce the average transaction costs of remittances to less than 3% of the amount transferred by 2030, with no remittance corridor costing more than 5%.

Our new research, Moving Money and Mindsets, shows an exciting new trend towards transferring money online. In 2016, 90% of remittances from the UK were being paid in cash at an agent. Fast forward two years, and we found that roughly half of focus group members now use online services – a significant and rapid switch in behaviour. Online remittances providers – like WorldRemit, Wave and TransferWise – not only provide transparency, security and convenience but are also significantly cheaper. It costs almost £16 to send £120 from the UK to Ethiopia in cash using an agent. The same amount costs only £6 to send online. Switching online clearly makes economic sense, so why stick to cash?

Some remittance markets are simply “stickier” than others. In countries with underdeveloped payment systems – like Zimbabwe, Sierra Leone and the DRC – cash is still king. For example, in the DRC, less than 10% of people have a bank account, and mobile money is virtually non-existent. Other barriers to switching to online services include the registration process, perceived security issues and technological barriers for older people. The solutions range from relatively easy quick fixes like simplifying the registration process and marketing online services to customers to longer-term interventions designed to develop digital payment infrastructures in Africa. Our Risk, Remittances and Integrity (RRI) Programme is working at the individual, regional and global levels to remove these barriers to switching to online, and to bring the transfer costs down. Cash may still be king in some countries in Africa, but cash is costly and with digital alternatives on the rise, its reign may be nearing its end.

Read FSD Africa’s new research, “Moving Money and Mindsets” here.

If you open the World Bank’s Global Financial Development Database and compare the data on private credit against total population, it is instructive to note the markedly different growth rates. In the developing economies of sub-Saharan Africa, credit extension has grown fairly impressively in the last 10 years albeit off a low base—from 10 percent to 18 percent. However, the total population of the region has grown by nearly a third, and now stands at 1 billion people. These disparate numbers suggest that credit is not growing fast enough to build the infrastructure and create the jobs needed to support this rapidly growing, young population.

THE IMPORTANCE OF CREDIT

For the majority who live on the continent, especially those living in cities contending with rising food and fuel prices, their ability to build or acquire assets is extremely constrained. For most people, access to credit is not about investing in buildings or businesses. It’s about managing daily challenges. In shor is a necessity, the means by which people can “stay in the game.”

For sure, easier access to credit—through, for example, credit and store cards as well as mobile-based loan product innovations like M-Shwari, Branch, and Tala—helps with consumption smoothing. But in Africa today there is not much that credit markets can offer the economically active “near poor” to help them build capital in a meaningful sense.

In developed economies, housing finance has allowed countless millions over the decades to build household wealth. Yet in Africa, mortgage markets are extremely thin. In Uganda, there are an estimated 5,000 mortgages for a population of 41 million while in Tanzania, there are only 3,500 mortgages in a country with a population of 55 million. Market dysfunction like this means that people without land or buildings do not benefit from the asset-price inflation that creates unearned wealth for those who already have capital, and so we see societies becoming dangerously divided and unequal.

Credit extension in Africa lags behind other regions of tha dramatic extent. While the ratio of credit to GDP is only 18 percent in sub-Saharan Africa, comparable figures in South Asia and Latin America are 37 percent and 47 percent, respectively. Across sub-Saharan Africa, central bankers and policymakers now realise that much bigger and better-functioning credit markets should be a priority outcome for their financial market reform strategies.

In the financial inclusion world, credit raises concerns because of the risks of over-indebtedness. Indeed, this is a worry in contexts such as in Kenya, where there has been a proliferation of different apps for online credit, and evidence is emerging that online credit is being used for unproductive activities, like online gambling. But we should not let this get in the way of the reality that Africa needs a lot more credit if economic development is keep pace with population growth.

Despite the importance of credit markets, we have not yet, collectively, made them a serious enough object of inquiry—and the consequs of not doing so are profound.

CREDIT MARKET REFORM

Credit market reform poses a challenge because credit straddles the entire financial market—from microcredit at the one end, through to capital markets, including project and bond finance, at the other. Credit also involves banks as well as non-bank financial institutions, including now fintechs and even telcos—so whose job is it to regulate credit markets? Central banks only? Or market conduct authorities with mandates that go beyond consumer credit into areas such as investor protection? Or dedicated credit regulators, such as South Africa’s National Credit Regulator? It is not always clear who should be responsible and so reform processes often lack leadership.

We also see credit market reform being promulgated in a fragmentary way. For example, strengthening credit market infrastructure tends to be the preserve of those interested in the development of small and medium enterprise finance, while consumer protection tend looked at through a responsible finance lens—when in fact the different elements interrelate. Credit market reform strategies should be much more joined up than they are.

