Experts argue that tax systems in most African countries favor investments in “brown” rather than “green” economies and this is prohibiting investments in renewable energy.

Read original article

Experts argue that tax systems in most African countries favor investments in “brown” rather than “green” economies and this is prohibiting investments in renewable energy.

Read original article

FSD Africa’s 2023 Development Impact Report discusses our progress against our sustainable finance strategy and is the second since we began implementing the strategy in April 2021. Other than progress, we also share the lessons we have been learning along the way on how to make finance work harder for Africa, both for current and for future generations.

In 2023, we celebrated two key milestones – the 10th anniversary of FSD Africa, and the coming of age of FSD Africa Investments. FSD Africa Investments turned six this year and has so far committed £92m pounds. Together, FSD Africa and FSDAi, have delivered value to over 12 million people and 3.2 million businesses, and have helped strengthen the financial markets in over 30 African countries.

While we celebrate several milestones, we are cognisant of the challenges that African countries continue to face in mobilising sufficient finance for climate and social development goals. That is why we are now placing a greater emphasis on new ways of mobilising finance for the continent’s sustainable development – through innovative climate finance solutions, leveraging Africa’s natural capital, and developing carbon markets. We emphasise the unique opportunities and resources that Africa has, and can bring to bear, in solving the climate and development challenge we all face.

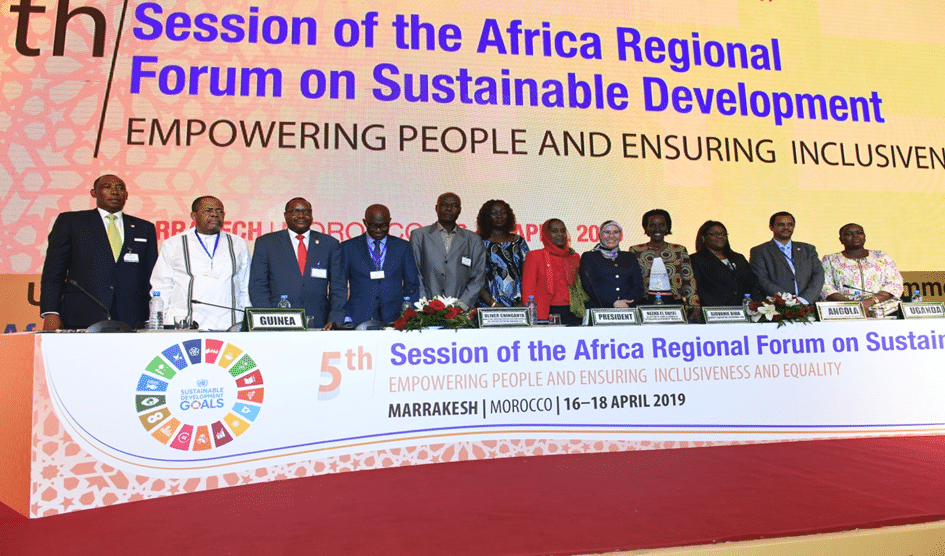

As international headlines chart the terrible suffering caused by flooding, earthquakes and wildfires, a less headline-grabbing, but nonetheless hugely significant, good news story has emerged from Nairobi, Kenya. The African Climate Summit, which concluded on September 6, was a huge success story for Africa and for Kenyan President William Ruto.

Pledges directed to African climate change adaptation and litigation amounting to $26bn have emerged from the summit. That’s not enough to solve Africa’s climate challenges, but even if only a fraction of this sum materialises, it will have a real impact on the ground.

Even more consequential in the long term is the consensus that emerged from the conference around the need for economic growth that delivers both prosperity and environmental benefits. The fact that a consensus was achieved is significant, because it strengthens Africa’s position for the forthcoming COP28 conference in Dubai in November. Furthermore, the admission of the African Union to the G20 means the African voice is getting louder and clearer on the world stage.

