To achieve sustainable development, every economy must create and sustain equal opportunities for individuals to meet their current and future needs. COVID-19 presents a risk in realising this goal. The World Bank estimates that the pandemic will push between 88m and 115m into extreme poverty by the end of 2021, 80% of these “new poor” will be in middle-income countries, such as Kenya.

WHY COVID-19 PANDEMIC WILL HIT THE POOREST HARDEST

Impact of COVID-19 on employment

The role of employment in achieving a sustainable future is highlighted in Sustainable Development Goal 8, which aims to “promote sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all”. COVID-19 sets sub-Saharan Africa (SSA) further back in realising this goal.

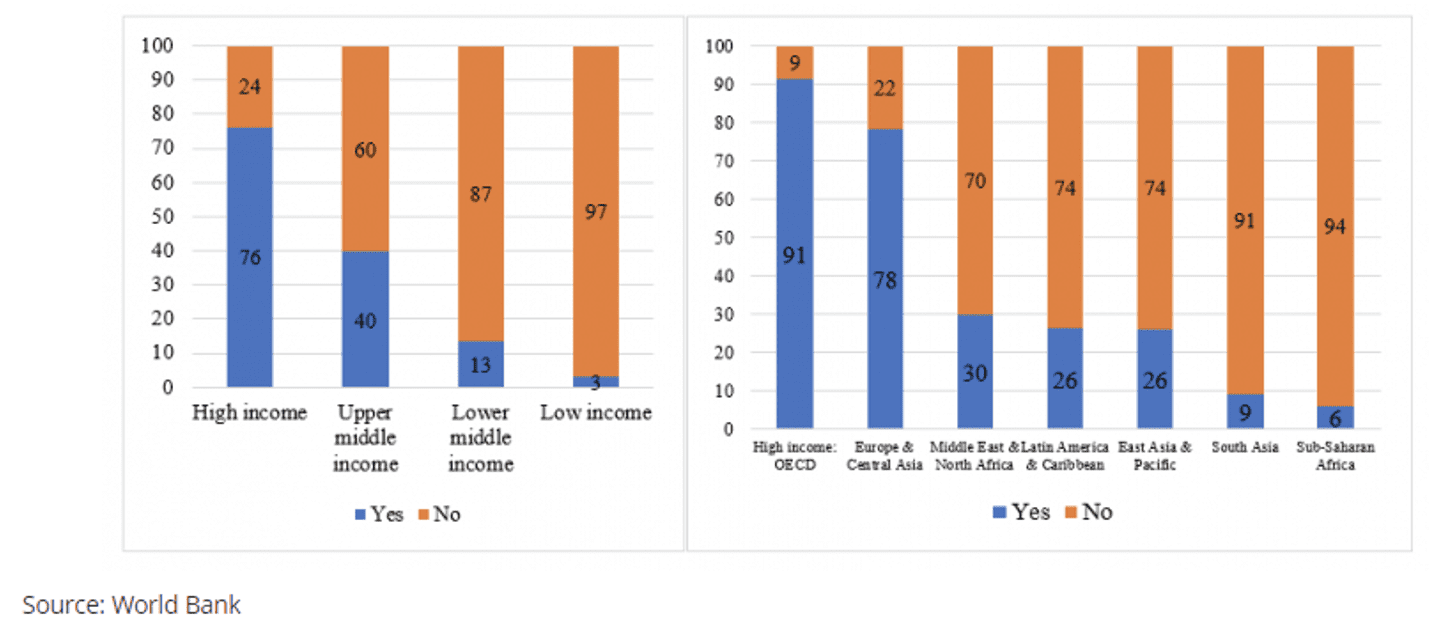

The African Union estimates that the continent could lose 20 million jobs both in the formal and informal sectors due to the pandemic. According to the World Bank, only 6% of countries in SSA have some form of unemployment protection programme which means there is no support to retain workers during economic downturns or to provide income security to unemployed workers. And it is expected that women will be affected disproportionately as 70% of women in developing countries are employed in the informal economy.