There is currently no single African “observatory” monitoring the evolution of credit markets in Africa and no single Africa-based resource dedicated to combating credit market dysfunction. The past decade has seen numerous policy mis-steps in relation to credit markets, well-intended initiatives that have not been grounded in good evidence. Better information exchange might have prevented these mistakes. In Africa we lack effective mechanisms for knowledge sharing and peer learning around credit, a marked contrast to the plentiful knowledge sharing around related areas such as bank supervision and digital financial services.

There is also a vital need for African credit markets to take advantage of the increasing availability of concessional capital as donor organisations shift their funding towards returnable capital and awaant finance. Blended finance capital structures, with their ability to de-risk and pump prime lending, should encourage banks and other lenders to explore new markets in a sustainable way, in which risks are appropriately shared.

In addition, there is a fundamental need for much better data on credit markets. Without much more granular data by sector or by gender, it is going to be difficult for policymakers to implement effective strategies aimed at driving investment into essential industry sectors such as agriculture, housing, and infrastructure.

The Bank of Zambia, with support from FSD Africa, has been piloting an innovative scheme to improve data on credit markets. Under the scheme, all regulated financial institutions submit supplemental quarterly returns on their loan books to the central bank in return for which they get to see, in aggregate and by sector, trend data on the evolution of credit markets in Zambia. In this way, they can benchmark their own performance against the performance of tentire industry. We think this will spur competition and innovation by private credit providers. The Zambian authorities, meanwhile, now have the information with which they can make informed choices about where to take credit markets in Zambia, and how to manage risks but also, crucially, how to foster innovation and where to target support.

Note: The Africa Growth Initiative at The Brookings Institute first posted this blog on 1 August 2018. This is a reproduction from the original with AGI’s permission.

Note: This blog reflects the views of the author only and does not reflect the views of the Africa Growth Initiative.<

Setting the scene…

Blink and you might have missed it. But as dusk gave way to darkness on a sunny afternoon in Kigali, UNHCR Livelihoods, Access to Finance Rwanda (AFR) and FSD Africa received a brief but deeply significant email from Equity Bank Rwanda…

“This is to confirm that Equity Bank Rwanda will honor either proof of registration or refugee IDs as valid identification documents [to open a bank account]. We will issue a memo to all our branches to this effect before the end of the week”

18:18, Thursday 22 February, 2018

Kigali, Rwanda

Equity Bank Rwanda

This email marked another milestone for FSD Africa (UK aid’s Nairobi-based platform for inclusive financial sector work in sub-Saharan Africa) almost exactly 12 months of work in a new and important area: the financial inclusion of refugees and other forcibly displaced populations (FDPs).

The recent, rapid growth of FDPs in sub-Saharan Africa has created an urgent need to respond quickly to a complex and dynamic challenge. Through this blog, we wanted to capture what we’ve learned so far so…

Demand-signals: a new way to deliver humanitarian assistance…

Perhaps our most important realisation/conclusion is that refugee settlements are not only hubs for humanitarian assistance. They’re markets, too…

There are buyers and sellers supported by rules and institutions (both formal and informal), especially in larger, older refugee settlements such as Gihembe in Rwanda. And like most markets – these places have failures and pinch-points which inhibit the ability of FDPs to access and use, for example, financial services to help manage their lives.

And while the need for food, shelter and other safety net-type activities will remain, there is now good evidence (from our work and beyond e.g. this study by the IFC, which was featured in The Financial Times) that market-shaping and building has the potential to crowd-in the private sector to profitably deliver some of the goods and services that refugees need and can pay for themselves.

As a quick data point or two from Rwanda, primary FSD Africa and BFA research showed that 90% of refugee households earn $29+/month (the same as the median value of Rwandan bank account holders), while 43% have a secondary school education or more. Globally, 42% of all FDPs have been displaced for 5 years or more.

Identify and experience the market opportunity…

We’ve found that a lack of information is a major challenge. First, refugees are typically viewed by financial service providers as high risk (and low return) clients. Second, they are too often treated as a homogeneous, unsegmented group, dependent on humanitarian hand-outs.

This stereotyping is a tough nut to crack. It involves bridging knowledge gaps, but also long-held attitudes and behaviors. We quickly realised that market intelligence alone – on the financial lives of FDPs and business case for providing FDPs with financial access – just wasn’t enough. Financial services providers needed to see and feel the refugee market for themselves.

In November 2017, FSD Africa, AFR and UNHCR took bank decision-makers out of their offices in Kigali and into a refugee settlement for two nights to develop and test new/existing products, an approach which was replicated by colleagues at FSD Uganda in June 2018.

The transformation was remarkable, and something we started to document, in order to share with other banking decision makers in Kigali, East Africa and beyond.