Importantly, the summit’s adoption of the Nairobi Declaration, which commits African countries to develop and implement “policies, regulations and incentives aimed at attracting local, regional and global investment in green growth and inclusive economies”, is also a signal that Africa will look for other strategies to support climate action, alongside the $100bn a year promised by developed nations in 2009.

Indeed, the summit was most of all an assertion of African self-determination and specifically the need to mobilise Africa’s domestic private capital in the continent’s climate efforts. Relying on international finance creates a dependency that Africa does not want. Put simply, Africa has determined that its own resources must be channelled, supported by a financial market architecture which ensures that states can absorb climate finance effectively, distributing it where it is most needed.

But if it is to do this, the current situation – in which less than 0.5% of domestic institutional assets under management are invested in alternative assets – cannot continue. As was argued powerfully at the launch of the Pan-African Fund Managers’ Association at the beginning of the summit, we need to think about how we can put in place not only the policy and regulatory incentives but also the instruments and the financial architecture to drive much more of the$1.4tn of institutional capital in Africa towards climate and nature-positive projects.

Crucially, this will mean more use of de-risking strategies such as credit guarantees to persuade pension funds to de-emphasise the easy but less safe option of government securities and to invest in green assets. It will also require sources of donor and philanthropic capital to step up their support for project development, for example through the use of challenge funds or by investing in intermediaries that are closer to the market as a way of reaching the more innovative start-ups and entrepreneurs who will drive the new green economy.

[Current] global prudential regulations can make it economically impossible for large institutional investors to allocate capital to African projects.

Moreover, the summit underlined an important issue that has seen Africa’s financing needs neglected, namely the need for reform of the global prudential regulations, which can make it economically impossible for large institutional investors to allocate capital to African projects. There should be a global review of these constraints, perhaps led by the G20.

Even with such reforms, African governments, many of which are battling with high levels of debt, will need to be both agile and visionary if they are to compete at a time when the world’s biggest economies are offering big incentives to attract green investment. Though deeply political, carbon taxes could be one way to go, but would need to be sensitively introduced. Other green fiscal incentives, balancing out tax breaks for green investment by removing subsidies for dirty industries, are also essential for governments to be able to direct their economies towards a greener future.

The UN Framework Convention on Climate Change has just released its first global stocktake report, highlighting yet again that, despite a major global effort, progress since the Paris Agreement has been inadequate. The report recommends greater commitment to transformation across all sectors and recognises the need for more access to climate finance for developing countries in line with the key recommendations from the Nairobi Summit.

If we get this right, the prize is very significant and the message from the summit is that Africa will not wait. Instead, it is determined to grab the opportunities of a new green growth pathway now, as are an increasing number of investors, and that has to be good for us all.

We, the African Heads of State and Government, gathered for the inaugural Africa Climate Summit (ACS) in Nairobi, Kenya, from 4th to 6th September 2023; in the presence of other Global Leaders, Intergovernmental Organizations, Regional Economic Communities, United Nations Agencies, Private Sector, Civil Society Organizations, Indigenous Peoples, Local Communities, Farmer Organizations, Children, Youth, Women and Academia:and Government in the presence of global leaders and high-level representatives on 6 September 2023 in Nairobi Kenya

In witness of which we the African Heads of State and Government assembled in the (venue) of the Kenyatta International Convention Centre in Nairobi now make this declaration in the presence of global leaders and high-level representatives on this 6th day September 2023, in Nairobi, Kenya

“In a short space of time, we have strengthened and developed financial markets and tapped into capital by using new instruments such as green and gender bonds,” says Mr Mark Napier, CEO of FSD Africa.

FSD Africa, a UK Aid funded specialist development agency, on 27th March celebrated a decade of strengthening financial markets across Africa, growing economies, increasing incomes for vulnerable populations and combatting poverty.

FSD Africa has made significant strides over the past decade by advancing policy and regulatory reforms, enhancing financial infrastructure and increasing capacity, all while tackling systemic issues in Africa’s financial markets. These efforts have led to large-scale and long-term change, providing access to financial services to over 10.2 million people and addressing issues related to financial exclusion.