Figure 1: Availability of unemployment protection varies widely by income and region

Impact of COVID-19 on Poverty in SSA

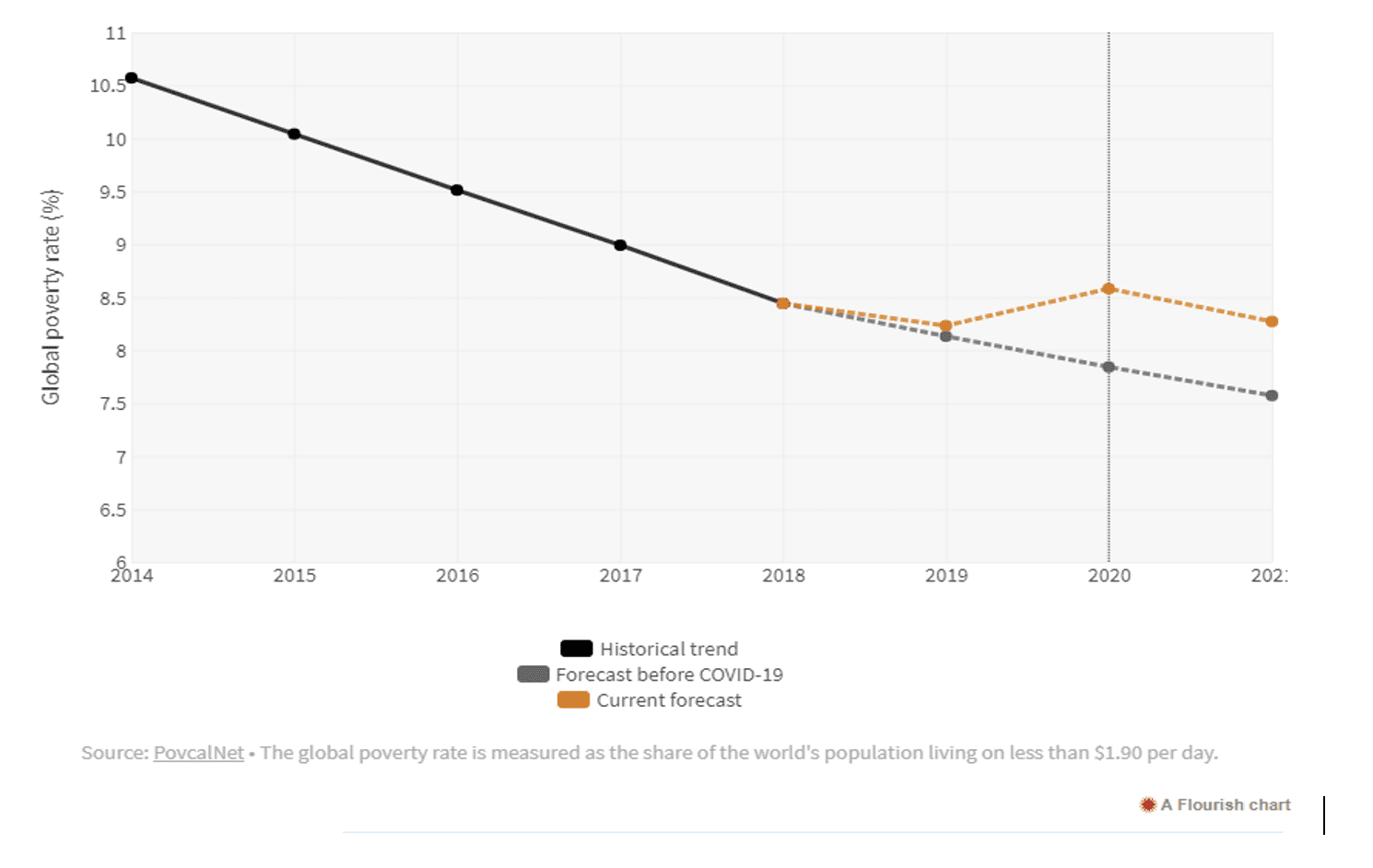

As African economies are plummeting into economic difficulties in the wake of COVID-19, extreme poverty rates are expected to increase as African economies struggle to finance and manage the pandemic. The World Bank’s Poverty and Shared Prosperity 2020 report shows that pandemic-related deprivation worldwide is hitting poor and vulnerable people hard and the World Food Programme is warning of an upcoming hunger pandemic¹.