“It is possible to serve the base of the pyramid, especially refugees, profitably; …I think I may have not necessarily seen the opportunity before I got here”

Patrice Kiiru, Equity Bank Kenya

The power of partnerships…

FSD Africa knew little about this space when we started out. We had theories to test, but little practical experience of accessing camps, refugee politics nor humanitarian assistance more broadly.

The only way we have been able to learn quickly is through the quality of our partners. For UNHCR Rwanda to speak with authority about the power of markets to deliver welfare enhancing outcomes to FDPs was refreshing and impressive in a space historically dominated by charitable giving and direct delivery.

“The way I see it, financial inclusion is really the key to unlocking the economic inclusion”

Jakob Oster, Livelihoods Officer, UNHCR Rwanda

We have built useful partnerships with a wide range of institutions, from commercial banks to charities, and from UN agencies to fintechs. Amongst them, UNHCR is our key humanitarian partner and, through our Innovation Competition FSD Africa and AFR are providing x5 £10,000 accelerator grants to CARE Rwanda, Equity Bank Rwanda, Tigo/Airtel Rwanda, Umutanguha and MFS Africa to develop new solutions to particular challenges faced by refugees. This commitment may be followed to larger investments (up to £150,000) to allow ideas to reach real scale. Beyond this competition, we’re continually looking for opportunities to engage interested, impactful private sector partners.

We have also built partnerships to maximise our local understanding and influence. AFR – a UK Aid, US Aid, Swedish Sida and MasterCard Foundation-funded ‘FSD’ programme for Rwanda – has been an invaluable support. Located in Kigali, with deep connections to the local banking system and regulators, the whole process has been made more effective. Within three months of beginning our work, AFR had successfully lobbied the Central Bank and MIDIMAR to add refugees to the Rwandan Financial Inclusion Strategy.

FSD Africa and AFR have also worked closely with DFID Rwanda.

“Market participation triggers wins for refugees, host communities and hosting governments. This new initiative has been a great demonstration of how to incentivise a market-driven response to a humanitarian challenge.”

Viola Dub, Private Sector Development Advisor, DFID Rwanda

This work falls within the context of a broader Government of Rwanda and DFID Rwanda approach to FDPs. In 2016, Rwanda – as an FDP host nation – signed up to the UN’s Comprehensive Refugee Response Framework, and with DFID Rwanda support is designing a plan for refugee integration.

The host community challenge/opportunity…

A crucial issue that we have struggled to grip is how to integrate host communities – ‘native’ settlements, often poor, rural and located nearby/adjacent to refugee settlements – into our programming. There are a number of stories about host community residents feeling that refugees benefit disproportionately from international aid and government agency support.

This is a difficult balance to strike. It is encouraging to see evidence that local communities benefit from hosting refugee communities, due to higher agricultural opportunities and incomes, but trickle down forces alone seem inadequate. Ensuring we work for host communities as well as FDPs means investing as much in understanding and responding to their specific needs as we do to the FDP. After all, their inclusion in our approach can only bolster the business case adding hundreds of thousands of potential clients.

“I was very surprised, because before arriving in the camps I was not expecting to find some real businesses in the camps; I was surprised to see someone with a business like other Rwandese outside of the camps.”

Theophile Nsabimana, Vision Fund Rwanda

Twelve month conclusions…

One year on, our successes (and failures) may lack the ‘flash-bang’ of a large DFI investment or a VIP launch, but we really can see the emergence of new markets.

FSD Africa and AFR are now seeding product/solution prototypes by more than five financial service providers in Rwanda. Refugees – young and old, male and female, short-term and long-term displaced – have expressed their demand for financial services to help manage their lives. The National Bank of Rwanda has incorporated refugee finance into its financial inclusion strategy, and banks now better understand that refugee IDs are eligible banking IDs (as per the introduction to this blog).

More broadly, we believe that we’re at the tipping point of genuine behaviour change within the private sector towards this group. FSD Africa and AFR received 23 applications to our refugee finance competition in December 2017, while only last week FSD Uganda and FSD Africa received more than 20 applications by MFIs, banks and fintechs just to visit camps to see the opportunity for themselves. FSD Africa is also about to start work replicating this approach in DRC, through our sister organisation ELAN RDC.

The proof is in the pudding. And we’ll be watching carefully to see: whether refugees can become long-term, profitable clients for the financial sector, but also whether finance can be genuinely useful to forcibly displaced people. But, for now at least, the market is on the move…

Refugees are not an obvious customer segment for financial service providers (FSPs). It is not hard to see why: in a world where refugees are too often portrayed as very poor, vulnerable, with few tangible assets and little stability, where are the incentives to enter such a challenging market?