During the Covid-19 pandemíc, FSD Africa observed a remarkable 87% increase in the demand for and use of remittance services, which played a crucial role in protecting families from Covid-19’s financial impacts.

FSD Africa’s market-building initiatives have resulted directly or indirectly in £1.9 billion of long-term capital made available for SMEs, affordable housing and sustainable energy projects, among others. Its support for financial sector innovation has increased access to financial services for close to 12 million Africans, while its support for business growth has improved access to finance for more than 3 million African businesses and led directly or indirectly to the creation of over 35,000 new jobs.

“Celebrating over ten years of our trailblazing work across Africa is special,” said Mr Mark Napier, CEO of FSD Africa. “In a short space of time, we have strengthened and developed financial markets and tapped into capital by using new instruments such as green and gender bonds.”

FSD Africa’s strategy has evolved to address the continent’s expanding needs, with a greater emphasis on identifying innovative methods to mobilise resources for sustainable economic development. The organisation has recently boosted investment into projects that enable an equitable transition to a green future for Africa after several successful initiatives, including developing regulations and assisting green bond issuance programmes in Kenya and Nigeria.

The organisation’s green portfolio and pipeline have expanded because of continuous investments in programmes that provide environmental and social consequences, with close to £50 million being invested in green initiatives.

Ms Jane Marriott, OBE, British High Commissioner to Kenya said the UK is continually working with Kenya to promote green finance and economic growth as part of its strategic partnership with Kenya. FSD Africa is delivering on these priorities in Kenya and across the continent, creating over 35,000 jobs and leveraging more than Ksh300 billion into sectors like renewable energy.

Kenya’s National Treasury Cabinet Secretary Prof Njuguna Ndung’u, said Kenya’s partnership with FSD Africa has created a favourable environment for the growth of local capital markets, resulting in increased interest from both domestic and foreign investors.

“FSD Africa also played a crucial role in establishing the Nairobi International Financial Centre (NIFC), positioning Kenya to receive more financial flows,” Prof Ndung’u said. “We look forward to collaborating more closely with FSD Africa on green finance initiatives to promote sustainable development while addressing climate change challenges.”

Read original article

FSD Africa, a UK aid funded specialist development agency, today celebrated a decade of strengthening financial markets across Africa, growing economies, increasing incomes for vulnerable populations, and combatting poverty.

FSD Africa has made significant strides over the past decade by advancing policy and regulatory reforms, enhancing financial infrastructure and increasing capacity, all while tackling systemic issues in Africa’s financial markets. These efforts have led to large-scale and long-term change, providing access to financial services to over 10.2 million people and addressing issues related to financial exclusion. During the Covid-19 pandemic, FSD Africa observed a remarkable 87% increase in the demand for and use of remittance services, which played a crucial role in protecting families from the pandemic’s financial impacts.

FSD Africa’s market-building initiatives have resulted directly or indirectly in £1.9 billion of long-term capital made available for SMEs, affordable housing and sustainable energy projects, among others. Its support for financial sector innovation has increased access to financial services for close to 12 million Africans, while its support for business growth has improved access to finance for more than 3 million African businesses and led directly or indirectly to the creation of over 35,000 new jobs.

Speaking during the event, Mark Napier, CEO at FSD Africa said: “Celebrating over ten years of our trailblazing work across Africa is special: in a short space of time, we have strengthened and developed financial markets, and tapped into capital by using new instruments such as green and gender bonds. The future is key, and I look forward to continuing our hard work with our collaborative and innovative team. I have no doubt that we will continue to support and address Africa’s expanding needs as we move towards sustainable economic development.’’

Future-focused, FSD Africa’s strategy has evolved to address Africa’s expanding needs, with a greater emphasis on identifying innovative methods to mobilise resources for sustainable economic development. The organisation has recently boosted their investment into projects that enable an equitable transition to a green future for Africa after several successful initiatives, including developing regulations and assisting green bond issuance programmes in Kenya and Nigeria. The organisation’s green portfolio and pipeline have expanded because of continuous investments in programmes that provide environmental and social consequences, with close to £50 million being invested in green initiatives.