Figure 2: The Impact of COVID-19 on Global Poverty

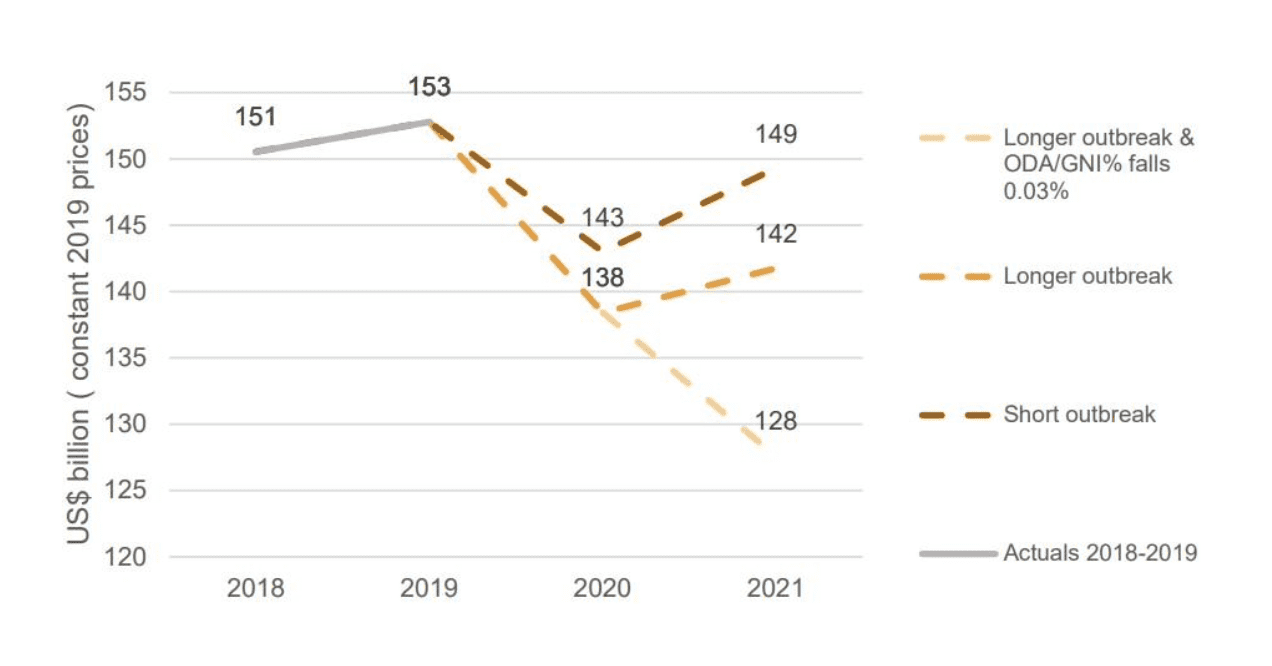

As the figure below illustrates, aid experts have issued a cloudy forecast on official development assistance which could see a global drop of US$25 billion by 2021.

Figure 3: Economic recession in donor countries may sharply reduce ODA levels, especially if donors reduce the share of national income spent on aid.

Effect of COVID-19 on building more equal, inclusive and sustainable economies

Due to the pandemic, vulnerabilities in social systems have been exposed. Gender-based violence has increased due to economic and social distress coupled with restricted movement and social isolation measures. These impacts have been amplified more in contexts of fragility, conflict and emergencies. Social protection programmes help to mitigate the economic fallout of lockdown measures, especially for those without the luxury to work from home and self-isolate. As of June 2020, 49 African countries had introduced social assistance which accounts for 84% COVID related response.

COVID-19 has worsened credit and liquidity constraints among micro, small and medium enterprises (MSMEs)². FSD Africa has responded to this by making five investments to support business liquidity, for example, FSD Investments has invested in Blue Orchard to enable Tier 2 and 3 MFIs to access immediate liquidity. As a result, the MFIs will be able to manage their deteriorating portfolios and have access to the longer-term finance to avert insolvency and further job losses.

What can we do to prepare for future pandemics?

COVID-19 is unlikely to be our last pandemic, and it might not be the worst. To build resilience in the society, an introduction of pandemic insurance policies will be on the rise and a vital part of the planning and preparing for the next pandemic. Providing affordable insurance policies for SMEs, MSMEs and workers in the informal sector will help mitigate the economic effects of future pandemics. In a new FSD Africa publication “Never waste a crisis – how sub-Saharan African insurers are being affected by, and are responding to, COVID-19” we find that while the pandemic has exacerbated pre-existing weaknesses of the insurance sector in SSA, it also provides an opportunity for insurers and regulators to become better equipped to embrace and adopt innovation and develop their insurance markets. COVID-19 has created an imperative for regulators to address the barriers to digitisation as well as proactively encouraging innovation in the sector.

Another approach that FSD Africa is exploring is a COVID-19 development impact bond, an outcome-based investment instrument with a goal to mobilise £11m. In partnership with UK aid, AMREF, and APHRC, this impact bond would be the first of its kind, aimed at meeting social outcomes relating to the prevention of the spread of COVID-19 in informal settlements in Kenya (Nairobi, Mombasa and Kisumu). This is a pilot project which could in future be replicated in other countries, not only rgency responses but also to support governments in meeting other healthcare priorities.

To find out more about FSD Africa’s response to the pandemic, and how we’re contributing to efforts to build back better, you can read the latest CEO’s updates and explore our Impact Report.

¹ Global report on food crisis 2020

² Economic impact of Covid-19 on micro, small and medium enterprises (MSMEs) in Africa and policy options for mitigation, COMESA special report