While FDPs often are vulnerable, poor, and burdened with instability, through a different lens they can present an intriguing opportunity. In places like Rwanda, large refugee camps can exist for decades and are home to vibrant micro-economies. Moreover, many FDPs fit the basic profile to access formal financial services; they have regular income, formal identification, and a need for financial products.

A study conducted by BFA Global in partnership with FSD Africa, Access to Finance Rwanda[1] (AFR), and UNHCR last year suggests that there are good reasons to believe that forcibly displaced persons (FDPs) can be a profitable customer group for FSPs.

Demand: Refugees Need Financial Services

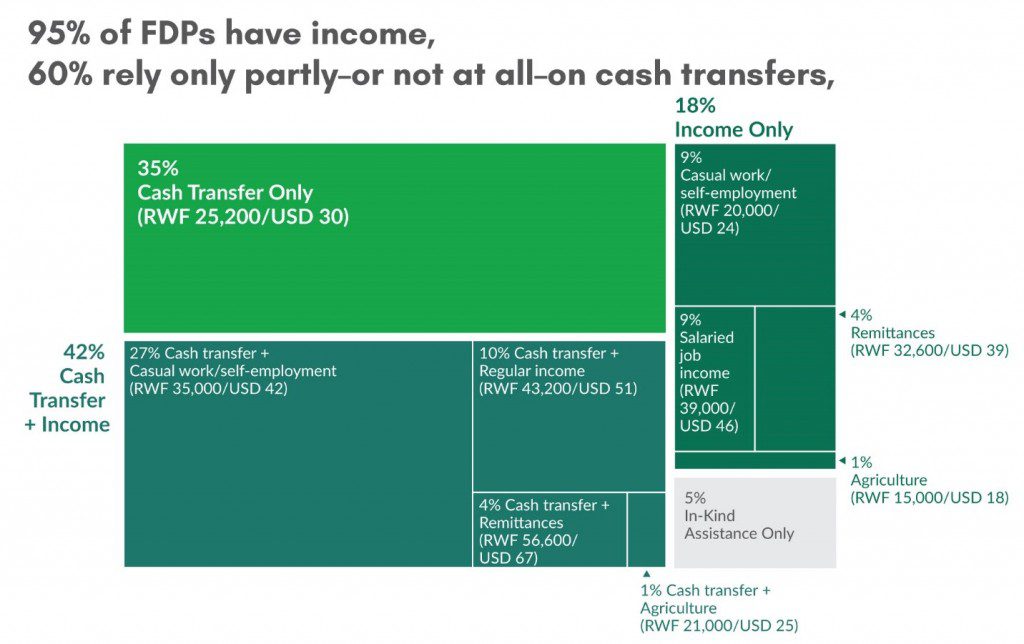

Many refugees not only receive aid, they also earn income, thereby creating sufficient cash flow to drive demand for financial services.

Although they are plagued by instability and insecurity, many refugees start businesses and some also have jobs. About a third, or 27% of refugees, are self-employed, providing services such as dressmaking and barbering largely within the camp. An additional 10% of refugees earn a monthly salary from employment. Finally, 4% receive remittances.

In addition to the income earned from work, 95% of refugees receive humanitarian aid in the form of monthly cash transfers. The World Food Programme (WFP) and the UNHCR are shifting from providing refugee households with in-kind humanitarian support to giving them cash. At the time of our study, refugee households in four out of the six camps in Rwanda were receiving monthly cash transfers. The other two camps were soon to migrate from in-kind to cash transfers.

With these regular inflows of cash, refugees need a place to receive and store their money, creating a clear demand for secure financial services.