Jane Marriott, OBE, British High Commissioner to Kenya said: ‘”The UK is continually working with Kenya to promote green finance and economic growth as part of the UK-Kenya Strategic Partnership. FSD Africa is delivering on these priorities in Kenya and across the continent, creating over 35,000 jobs and leveraging more than KES 300 billion into sectors like renewable energy. I look forward to FSD Africa’s continued work in the years ahead.”

Prof. Njuguna Ndung’u, Cabinet Secretary, Kenya National Treasury said: ‘’Kenya’s partnership with FSD Africa has created a favourable environment for the growth of our local capital markets, resulting in increased interest from both domestic and foreign investors. FSD Africa also played a crucial role in establishing the Nairobi International Financial Centre (NIFC), positioning Kenya to receive more financial flows. We look forward to collaborating more closely with FSD Africa on green finance initiatives to promote sustainable development while addressing climate change challenges.’’

Read original article

FSD Africa, a UK aid-funded specialist development agency, today celebrated a decade of strengthening financial markets across Africa, growing economies, increasing incomes for vulnerable populations, and combatting poverty.

FSD Africa has made significant strides over the past decade by advancing policy and regulatory reforms, enhancing financial infrastructure, and increasing capacity, all while tackling systemic issues in Africa’s financial markets.

These efforts have led to large-scale and long-term change, providing access to financial services to over 10.2 million people and addressing issues related to financial exclusion. During the Covid-19 pandemic, FSD Africa observed a remarkable 87% increase in the demand for and use of remittance services, which played a crucial role in protecting families from the pandemic’s financial impacts.

FSD Africa’s market-building initiatives have resulted directly or indirectly in £1.9 billion of long-term capital made available for SMEs, affordable housing, and sustainable energy projects, among others. Its support for financial sector innovation has increased access to financial services for close to 12 million Africans, while its support for business growth has improved access to finance for more than 3 million African businesses and led directly or indirectly to the creation of over 35,000 new jobs.

Speaking during the event, Mark Napier, CEO at FSD Africa said: “Celebrating over ten years of our trailblazing work across Africa is special: in a short space of time, we have strengthened and developed financial markets and tapped into capital by using new instruments such as green and gender bonds. The future is key, and I look forward to continuing our hard work with our collaborative and innovative team. I have no doubt that we will continue to support and address Africa’s expanding needs as we move towards sustainable economic development.’’

Future-focused, FSD Africa’s strategy has evolved to address Africa’s expanding needs, with a greater emphasis on identifying innovative methods to mobilize resources for sustainable economic development. The organization has recently boosted its investment into projects that enable an equitable transition to a green future for Africa after several successful initiatives, including developing regulations and assisting green bond issuance programs in Kenya and Nigeria. The organization’s green portfolio and pipeline have expanded because of continuous investments in programs that provide environmental and social consequences, with close to £50 million being invested in green initiatives.

Jane Marriott, OBE, British High Commissioner to Kenya said: ‘”The UK is continually working with Kenya to promote green finance and economic growth as part of the UK-Kenya Strategic Partnership. FSD Africa is delivering on these priorities in Kenya and across the continent, creating over 35,000 jobs and leveraging more than KES 300 billion into sectors like renewable energy. I look forward to FSD Africa’s continued work in the years ahead.”

Prof. Njuguna Ndung’u, Cabinet Secretary, Kenya National Treasury said: ‘’Kenya’s partnership with FSD Africa has created a favorable environment for the growth of our local capital markets, resulting in increased interest from both domestic and foreign investors. FSD Africa also played a crucial role in establishing the Nairobi International Financial Centre (NIFC), positioning Kenya to receive more financial flows. We look forward to collaborating more closely with FSD Africa on green finance initiatives to promote sustainable development while addressing climate change challenges.’’