Supply: Refugees can be a profitable segment

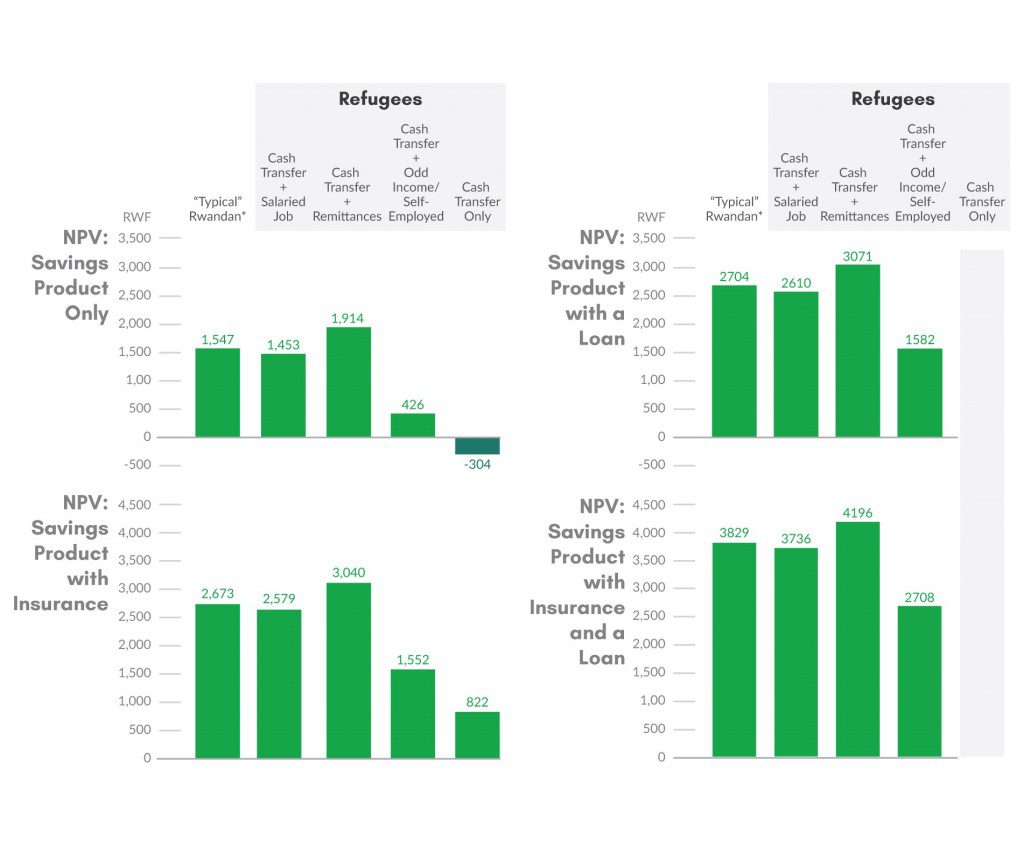

Not only is there substantial demand for financial services, our analysis suggests refugees are a viable customer segment. Of the 160,000 men, women and children who are displaced in Rwanda, we estimate that about 44,000 adults have sufficient monthly cash flow to make them viable customers for FSPs, with additional opportunities for cross selling.

To start, the basic transaction accounts that banks offer other low-income Rwandans would likely be even more successful with refugees who have regular, stable cash flows. Moreover, accounts that refugees open to receive their monthly cash transfers are notlikely to become dormant or inactive, as is generally the case with many low balance accounts, making refugees a more attractive proposition for banks.

In addition, there are opportunities for cost savings using mobile money. Although low-income households tend to use informal mechanisms such as savings groupto manage their finances, 90% of the refugees we interviewed use mobile money regularly and 95% already have experience using a bank account, thereby decreasing upfront training and client education costs.

Finally, there are opportunities to cross sell other products although many segments are profitable with just a savings product. Our dynamic net present value model estimates FSPs can profitably serve refugees with salaried jobs, those who are self-employed, and those who receive regular remittances with only a savings proposition! In fact, we believe that these three segments, who together make up 41% of the adult refugee population, can be just as profitable to FSPs as typical low-income account holders in Rwanda.

That said, FSPs that offer only a savings product to refugees who depend solely on cash transfers are not likely to have a profitable proposition. Targeted cross-selling of other financial products, such as a loan or micro-insurance, will be needed to improve the FSP’s profitability for this segment.

Regulatory Environment: Refugees Qualify for Financial Services

Given the significant forces for demand and supply, the regulatory environment is the last piece of the puzzle. Fortunately, we found that refugees meet the formal requirements for opening a bank account in Rwanda.

Although most refugees do not have a government-issued ID card (which FSPs typically use for KYC purposes), all refugees have a proof of registration document issued by the Ministry of Disaster Management and Refugee Affairs. FSPs that want to serve refugees can request regulatory approval to use the proof of registration document to open accounts; the National Bank of Rwanda has approved such requests in the past.

Ultimately, our research suggests that FSPs shouldn’t be guided by the stereotypical narratives about refugees. We found that while refugees face difficult circumstances, they are also viable customers for FSPs that take an innovative approach to product design and customer acquisition.

As added incentive, in December 2017, FSD Africa launched an innovation competition to provide FSPs with ideas about how to bring financial access to refugees with grant funding of up to £160,000. The competition has received 21 concept notes to date.

[1]Rwanda is a signatory to the 1951 Convention relating to the Status of Refugees[1], which guarantees refugees the freedom of movement, right to work and other liberties and has been hosting refugees for over 20 years.

[1] BFA’s calculations based on the Maastricht Graduate School of Governance (2016) data set from a research conducted in May 20

This month, we celebrate International Women’s Day united in the 2018 theme “Press for Progress.” While much of the discussion is around how global actors are pressing for progress on women’s equality at the macro level, I’d like to take a deeper look at how a low-income woman presses for progress in her own financial life.