Read original article

These trees are Gabon’s superstars. They absorb and store millions of tons of earth-warming carbon dioxide each year, a critical function for the global fight against climate change. They also fuel the country’s timber industry, a major focus of economic development during the past decade.

In today’s financial markets, Gabon’s trees are worth more dead than alive. Despite the billions pledged worldwide to fight climate change, little has been distributed as compensation for the global benefit that trees provide. In 2021, Gabon received its first payment for reducing forest-related emissions—$17 million via the Central African Forest Initiative.

The timber industry, on the other hand, contributes about $1 billion to Gabon’s annual gross domestic product. It could be a great deal more. Unlike some of its neighbors, the country strictly limits logging, palm oil production and other activities that lead to forest destruction; it’s suffered less than 1% forest loss since 1990, compared with about 14% for continental Africa.

Now that oil production, the country’s primary source of revenue, is dwindling, leaders are reevaluating the money-making potential of the forests. Opening more land to timber companies is one option, but for now Gabon’s environmentally minded government is more interested in keeping the trees alive—if the international financial markets can make it worthwhile.

The best avenue for that, Gabon says, is the $2 billion-and-growing market for “carbon offsets.” That’s traditionally been limited to those who can document improvement on past environmental practices, not those who, like Gabon, never wrecked their forests in the first place. That’s because for a carbon offset to fulfill its function of compensating for its buyer’s emissions, it needs to have financed something that wouldn’t have happened otherwise. But in Gabon, forest protection has been happening anyway.

Still, Gabon insists it should be compensated for the air-purifying service its trees provide. Otherwise, it hints, its commitment to forest preservation may take a backseat to more traditional economic development. In its recent national action plan under the Paris Agreement, the global climate pact, the country says it plans to remain a “net-carbon absorber”—if it gets access to international finance through a carbon market.

“There is no financial instrument to support Gabon to continue to offer this critical ecosystem service,” Akim Daouda, the chief executive officer of Gabon’s $1.9 billion sovereign wealth fund, said in an interview during a recent trip to London. “Can we monetize the forest and keep it for the rest of the planet? Or do we need to find a way to respond to the needs of our population?”

Gabon’s per capita GDP is the highest on the continent, but there’s little evidence of wealth past or present in Nyanga. One of the few local health centers lacks running water, exposed wires poke out of the walls, and bare mattresses cover four, cast-iron bedframes.

The province is home to a 100,000 hectare (247,000 acre) cattle ranch, part of the Grande Mayumba project. A flagship of Gabon’s “sustainable development” efforts and backed by investments from the family offices of the Westons, Fricks and Sarikhanis, Grande Mayumba’s plans include logging, cattle farming and eco-tourism, as well as an area 37 times the size of Manhattan set aside for conservation.

The ranch raises N’Dama, a small chestnut-colored breed of indigenous beef cattle that tolerate tsetse flies and the sleeping sickness they carry. The 4,000-strong herd will grow and eventually roam alongside wild buffalo and antelope. The free-range model will minimize harm to the savannah ecosystem, and careful grasslands management could boost the soil’s carbon stock, according to Africa Conservation Development Corp., Grande Mayumba’s parent company.

The ranch isn’t profitable yet. So far, only Grande Mayumba’s logging operation is fully operational. The rest has moved far more slowly. To raise the money needed to really get the project off the ground, ACDG will need to issue and sell carbon credits.

The forest-based carbon offsets on the market today tend to be based on projects that seek to avoid emissions or increase carbon storage. Limiting deforestation usually qualifies; so could planting trees. Developers usually calculate how the forests fared under their control compared with a historical baseline, then sell the difference in units of extra tons of carbon removed or avoided as offsets.

But because Gabon already has stringent restrictions on logging and there’s little deforestation to speak of, ACDG has had to take a different approach. Based on trends in more than a dozen once-highly forested countries, it contends there’s an imminent threat to the trees in Nyanga. Pending government approval, ACDG will sell credits based on how Grande Mayumba’s activities avert that hypothetical future destruction.

“There will be development in the Grande Mayumba area over time,” said Rob Morley, science and environmental planning director at ACDG. “This will either be unsustainable, unplanned and that will lead to a large amount of forest loss, or it will be planned.”

On the ground, the threat feels distant. About the size of Israel, the province is Gabon’s poorest, with just three paved roads, two hospitals and few public services. Residents have gone looking for better opportunities in Gabon’s main cities, leaving a population of around 53,000.

The Grande Mayumba project says it will generate as many as 4,000 jobs, mirroring President Ali Bongo’s Gabon Émergent, the country’s three-pillar development strategy based on industry, the environment and a services economy. Most will work in forestry or ranching, but a handful will staff a luxury ecolodge under construction in neighboring Ogooué-Maritime province. For $2,000 per night or so, well-heeled tourists will be able to see hippos frolic in the surf and ghost crabs dash in and out of the waves.

When ACDG figures out how to stabilize a runway on the sandy soils, guests will be able to access the lodge by plane. Until then, it’s a half-day journey from the nearest main town, by car, river barge and speedboat. The last leg is by quadbike along a strip of beach frequented by buffalo and the odd elephant, tide permitting.

In its original plans, Grande Mayumba expected its model to generate as many as 200 million credits over the next 25 years. At today’s prices, that would be worth about $2 billion, according to data provider Allied Offsets, roughly equal to Gabon’s sovereign wealth fund.

So far that’s yet to materialize. The British bank Standard Chartered Plc and Swiss trading firm Vitol SA have expressed interest, but neither have culminated in a deal. Investors are getting antsy.

Josh Ponte, a former gorilla researcher and special adviser to the President of Gabon and now an ACDG director, bemoaned the delay in carbon-credit revenue.

“The carbon play was a core incentive,” he said, sitting on a rudimentary platform that will eventually be a dining room. Other than some staff lodging, there’s little more to see. “But there’s since been a reality check on the timeline of the carbon credits, how they’ll work, and how they’ll fit with government strategy. It’s really tiring our investors.”

Gabon Vert, the environmental pillar of the Bongo administration’s development plan, frames both its deal with ACDG and the country’s plans to issue its own, sovereign carbon offsets. Gabon’s offering will rely on different math. It plans to tally the CO2 its trees suck out of the atmosphere, subtract its own emissions, and sell the difference to other, more polluting countries as “net sequestration” credits.

Anyone can issue carbon credits, and anyone can buy them. Most developers use third-party verification bodies to vouch for the quality of their offerings. Gabon doesn’t plan to do so. Fledgling exchanges are also trying to streamline trade, but for now, over-the-counter, bilateral deals are the most common.

It’s not clear the markets will bite. Gabon’s plans have been met with caution. It’s yet to sell some 90 million credits it already generated for past carbon absorption using an established albeit contested approach.

“It always makes me nervous when people say they’re going to roll out their own methodology,” said Danny Cullenward, policy director at nonprofit research group CarbonPlan. “It’s really easy to manipulate the methodology intentionally or incidentally to produce outcomes that are less credible or inconsistent with other key points of data.”

Methodology aside, political uncertainty hangs over Gabon. The fate of Gabon Vert may depend on the outcome of the presidential election later this year.

Though a member of the Bongo family has led Gabon for the past 56 years, the current presidency is under a cloud. Ali Bongo won his most recent election by fewer than 10,000 votes, triggering charges of ballot-rigging and days of violent protest. A 2019 coup attempt failed, and Bongo has had a stroke.

Ahead of this year’s presidential election, the government has embarked on an aggressive green diplomacy push. In February, a delegation joined the UK’s environment ministry and King Charles III to chat conservation. This week, Emmanuel Macron will attend a “One Forest” summit in Libreville, the first time a French president has visited the country in about a decade.