Our program, Financial Sector Deepening Africa (FSD Africa), funded by UK aid from the UK government, is supporting Women’s World Banking’s partnership with Diamond Bank in Nigeria to improve access and usage of savings accounts among low-income clients, particularly women.

Three years into this partnership, we’re starting to understand just how transformational saving with a formal institution can be for women.

Women’s World Banking’s global research shows that women have specific and often complex savings needs. They are juggling scarce resources to cover day-to-day expenses with an eye toward the future. They save against emergencies and toward goals such as education and business growth.

However, low-income women often face barriers to accessing a safe place to save due to mobility and time constraints as well as low levels of financial literacy. They are forced to save in less reliable ways: at home in a drawer or under a mattress, by buying excess stock for their businesses or through a neighborhood savings club.

In Nigeria, Women’s World Banking’s research revealed a strong savings culture. Women running businesses in the bustling urban markets of Lagos put aside as much as 60 percent of their daily income in informal savings tools such as ajo, adako and other methods. What was most surprising though—these women’s businesses were located literally steps from bank branches. Why were they not opening savings accounts?

The answer—the distance is emotional, not physical. These market women are familiar with banks yet they do not see them as relevant or accessible. Even those who have accounts usually place most of their money in traditional, though more informal, financial tools. Diamond Bank set out to close this gap by offering an innovative and relevant savings product that crosses the barriers preventing low-income Nigerians from accessing formal financial services.

Planting a Seed: A transformational savings account

The BETA (meaning “good” in pidgin English) account targets self-employed market women and men who want to save frequently (daily or weekly). The account can be opened in less than five minutes and has no minimum balance and few fees.

Because these clients, especially women, value convenience, the product is built around serving women in the market where they work. Agents, known as BETA Friends, visit a client’s business to open accounts and handle transactions, including deposit and withdrawal, using a mobile phone application.

With support from FSD Africa, Women’s World Banking and Diamond Bank are expanding on the BETA proposition to offer women more financial tools and services, including BETA Target Savers, a long-term savings account to help clients work toward larger goals.

Today, Diamond Bank has more than 520,000 new savings account holders who are using these valuable tools, more than 197,000 of whom are women. That’s more than a half million low-income clients who did not previously have access to Diamond Bank, a bank often just steps away from their businesses.

One woman client, who has BETA Friend agents visiting her market stall regularly to collect deposits, put it quite simply:

I want them to be coming around often so that I can save my money, so I can use it to do better things for myself.

With Target Savings, we’re hearing a similar sentiment. A woman client said,

You keep your money to achieve what you want to do. You keep in the back of your mind to achieve your goal.

When we look at how women are able to “press for progress” in their own lives, we know that true financial inclusion is not just about opening accounts, but meaningful usage of these accounts to achieve financial goals and build a better future. Women’s World Banking’s partnership with Diamond Bank is at an exciting phase of the project where we can start to understand just how transformational these savings accounts will be.

While we’re in the very early stages of analyzing the data, Women’s World Banking is looking at exactly how clients are doing this. After conducting a baseline survey in 2015 as well as a follow up survey in late 2017 to measure how clients are using the savings accounts to improve their lives, we are seeing promising early results, specifically in using savings to grow businesses and achieve goals.

Clients are reporting using their savings to fund business expansion. This is a critical point as financial services for low-income women are often associated with micro loans, and while credit is an important tool, savings is essential for women to grow their businesses.

Additionally, time and time again, when Women’s World Banking asks women about their primary savings goals, education for their children is at the top of the list. Initial survey results are showing that BETA clients are saving for their children’s education and are more likely to have all of their school-aged children in school.

On International Women’s Day, we’re happy to celebrate these promising signs of progress for women in Nigeria. We look forward to continuing to learn more about how savings tools can help women to press for progress.

This blog was published by Women’s World Banking http://www.womensworldbanking.org/news/blog/international-womens-day-women-save-succeed/

Join us in celebrating International Women’s Day 2018!

Through our #PressforProgress campaign, we are proud to share information about our partnerships that are supporting women’s economic empowerment in a variety of ways.

The Fletcher School Leadership Programme for Financial Inclusion is an intensive and innovative executive education initiative for promising financial regulators and policymakers from emerging and frontier markets, including in sub-Saharan Africa. Through support from FSD Africa, the Bill & Melinda Gates Foundation and the MasterCard Foundation, the programme has trained financial regulators and policy makers, including 40% women, with many going on to develop and implement policies that address financial inclusion in their respective countries, including for women.,

Just as in technology and finance industries around the world, fintech companies in Africa are grappling with a severe under-representation of women in leadership roles and throughout their businesses. When compiling the data in the 2017 Fintech Talent Africa report, Digital Frontiers Institute (DFI) made gender balance a particular focus of the research, knowing that this is a significant problem in the industry.