The Grande Mayumba project was already halted once, in 2015, when Gabon’s then-oil minister gave the site of a proposed port to a Moroccan company, despite an agreement that assigned it to ACDG. Development stalled until the dispute was resolved in 2018.

“If the president were to change, I’m not convinced that the model has got deep enough roots yet to be fully sustainable,” said Lee White, environment minister in Bongo’s government. The project also is facing a groundswell of opposition from local communities and NGOs. A grassroots campaign called “No to Grande Mayumba” calls for the suspension of the plan, saying restrictions on access to resources threaten the custom and livelihoods of subsistence farmers who haven’t been adequately consulted.

“There’s sacred forest here and the local population should be consulted on what can and can’t be cut down,” said Nicole Nouhando, governor of Nyanga province who’s broadly supportive of ACDG’s plans.

ACDG has had its own turmoil. Alan Bernstein, the South African safari entrepreneur who founded the company, left after a falling-out with its biggest investors. ACDG says he no longer holds stock in the group; Bernstein says he is seeking compensation after an initial court settlement in January.

For now, Gabon and ACDG are pushing ahead. In the absence of oversight, their success depends less on whether the credits help avert climate change and more on whether and how much a buyer will pay.

In December, US oil company Hess Corp. sealed the first purchase agreement for a similar kind of “high forest, low deforestation” credits with Guyana. Earlier in the year, the International Civil Aviation Organization said those credits could be used by airlines to offset their emissions. Experts have cautioned the credits will fail to serve their purpose.

If ACDG or Gabon can make a deal, it will add fuel to the efforts of other rainforest nations across the world’s tropical belt.

It could also pit the government at odds with the private sector. Gabon is one of a handful of countries with agreements to generate and trade their own carbon credits under a new carbon market run by the United Nations, according to Trove Research Ltd., a carbon analytics company. Last year, White castigated TotalEnergies over a new forest-based credits plan in Gabon. “They don’t have the rights” to that carbon, he said.

ACDG retains the government’s support. The success of the Grande Mayumba project would encourage “forest countries to continue preserving their forests,” said Daouda of Gabon’s sovereign wealth fund, which will market the country’s carbon credits. For him, it would answer the country’s big question in the affirmative: “It would mean that today, the world is recognizing that a living tree has higher value than a dead one.” —With Akshat Rathi and Ben Elgin

Read original article

As countries around the world race to combat the effects of climate change, carbon trading continues to gain traction.

Carbon trading is the buying and selling of permits of carbon credits that allow the holder to emit a certain amount of carbon dioxide and other greenhouse gases (GHGs).

Financial site Investopedia defines a carbon credit as the equivalent of one tonne of carbon dioxide or any other GHGs that an organisation can emit into the atmosphere.

Essentially, companies are awarded credits to allow them to continue to pollute up to a certain limit, often on a reducing basis.

While some businesses are able to cut their emissions, others are not able to do so. For some, their emissions might even increase in the course of a given period.

Those that cannot reduce their emissions are, however, allowed to continue operating, but usually at a higher cost.

In some instances, businesses are unable to exhaust their credit limits even after operating for the marked duration. These are called ‘‘surplus’’ or ‘‘excess’’ credits.

When a business is left with unutilised credits, it can sell them to other businesses. The business may also choose to keep the surplus credits for future use.

While carbon credits and carbon offsets are sometimes used interchangeably, they are different commodities with the same goal of reducing the emission of carbon and other GHGs into the atmosphere.

Carbon credits are limited to within an area and are regulated by a governing body. It is this governing body that is also responsible for creating and distributing them to companies operating within that jurisdiction.

Carbon offsets are neither created by a specific entity nor distributed by a particular body. Instead, they are traded freely on ‘‘voluntary markets.’’

Read: Northern Kenya conservancies eye pie of carbon credit billions

While carbon credits ‘‘cap’’ emissions, carbon offsets compensate an organisation for investing in carbon projects, also called green projects, that help to cut down emissions.

Carbon offset projects can be realised through activities that either reduce the emission of greenhouse gases or those that increase carbon sequestration.

Some of these activities may involve investment in renewable energy forms to displace fossil fuels that emit carbon and reforestation to increase the number of trees that serve as carbon sinks.

This trade dates back to 2014. A group of 60,000 smallholder farmers in the Western region under the Kenya Agricultural Carbon Project (KACP) earned carbon credits for sustainable farming.

The credits had been issued worldwide under the sustainable agricultural land management (SALM) carbon accounting methodology.

The programme supported the farmers to grow crops in a productive, sustainable and climate-friendly manner.

With its forests, expansive grasslands and wetlands, Kenya is considered a rich carbon offset sink. This is expected to improve even further once the country attains its target of planting 15 billion trees in the next 10 years.

One of the functions of the National Climate Change Action Plan under the Climate Change Act of 2016 is ‘‘to guide the country toward the achievement of low-carbon climate-resilient sustainable development.’’

It does not, however, address specifically how trading in carbon credits, as a climate change response, will be regulated in Kenya.

Environment lawyer Stella Ojango acknowledges the gaps, noting that Kenya’s limited regulatory framework and absence of requisite laws make carbon trading in the country an almost opaque undertaking.

‘‘We have the Climate Change Act of 2016, but it does not address carbon trading sufficiently. We need to amend that Act so that we can introduce regulations for trading carbon. Enriching our laws will help to regularise this business.’’ Ojango says.

Last year, the Nairobi International Finance Centre (NIFC) said Kenya lacks a clear framework for buying and selling carbon credits locally.

The body noted that this unregulated sale of carbon credits costs the country billions of shillings in unrealised revenues.

The organisation is planning to establish a carbon trading exchange in the country to allow small-scale trade-in credits.

‘‘We need to have in place mechanisms that measure how much carbon is being absorbed through reforestation. This way, we will have created a market. Regulating the pricing aspect will then become easier,’’ Ojango adds.

Kenya is not alone in lacking proper regulation for carbon trading. Most of the carbon credit markets in the developing world are unregulated by law. There are no agreed prices for carbon credits.

Plans are underway to establish a global carbon credit and carbon offset trading market. This was agreed on by negotiators at COP26 in Glasgow in 2021. Carbon credits also exist within markets with Cap & Trade regulations.

A number of businesses and organisations are already making money from either carbon credits or carbon offset programmes.

In Northern Kenya, conservancies are increasingly moving away from tourism as their mainstay to now invest in carbon projects as a source of revenue.

Northern Rangelands Trust (NRT), for instance, has put 4.7 million acres of grassland under a carbon project.

NRT is a group of 39 marine and land conservancies that cover, among other counties, Laikipia, Samburu, Tana River and Lamu. Out of these, 14 are under the project.

The Northern Rangelands Carbon Project will focus exclusively on the removal of carbon from the soil, with a target of 50 million tonnes of CO2 in 30 years. This effectively makes it one of the few projects of this scale in the market globally.

Last year, Kenya Forest Service (KFS) signed a deal with global audit firm BDO that would see the government agency earn millions of shillings for offsetting carbon dioxide.

According to the deal, KFS will rake in $15 (Sh1868) for every tonne of carbon dioxide removed from the atmosphere by government forests.

In villages in coastal Kenya, communities living near the sea are selling ‘‘hewa kaa’’ to international corporations to help them reduce their carbon emissions.

This carbon project is promoting the conservation and sustainable use of mangrove resources by the villagers.

While widely adopted around the world today, carbon credits still divide opinion. Those in support say carbon trading is a ‘‘measurable and verifiable’’ emissions reduction strategy through climate projects.

Those opposed to carbon offsets call the trade ‘‘a scammer’s dream scheme’’ and the next big thing in greenwashing.

Climate change advocacy organisation Greenpeace dismisses carbon offsets as a bookkeeping trick ‘‘intended to obscure climate-wrecking emissions.’’

Read original article