The findings of the report validated this belief. More than 400 industry leaders and professionals responded to the survey and of these, only 12.5% were women. The gender gap was reflected again in the data they reported: respondents indicated that the teams they lead are made up of approximately 39% women, while senior or executive teams are made up of 43% women. This data highlights that there is still a way to go in order to achieve gender parity.

To learn more about addressing the gender gap in fintech, access the full blog via this link.,

Join us in celebrating International Women’s Day 2018!

Through our #PressforProgress campaign, we are proud to share information about our partnerships that are supporting women’s economic empowerment in a variety of ways.

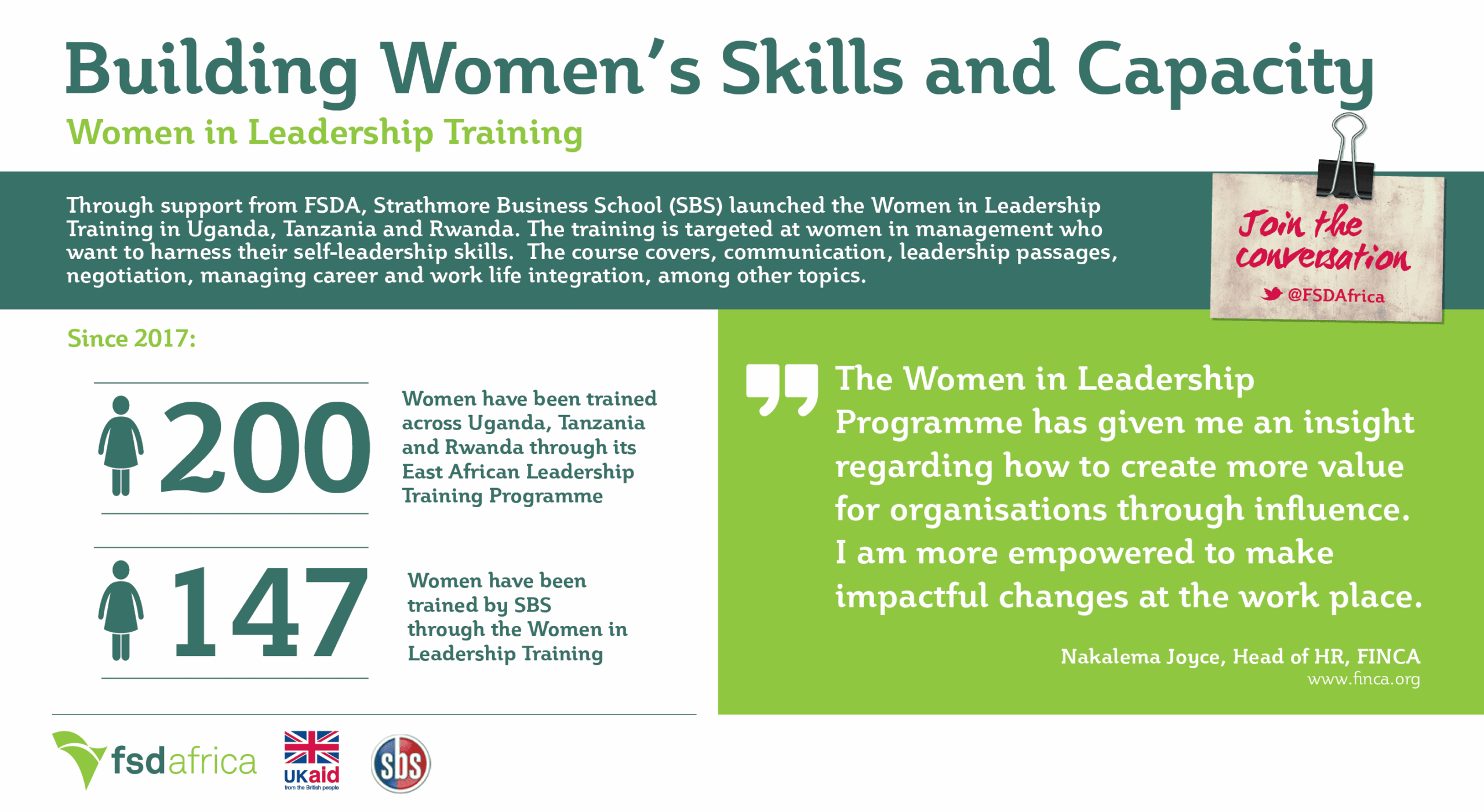

The Strathmore Business School (SBS) is a renowned institution in East Africa that aims at developing transformative business leaders to tackle the various social and economic challenges facing Africa. With support from FSD Africa, SBS has developed and expanded its Leadership Academy in East Africa including creating a ‘Women in Leadership’ programme. The programme is targeted at women in management and equips women with skills to perform effectively and efficiently to achieve excellence in the various spheres of their lives.

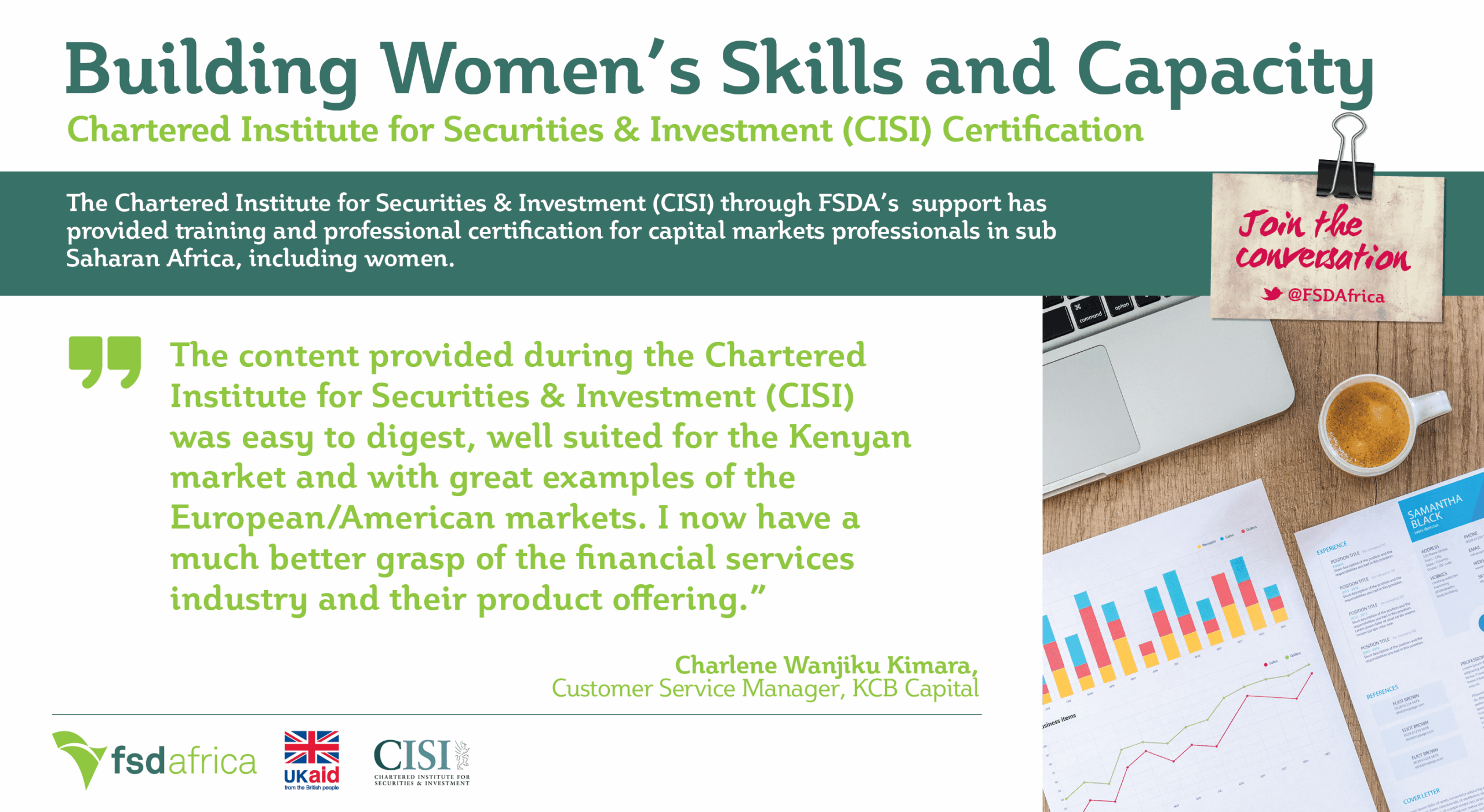

Additionally, The Chartered Institute for Securities & Investment (CISI) through FSD Africa’s support, is providing skills development and training in order to strengthen professional standards among Capital Markets Professionals – women included. CISI is a professional body that offers a wide range of qualifications in the financial sector including Operations, Wealth Management, Compliance/Risk, Capital Markets/Corporate Finance, Financial Planning and Islamic F